11. EU Investment in Energy Supply for Europe

© Chapter Authors, CC BY 4.0 https://doi.org/10.11647/OBP.0280.11

Introduction

A central element of the European Green Deal is the commitment of the EU to become climate neutral by 2050. Against that backdrop, the European Commission promises a “shift from strategy to delivery” in 2021, and the 2021 EU climate law states that the EU will reduce greenhouse gas emissions by at least 55% by 2030 compared to 1990. The “Fit for 55 Package” is wide-ranging in scope, encompassing renewables, delivering on the “energy efficiency first” principle, energy performance of buildings, land use, energy taxation, effort sharing and emissions trading.1 It goes without saying that this requires the multiannual financial framework (MFF) 2021–27 to allocate resources accordingly.

The unprecedented measures taken in the spring of 2020 by the EU to counter the unprecedented crisis triggered by the spread of the coronavirus SARS-CoV-2 have been designed in the spirit of “building back better”: they shall not simply get the EU economy back on the trajectory it was on before the crisis, rather they shall help switch this huge economy to an ambitious trajectory that realises the European Green Deal.

One of many aspects of this endeavour is the allocation of public investment resources for the energy supply for Europe. Such resources fall into three categories. First, there are those mobilised in the 2021–27 MFF. Second, there are the exceptional resources made available through what Olaf Scholz, the German minister of finance, labelled as a Hamilton moment for Europe (more about this below): the decision that the EU would raise €750 bn (at 2018 prices) on the international financial markets. Eventually, these resources were grouped under the label Next Generation EU (NGEU). And third, there are the resources that the European Investment Bank, EIB, by its mandate, can regularly raise on the same markets.

