3. Public Investment in Germany: Much More Needs to Be Done

© Katja Rietzler and Andrew Watt, CC BY 4.0 https://doi.org/10.11647/OBP.0280.03

Introduction

The analysis of the German situation in last year’s issue of the European Public Investment Outlook described public investment and the public capital stock since the German reunification. It contrasted the development of German infrastructure with economic and population growth, and showed that public investment had been insufficient for more than a decade. The country needed massive public investment in a number of fields to modernise its infrastructure as well as ensure that Germany meets its own climate policy goals (Dullien et al. 2020c). This year’s chapter looks at the most recent developments. It begins with an overall analysis of public investment across policy fields and the activities of different levels of government. The next section focuses on the massive stimulus package, which the German government launched in summer 2020―the so-called “Konjunktur- und Zukunftspaket” (stimulus and future package). We analyse the investment content of the package and the progress of its implementation. The third section focuses on the German Recovery and Resilience Plan (Deutscher Aufbau und Resilienzplan, DARP) as part of the EU’s NextGeneration programme, noting the very substantial overlap with the domestic stimulus plan. The fourth section presents recent simulations by the Macroeconomic Policy Institute (IMK) with the National Institute`s Global Economic Model (NIGEM), which show that under the current financial conditions a substantial credit-financed public investment initiative is compatible with a reduction of the debt-to-GDP ratio (Dullien et al. 2021). The concluding section sums up the resulting policy recommendations.

3.1 Public Construction Investment Softened in the Pandemic, Equipment Massively Increased

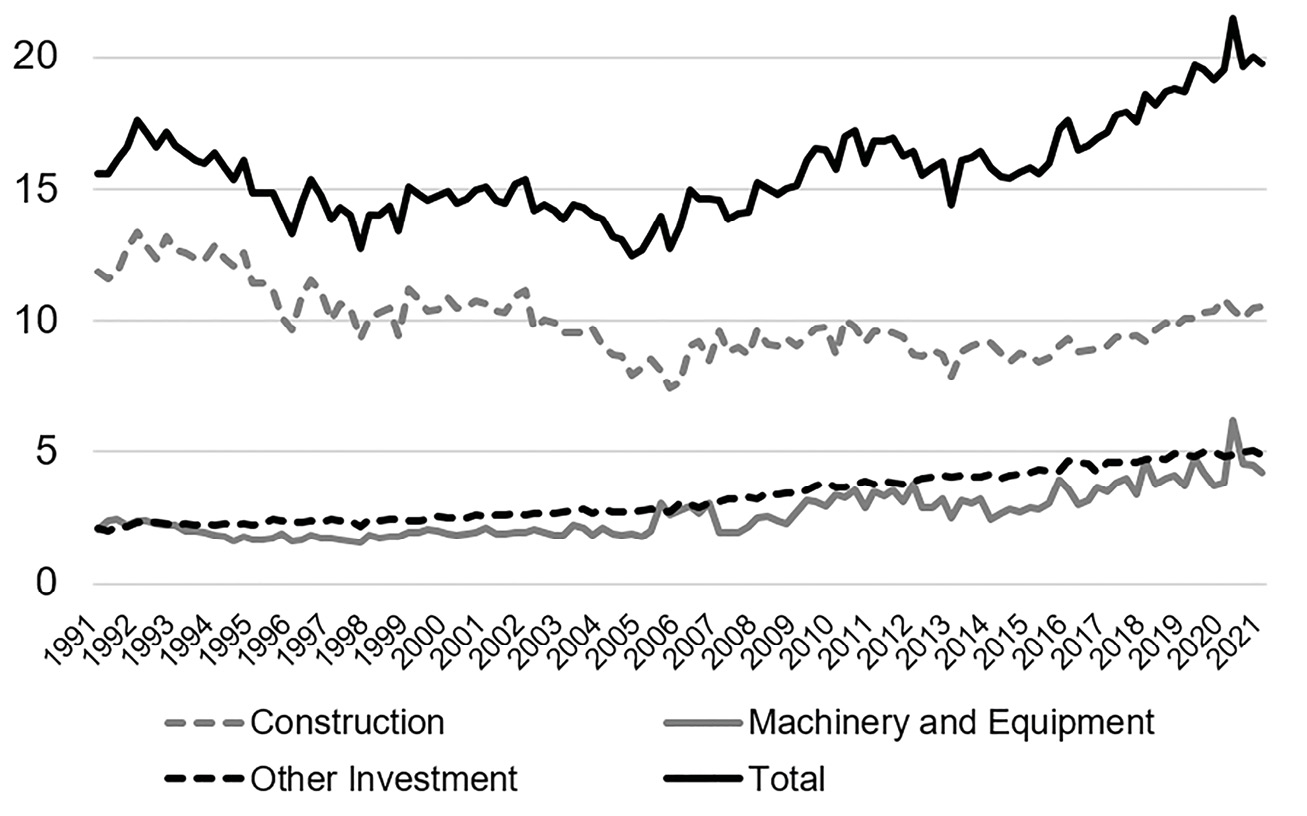

Since the early 2000s, Germany has recorded a substantial investment backlog, which has become more and more prominent in the economic policy debate in the wake of a report by the DIW Berlin in 2013 (Bach et al. 2013). As already shown in the previous European Public Investment Outlook (Dullien et al. 2020c), net public investment was negative during much of the last two decades. Stimulus packages following the financial crisis of 2008–09 caused a temporary increase in public investment. However, when they were phased out in 2012, real gross fixed capital formation of the government sector in Germany was only slightly above the level of the year 2000.