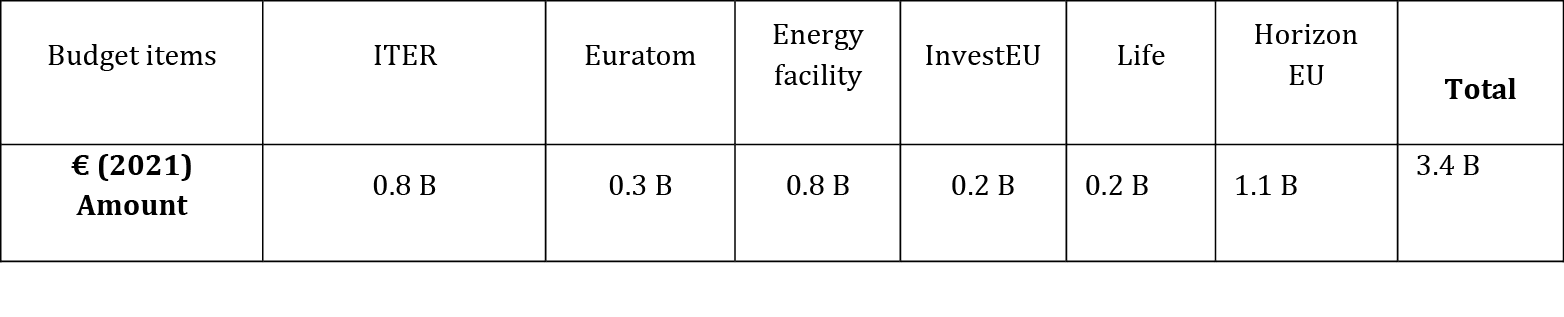

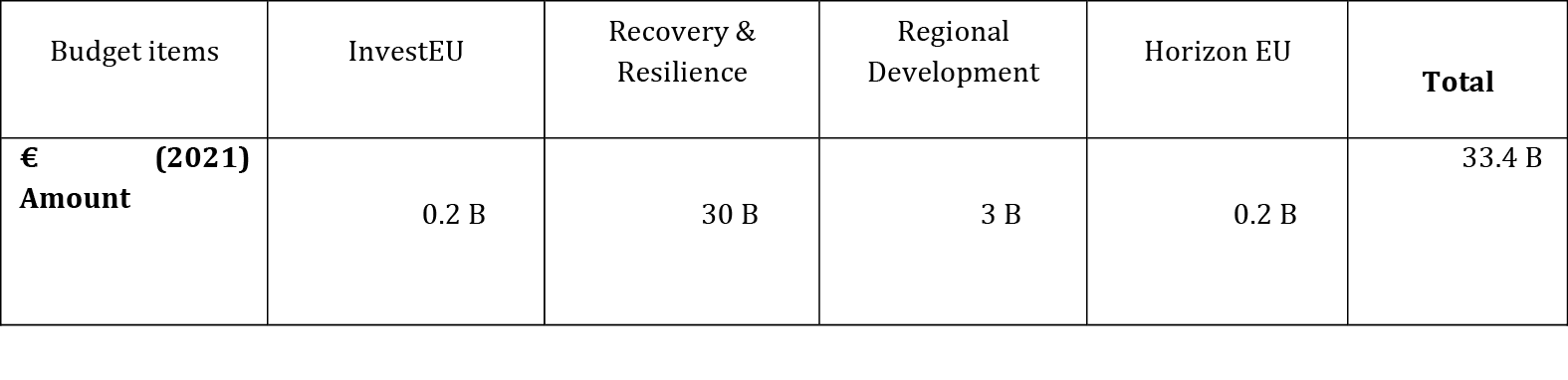

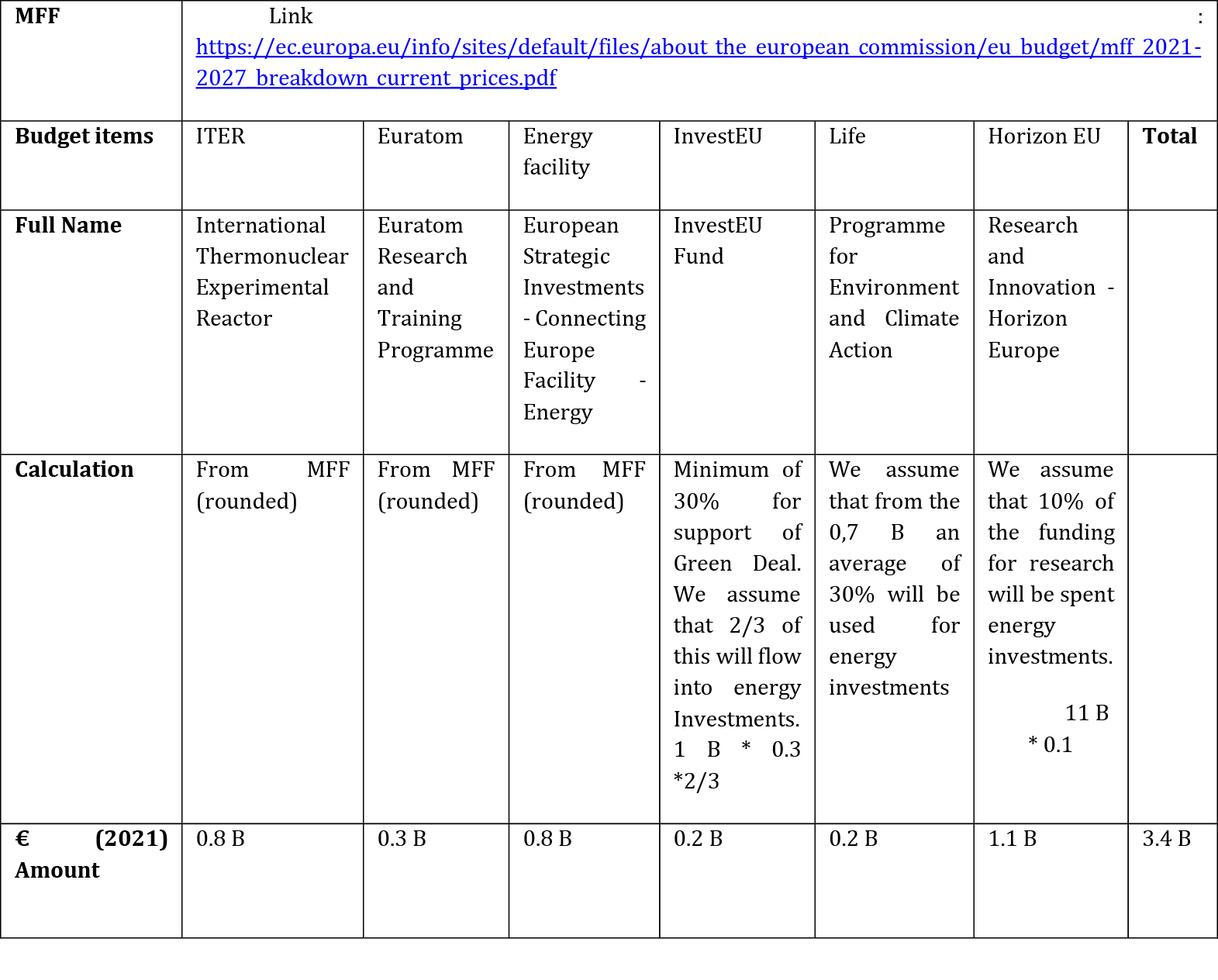

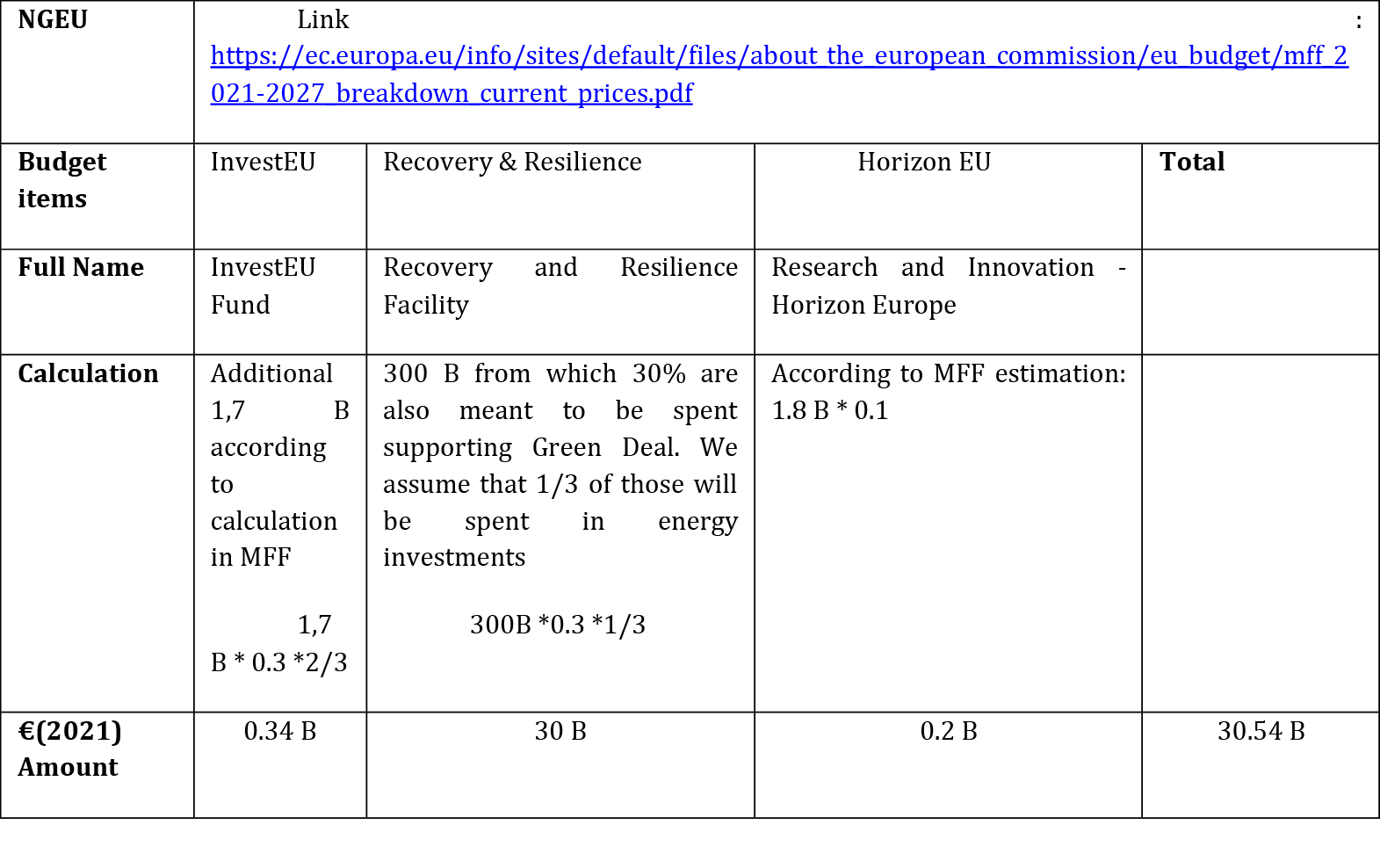

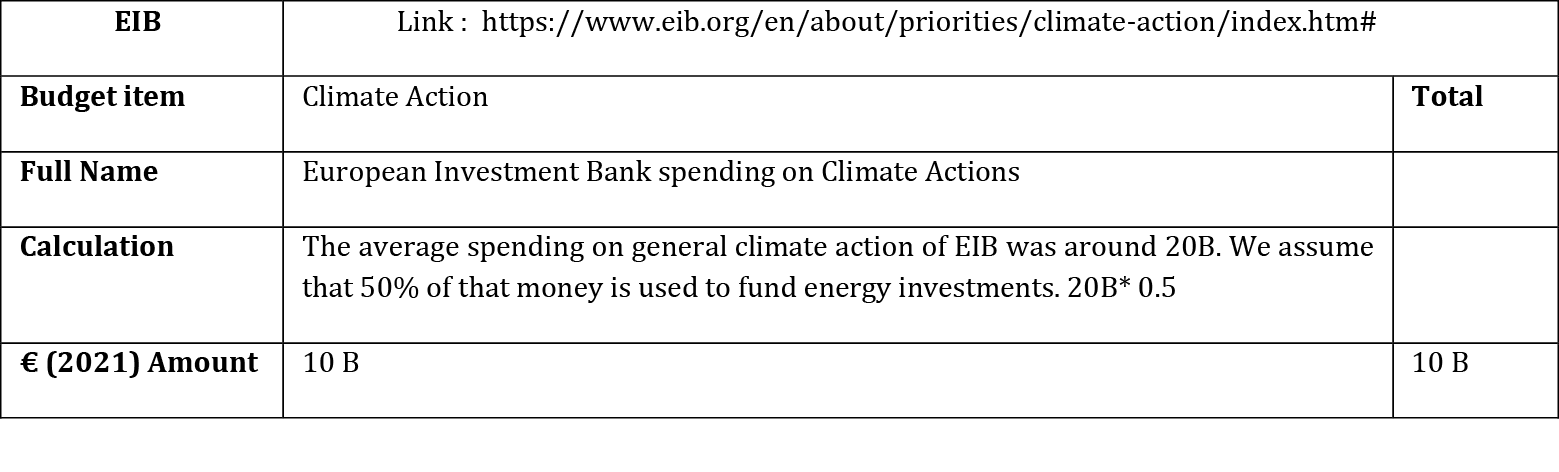

With regards to investment for the energy supply for Europe, estimates for the resulting numbers in 2021 are collated in Tables 1a, 1b, and 1c (see the Annex for sources and explanations).

a) MFF

b) NGEU

c) EIB

Table 1a, 1b, 1c: EU Investment in Energy Supply for Europe in 2021

For sources and supplementary information, see the Annex.

The total over the three budgets is €46.8 bn. The three totals come with leverage rates for investments of various kinds that will be discussed in more detail below. For the MFF, a reasonable leverage ratio is 1.2, leading to an enhanced amount in the order of €4.1 bn. For NGEU, a reasonable leverage ratio is 1.5, leading to an enhanced amount in the order of €50.1 bn. For the EIB, a reasonable rate is 2, yielding €20 bn. All three together then amount to an investment flow of €74.2 bn. To put these numbers in perspective, one needs to consider some implications of the 55% reduction goal of the EU for 2030.

11.1 The 2030 Challenge

Several studies (EEA 2020; Agora Energiewende & Ecologic Institute 2021) based on EU Long-Term Strategy and European Green Deal project at least a 10% gap for EU emissions reductions in its current baseline scenarios for 2030. They also estimate that in the 2021–30 period the EU will need to invest €35–88 bn per year more for buildings and transport alone. Despite significant climate financing allocated in the European Green Deal, EU financing alone will not close the projected investment gap. McKinsey & Company (2020) state that an average incremental investment of €160 bn per year is needed for the 2021–30 period. Of this amount, 31% (€50 bn) is allocated to buildings and 12% (€19 bn) is allocated to transport.

In 2019, 69.3% of all energy in the EU was produced from fossil fuels, namely coal (11.6%), oil and petroleum products (34.5%), and natural gas (23.1%) (all numbers from Eurostat 2021a). Renewable energies made up 15.8% of the total, nuclear accounted for 13.5%. A 55% reduction of emissions implies a reduction of fossil fuels in the order of 30% of total energy use (38% if the fossil fuel mix should stay unchanged). To replace this with renewables, the EU would have to triple the present production of renewable energy within ten years. Alternatively, one might double the amount of both renewables and of nuclear. The contribution of renewable energy sources showed a stable growth, having already surpassed coal in 2018 and further increasing in 2019. Coal decreased by 19.7% in 2019 and reached the record lowest value since 1990.

One may try to boost this process by importing renewable energy from outside the EU. Presently, about 60% of fossil fuels used in the EU are imported (Eurostat 2021a). In principle, large scale imports of renewable energy are feasible, e.g., as green hydrogen or via high-voltage direct power transmission. But this presupposes the establishment of large infrastructures and institutional arrangements that are hardly feasible before 2030.

A different option is the reduction of energy use, often labelled as increasing energy efficiency (European Commission 2020). A reduction of energy use by one third in the nine years remaining until 2030 is not impossible, but hard to achieve and definitely harder without increasing the EU’s current energy efficiency target (32.5% for 2030). The 55% reduction could then be achieved by doubling renewable energy generation. Clearly, this requires massive investments in wind and solar power plants, combined with similarly massive investments in power grids. Green hydrogen may play an increasing role, but it will hardly reach a sufficient volume to make a huge difference by 2030.