A sustained upward trend started only in 2015 (Figure 1).1 It was driven by two main factors: firstly, Germany’s population rose sharply due to the migration of hundreds of thousands of refugees, creating an urgent need for additional infrastructure; secondly, the fiscal situation improved rapidly with the strong recovery after the Global Financial Crisis. From 2014 onwards, both the federal government and the states (taken together) recorded rising fiscal surpluses, which made it easier to finance new investment projects. The increase was particularly pronounced in construction as well as machinery and equipment,2 whereas other investment3 had already been on a steady upward trend since the 1990s.

Fig. 1 Quarterly Real Gross Fixed Capital Formation of the Government Sector (in Billion Euros, Prices from 2015).

Source of data: Destatis, Quarterly National Accounts, seasonally adjusted, 1991 Q1 until 2021 Q1.

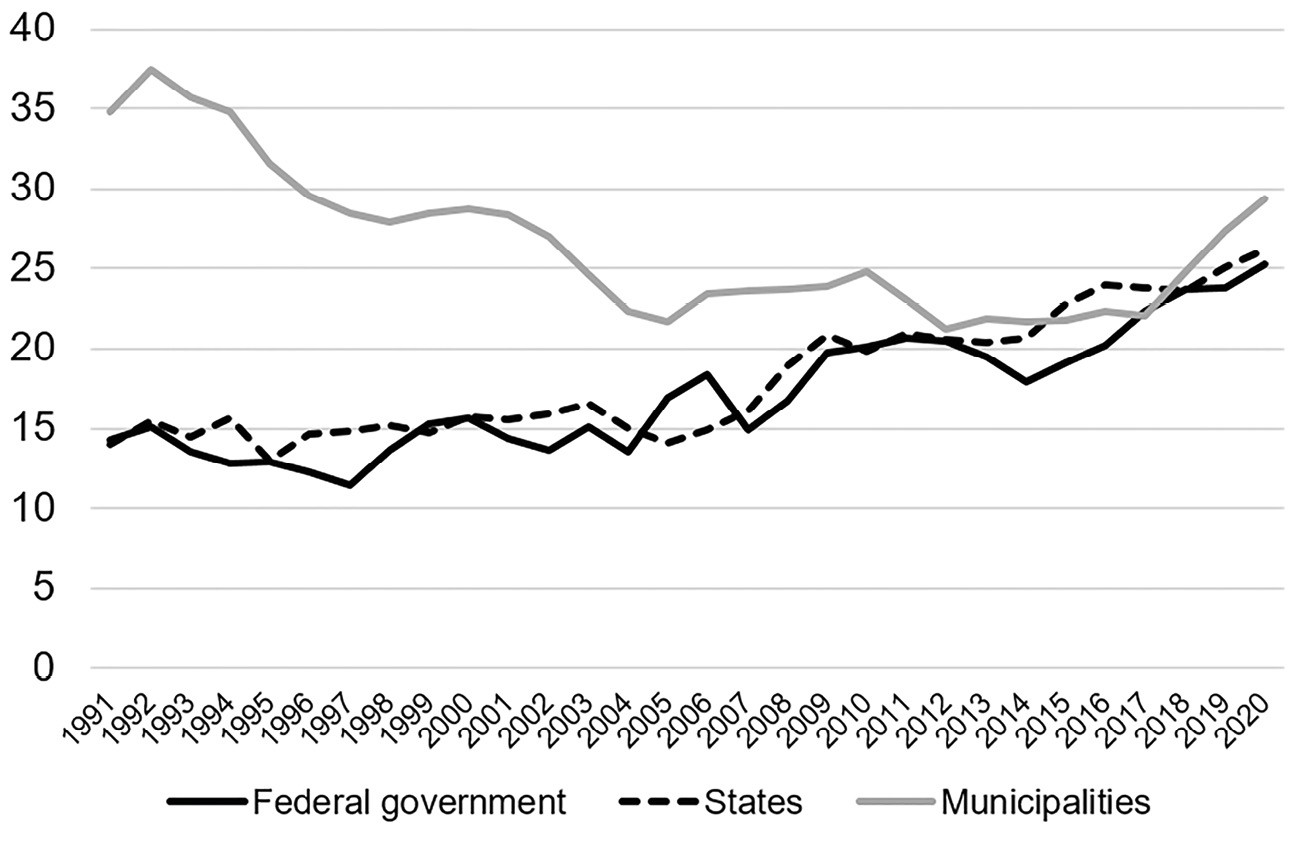

The public investment backlog is most pronounced in construction, where net investment has been negative since 2003. In 2015 the negative public construction investment trend was reversed, but depreciation still exceeded new construction investment in 2020. Insufficient infrastructure investment is largely a problem of the local government level, which is responsible―amongst other things―for schools, childcare facilities, and municipal roads, and accounts for about 60% of construction investment. Local government investment increased steeply after 2017, in parallel to rising investment grants both from the states and from federal programmes. However, after years of stagnating investment, the municipalities face serious bottlenecks. They have insufficient staff in their planning departments after years of job cuts and are confronted with capacity constraints in a booming construction industry (Scheller et al. 2021). Nevertheless, municipal investment, 85% of which is construction investment, rose by 33.3% in real terms (Figure 2). The national data conceal considerable regional disparities.

Developments since the first quarter of 2020 have been dominated by the COVID-19 pandemic and other one-off factors. Government construction investment declined two quarters in a row last summer, and is now slightly below the pre-crisis level and slightly below the level of twenty years earlier. In the second quarter of 2020, investment in machinery and equipment surged and declined again in subsequent quarters. According to Destatis, this temporary increase was due to a large defence project as well as regional spending on the railways. Overall, public gross fixed capital formation has lost some momentum in recent quarters.

Fig. 2 Annual Real Gross Capital Formation of Government Subsectors (in Billion Euros, Reference Year 2015).

Source of data: Destatis, Annual National Accounts, price adjustment by IMK using weighted deflators for government subsectors. Investment of social security is not presented, as it is negligible.

3.2 Investment Projects under the Stimulus and Future Investment Package: Limited Scope and Slow Progress