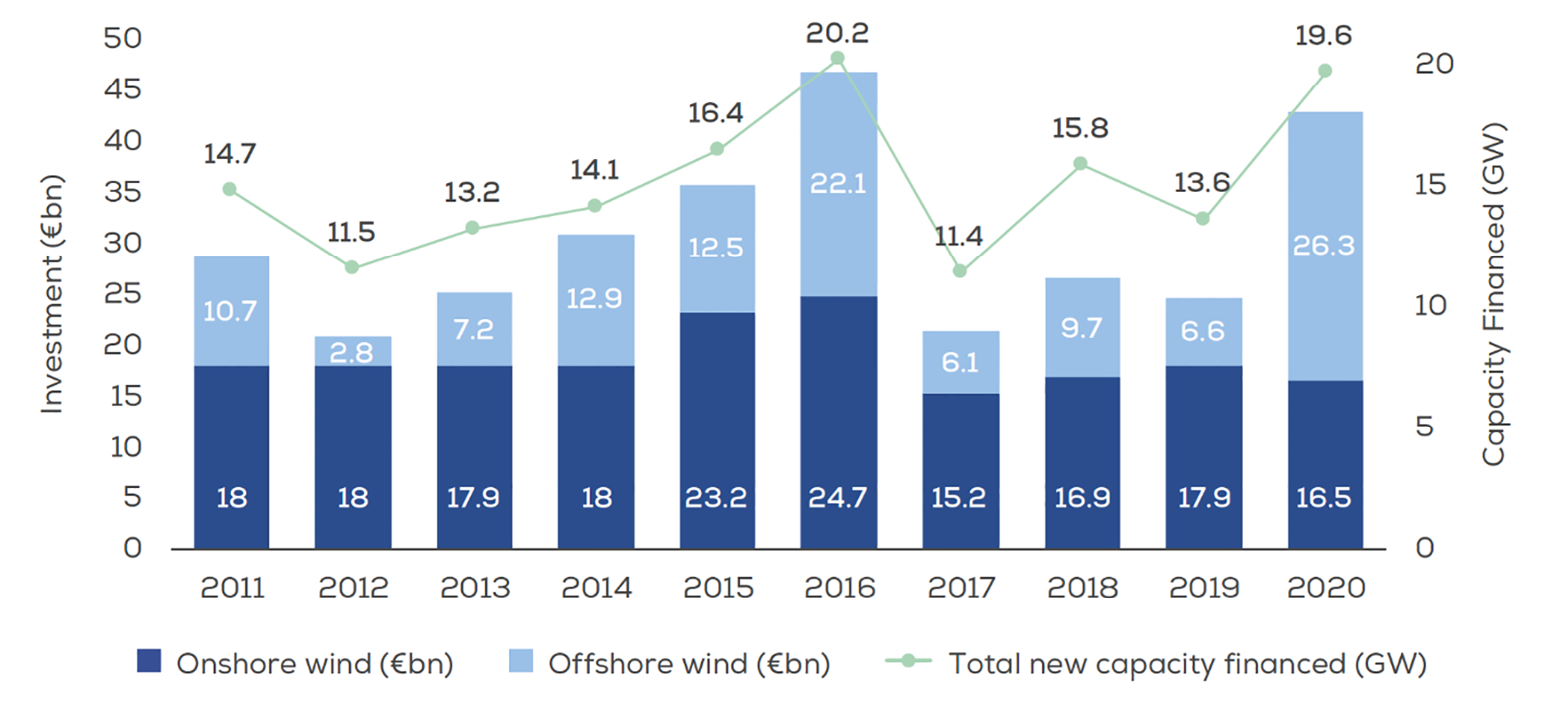

Fig. 1 New Asset Finance in Wind Energy 2011–20 (GW and € bn).

Source of data: Wind Europe (2021).

In view of the energy supply for Europe, the upshot of this analysis is that the 2030 goal will require unprecedent investments in renewables. So far, the highest investment in Europe in wind energy alone took place in 2016, when it reached €46.8 bn for a total new capacity of 20.2 GW, followed by 2020 with 42.8 for 19.6 GW (Figure 1).

With the previous, less ambitious targets for 2030, total annual investment needs for wind, solar, transmission, distribution, and storage were estimated in the range of €95–145 bn (Trinomics 2017). With the raised ambition of the -55% target, €150 bn is more realistic. The leveraged figure of about €75 bn from Tables 1 a, 1b, and 1c may give the impression that the door for those investments is wide open. However, these numbers are for the envisaged disbursements from the EU to member states, the actual investments will come with a delay. What is more, the grant allocations last for three years only, allocation of loans for two years. Front loading these financial flows is appropriate for the purposes of economic recovery, but for the needed changes in energy supply up to 2030 they cannot suffice.

Of course, additional investments for renewable energy supply can and will be induced by specific regulation and increasing CO2 prices. The political, economic, and technological obstacles to be overcome EU-wide, however, are substantial. And without further measures to stimulate effective demand, these politically induced investments will crowd out other investments, putting a drag on growth and thereby employment in other sectors.

The macroeconomic impact of EU investments in energy supply must not be overestimated. In 2019, gross investment in the EU was 22.1% of GDP, i.e., €3.1 bn. Of these, energy supply investments of €150 bn would make up 1% of EU GDP. As long as they are mainly shifted from other sectors and lasting only two or three years, the overall economic impact will be limited.

A substantial positive effect, however, can be reached if EU energy supply investments will be additional and steady until 2030 or later. We are well aware of how contentious the debate about such possibilities is (Amato et al. 2020; Arnold et al. 2018; Bini-Smaghi 2021; Schäuble 2021). Unfortunately, the debate is still rather obsessively focused on the volume of public debt. But the historical breakthrough of the original Hamilton moment, the compromise struck between Hamilton, Jefferson, and Madison in 1790, was not about an increase of public debt (public debt was only shifted from single states to the US), but about the creation of an effective market for US bonds. Without this market, the US would never have achieved its impressive successes. Nowadays, the financing and possible success of the European Green Deal are tied to an analogous challenge.

Whether the Franco-German compromise of 2020 will usher in a Hamiltonian dynamic for the European Green Deal remains to be seen. It will critically depend on whether Germany will develop the will and competence to become the benevolent catalyst of a European Renaissance, or whether it will stick to a mercantilist interpretation of its national interest.

11.2 Employment and Geography

In terms of economic variables, the energy sector is a small part of the economy (Taylor 2021). We have seen this by comparing investment in the energy sector with overall investment. The same holds when considering employment. However, the effects of decarbonisation on employment are a big topic, especially as decarbonisation is being pursued in a global context of digitalisation. A closer look at employment is warranted, especially in view of the European Green Deal.

Table 2 shows a breakdown of employment in the energy sector, broadly defined, for EU28 from 2010 to 2018. Taking Brexit into account, employment in the EU27 by now is somewhat below 2 million people. The number of employees in the EU27 in turn is in the order of 220 million: the energy sector amounts to less than 1% of total employment. Table 2 also suggests that the bulk of energy sector jobs is in electricity, gas, steam and air conditioning supply. An emissions reduction of 55% by 2030 is unlikely to reduce the number of jobs in this domain; quite the opposite: the transformation of the energy system will require more craftspeople and professionals able to handle the new devices and technologies to be introduced.

Table 2: Employment of the EU28 Energy Sector, 2010–18 (Czako 2020).

|

Thousands |

2010 |

2015 |

2016 |

2017 |

2018 |

|

Mining and Coal Lignite |

331.2 |

294.5 |

274.1 |

258.9 |

247.6 |

|

Extraction of Crude Petroleum and Natural Gas |

103.8 |

88.9 |

81.4 |

70.0 |

60.7 |

|

Extraction of Peat |

11.1 |

11.1 |

9.9 |

9.7 |

9.7 |

|

Support Activities for Petroleum and Natural Gas Extraction |

47.7 |

56.8 |

48.0 |

41.4 |

41.4 |

|

Manufacture of Coke and refined Petroleum Products |

218.7 |

190.0 |

186.5 |

188.6 |

193.6 |

|

Electricity, Gas, Steam and Air Conditioning Supply |

1645.3 |

1550.5 |

1553.0 |

1546.0 |

1569.1 |

|

Broad Sector Total Employment |

2357.9 |

2191.8 |

2152.9 |

2114.5 |

2122.0 |

Of course, things may look very different in other sectors. But as far as the energy sector is concerned, the challenge at the scale of the EU labour market as a whole concerns about 0.25% of the total labour force. Regular fluctuations on the labour market are much larger than this. However, here we are faced with half a million people concentrated in regions where the fossil fuel-based energy sector plays a prominent role. Whether employment in a coal-mining region can turn into jobs focused on generating wind and solar power is far from obvious. How to address the challenge these regions are faced with is a hard problem that needs and deserves in-depth research (for an example of research in this direction, see https://tipping-plus.eu).

When looking at employment, geography matters. In the EU and especially the Eurozone, this is particularly relevant with regard to the divergence of the Eurozone (Gräbner et al. 2020). In the Next Generation EU package, this divergence is addressed by allocating the largest budget to Italy and the second largest to Spain.

Looking first at Italy, one of the most pressing problems is indeed the one of employment (the following numbers are from https://tradingeconomics.com): at the time of writing, the unemployment rate is larger than 10% for Italy as a whole, with youth unemployment higher than 30%. Moreover, unemployment is heavily concentrated in the south of Italy. The plan for how the Italian government, led by former ECB president Mario Draghi, intends to use the money from the EU pandemic recovery funds reflects this challenge (MEF 2021; Johnson and Fleming 2021). The priority is on digitalisation and high-speed rail. These technological investments shall help increase productivity across the whole of Italy, including both the private and the public sector. They are explicitly planned in the perspective of the European Green Deal, but with an emphasis on energy renewal of the—private and public—buildings more than on expanding renewable energy generation. This makes perfect sense, as construction has a much larger potential for job creation than the energy sector. And according to the European Commission (2020) the contribution of energy efficiency to the -55% reduction goal for 2030 is as important as the expansion of renewables generation. Last but not least, by improving train connections across Italy, explicitly aiming at sustainable mobility at the local scale, and strengthening the health sector shattered by the pandemic, tourism can rebound as a key sector of the Italian economy.

The details of the Italian plan are sound, and the argument from the previous section applies here, too: it will be crucial to avoid the temptation of a new austerity cycle in the coming years and instead stabilise the measures undertaken as a reaction to the pandemic at least until the 2030 goal has been reached.

The situation in Spain is similar in many respects, although internal tensions are presently making the task of forming a common will even more difficult than in Italy. At the time of writing, the unemployment rate is in the order of 15%, with youth unemployment at nearly 40% (numbers from https://tradingeconomics.com). For good reasons, the goals are similar to those in Italy: strengthen employment and foster growth (Gobierno de España 2021; Lázaro Touza 2020). Given the structure of the Spanish economy, including its tourist sector, the plan has a strong focus on supporting SMEs. Again, digitalisation is high priority, as is sustainable mobility. Generation of renewable energy is included, but not at a scale that would change the energy supply for the EU or the growth rate of the Spanish economy. However, a long-term strategy in the direction of green hydrogen production is embedded in the plan, as is an emphasis on science, technology, and education.

When it comes to renewable energy supply for Europe, the big difference in the present decade will not come from the countries prioritised by Next Generation EU, but from countries like Germany and Denmark, who can expand renewable generation with domestic means if they avoid a return to austerity.

11.3 “There is No Alternative” or Experimentalist Governance?

When thinking about a historical project like the European Green Deal, one may be forgiven for imagining it as defined by necessities that are as inevitable as they are foreseeable. The whole process is then governed by “TINA”: there is no alternative.

Once this perspective is embraced, the transition to a climate neutral Europe starts looking like a journey on trains with well specified timetables, clearly foreseeable transfers from one train to another, and a sense of safety strengthened by smoothly running organisations. Expanding the generation of renewable energies can be envisaged with such a mindset, too, and in many contexts this is the way to go. But there is danger in ignoring the fact that contexts change, and often in unexpected ways.

An important example is the idea of leveraging large private investments with small public ones. As we have seen, the public investment in renewable energy financed through the combination of MFF, NGEU, and EIB is quite small; first, because the largest annual budget, the one of NGEU, is designed for no more than three years, and second, because for perfectly understandable reasons the main recipients of NGEU funds, while determined to use them for a broad ecological transition, don’t focus on large-scale expansion of renewable energy generation. In this situation, the idea of leveraging large private investment through small public ones is comforting. In fact, there is overwhelming evidence to the effect that there are contexts where such leverage is considerable, but there is also evidence for contexts where the effect is much smaller (Boitani and Perdichizzi 2018). Moreover, while some of the relevant contexts are known (economic recessions vs economic booms), many of them defy easy definition (e.g., through output gaps; see Heimberger and Kapeller 2016).

In the case of NGEU, the leverage ratio boils down to the multiplier linking government expenditure to effective demand. As NGEU funds are disbursed in situations of economic crisis, high unemployment, capacity underutilisation, and strong incentives for investing in renewable energy, the leverage of 1.5 used in Section 1 is a conservative estimate. The same holds for those MFF expenditures that go into investment for expanding capacity of renewable energy generation. ITER and Euratom are not in this category (if some day nuclear fusion should really work, the whole analysis about renewables might have to change—but that’s certainly irrelevant for the present decade). That’s why for MFF a leverage of 1.2 is more appropriate.

The EIB presents a fundamentally different situation. First, the EIB engages in co-financing of investments. From the point of view of the investor, alternative co-financing is usually available, although often at somewhat less advantageous conditions. Many profitable investments co-financed by the EIB would still take place with other co-financing partners. Simply using the ratio of the total investment volume to the EIB contribution as a leverage factor is misleading. On the other hand, the EIB does encourage and sometimes trigger investments—especially by public authorities—that would not take place otherwise. That’s why a leverage factor of 2, i.e., somewhat higher than for NGEU, is a reasonable estimate in this case.

In the past two decades, the EU economy, like smaller and even bigger economies, has experienced diversity of contexts and their often unforeseen changes on two dramatic occasions: the Global Financial Crisis and the COVID-19 pandemic. Perhaps no surprises of that scale will happen during the transition to climate neutrality, but for sure surprises will happen. This is where the concept of experimentalist governance (Sabel and Zeitlin 2012; see also Foray and Woerter 2021) matters for the expansion of renewable energies as well as for other dimensions of the European Green Deal.

Experimentalist governance can build on the diversity of regional contexts by creating conditions that allow and enable different regions to implement different strategies. For this purpose, regions need a safety net to engage in risky endeavours. And if they succeed, they need to share their learning experience with others without trying to impose a simplistic recipe. In this spirit, a Spanish region may aggressively explore the options for green hydrogen, while a region in Italy may gather experience with methanol gained from air capture of CO2 in a circular economy perspective (Olah et al. 2018).

Public and private investments in expanding renewable energy generation offer scope for strategic leadership, e.g., in expanding offshore wind wherever it is possible and reasonable. And they offer scope for complementary approaches in different regional contexts as illustrated above. What matters is to combine the diversity of experiences needed to navigate future surprises with the perseverance of pursuing the opportunity created by the near-Hamilton moment in the midst of the COVID-19 pandemic.

ANNEX: Background for Tables 1a, 1b, 1c

References

Agora Energiewende (2019) European Energy Transition 2030: The Big Picture. Ten Priorities for the next European Commission to meet the EU’s 2030 targets and accelerate towards 2050, https://www.agora-energiewende.de/en/publications/european-energy-transition-2030-the-big-picture/.

Agora Energiewende and Ecologic Institute (2021) A “Fit for 55” Package Based on Environmental Integrity and Solidarity: Designing an EU Climate Policy architecture for ETS and Effort Sharing to Deliver 55% Lower GHG Emissions by 2030, https://www.agora-energiewende.de/en/publications/a-fit-for-55-package-based-on-environmental-integrity-and-solidarity/.

Amato, M., E. Belloni, P. Falbo and L. Gobbi (2020) Transforming Sovereign Debts into Perpetuities through a European Debt Agency, http://dx.doi.org/10.2139/ssrn.3579496.

Arnold, N. G., B. B. Barkbu, H. E. Ture, H. Wang and J. Yao (2018) A Central Fiscal Stabilization Capacity for the Euro Area, IMF Staff Discussion Note, 18/03.

Bini-Smaghi, L. (2021) “The eurozone must not return to its pre-crisis ‘normality’”, The Financial Times, June 14, 2021.

Calhoun, G. (2020) “Europe’s Hamiltonian Moment—What Is It Really?”, Forbes, May 26, 2020, https://www.forbes.com/sites/georgecalhoun/2020/05/26/europes-hamiltonian-moment--what-is-it-really.

Czako, V. (2020) Employment in the Energy Sector Status Report 2020. Publications Office of the European Union, JRC120302, https://doi.org/10.2760/95180.

European Commission (2020) Greenhouse Gas Emissions—Raising the Ambition, https://ec.europa.eu/clima/policies/strategies/2030_en.

European Commission (2021) Multiannual financial framework, https://ec.europa.eu/info/sites/default/files/about_the_european_commission/eu_budget/mff_2021-2027_breakdown_current_prices.pdf.

European Environment Agency (2020) Trends and projections in Europe 2020 Tracking progress towards Europe’s climate and energy targets, https://www.eea.europa.eu/publications/trends-and-projections-in-europe-2020.

Eurostat (2021a) Energy statistics—an overview, https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Energy_statistics_-_an_overview.

Eurostat (2021b) Data Explorer, https://appsso.eurostat.ec.europa.eu/nui/show.do?dataset=nama_10_a64_e&lang=en.

Eurostat (2020), National Accounts and GDP, https://ec.europa.eu/eurostat/statistics-explained/index.php?title=National_accounts_and_GDP.

Foray, D. and M. Woerter (2021) “The formation of Coasean institutions to provide university knowledge for innovation: a case study and econometric evidence for Switzerland”, The Journal of Technology Transfer, 46(5), 1584–610.

Gobierno de España (2021) Plan de Recuperación, Transformación y Resiliencia, https://www.lamoncloa.gob.es/temas/fondos-recuperacion/Documents/160621-Plan_Recuperacion_Transformacion_Resiliencia.pdf.

Gräbner, C., P. Heimberger, J. Kapeller and B. Schütz (2020) “Is the Eurozone disintegrating? Macroeconomic divergence, structural polarisation, trade and fragility”, Cambridge Journal of Economics 44: 647–69, https://doi.org/10.1093/cje/bez059.

Heimberger, P. and J. Kapeller (2016) The performativity of potential output: Pro-cyclicality and path dependency in coordinatingEuropeanfiscal policies, ICAE Working Paper Series—No. 50, June 2016, https://www.boeckler.de/pdf/v_2016_10_21_heimberger.pdf.

Johnson, M. and S. Fleming (2021) “Draghi plans €220 B overhaul of Italy’s economy”, The Financial Times, April 21, 2021, https://www.ft.com/content/29d4b262-fb4a-46be-b504-6689e0eec994.

Lázaro Touza, L., G. Escribano Francés and F. Steinberg (2020) Spain’s Recovery, Resilience and Transformation Plan: key challenges for implementation, https://www.iddri.org/en/publications-and-events/blog-post/spains-recovery-resilience-and-transformation-plan-key-challenges.

McKinsey & Co. (2020): Net-Zero Europe. Decarbonization Pathways and Socioeconomic Implications, https://www.mckinsey.com/~/media/mckinsey/business%20functions/sustainability/our%20insights/how%20the%20european%20union%20could%20achieve%20net%20zero%20emissions%20at%20net%20zero%20cost/net-zero-europe-vf.pdf.

MEF (Ministry of Economy and Finance of Italy) (2021) The Recovery and Resilience Plan: Next Generation Italia, https://www.mef.gov.it/en/focus/The-Recovery-and-Resilience-Plan-Next-Generation-Italia.

Olah, G. A., A. Goeppert and S. Prakash (2018) Beyond Oil and Gas: The Methanol Economy (Wiley).

Sabel, C. F. and J. Zeitlin (2012) “Experimentalist Governance”, in The Oxford Handbook of Governance, ed. by Levi-Faur (Oxford: Oxford University Press), pp. 169–83.

Saraceno, F. (2021) “Europe After COVID-19: A New Role for German Leadership?”, Intereconomics 56: 65–69.

Schäuble, W. (2021) “Europe’s social peace requires a return to fiscal discipline”, The Financial Times, June 2, 2021, https://www.ft.com/content/640d084b-7b13-4555-ba00-734f6daed078.

Statista (2021) Wind energy investment outlook in Europe 2010–2022, https://www.statista.com/statistics/858972/wind-energy-investment-outlook-europe.

Trinomics (2017) European Energy Industry Investments, trinomics.eu/wp-content/uploads/2018/05/European-energy-industry-investments.pdf.

Wind Europe (2021) Financing and investment trends. The European wind industry in 2020, https://windeurope.org/intelligence-platform/product/financing-and-investment-trends-2020/.

1 “Energy efficiency first” is one of the key principles of the Energy Union, intended to ensure secure, sustainable, competitive and affordable energy supply in the EU. The adaptation of the EU ETS, covering 40% of Europe’s emissions, is seen as the central instrument for reducing GHG emissions in the “Fit for 55” package.