On 3 June 2020, the German government published its “stimulus and future package”. Its focus was on stabilising incomes and consumption, as well as businesses, in the COVID-19 crisis. Key elements were a temporary lowering of the VAT rate in the second half of 2020, a reduction of the renewable energy levy in 2021, and generous subsidies to support businesses adversely affected by the anti-COVID measures. In addition to the usual criteria of being timely, targeted, and temporary (Elmendorf and Furman 2008), the package also aimed to be transformative. This is why it is split into two parts: a stimulus package (“Konjunkturpaket”) and the future package (“Zukunftspaket”), a medium-term programme consisting largely of investment in key areas such as decarbonisation and climate-friendly mobility, digitalisation and the modernisation of the health sector. The total volume of quantified measures in both packages adds up to €171.6 bn, of which roughly €130 bn was supposed be effective in 2020–21 (BMF 2020; Dullien et al. 2020a).

As several measures were not quantified― e.g., the extension of the short-time work scheme beyond 2020―and subsidies to business as well as spending to contain the pandemic have repeatedly been upgraded, the overall volume of the package could be even higher. The measures of the Zukunftspaket amount to €57.9 bn, of which €43.9 bn is either direct public investment or investment grants.4 At the same time, the stimulus package includes investment totalling €13.9 bn. Overall investment in the stimulus and future investment package thus amounts to €57.8 bn, or roughly one third of the total quantified amount (Table 1).

At first sight, this looks impressive. However, in some cases, the planned implementation stretches beyond 2025, translating into an annual allocation in the single-digit billions of euros. Total investment in the stimulus and future investment package thus covers only about 12% of the requirements identified by the IMK and IW Köln in their joint report, which was endorsed by both the German Trade Union Confederation and the Federation of German Industries (Bardt et al. 2019). The order of magnitude of the institutes’ estimate, a total of €457 bn over ten years, was classified as “not implausible” by the Board of Academic Advisors at the Federal Ministry of Economic Affairs and Energy (BMWi 2020).

Furthermore, not all of the investment is additional. €10 bn of the package refers to planned investments of the federal government that were to be brought forward. If one looks at the statistics of the past year, there has not been much additional investment. According to the national accounts, gross capital formation of the federal government at current prices increased by just €1.9 bn in 2020.

Moreover, implementation is lagging in some areas. An example is the national hydrogen strategy, the largest individual item of the future investment package, with a total scope of €7 bn.5 Of this amount, less than €0.6 bn is to be disbursed until the end of 2021. As the package was only launched in mid-2020, it was clear that not too much could be achieved that year, but, at less than €0.4 bn, the plan for 2021 is also quite unambitious, after being scaled down from €1.7 bn in the original draft budget. This is all the more problematic if one takes into account that the government’s hydrogen strategy is far too small in dimension, compared to what would be needed. A recent working paper by Tom Krebs of the University of Mannheim, one of Germany’s leading experts on investment, calls for a much more ambitious hydrogen strategy combining massive infrastructure investment (both in Germany and across Europe) and industrial policies. With an overall budget of €100 bn until 2030, it would be more than eight times the size of the current plans. More importantly, it envisages a much more active role of the government and substantial hydrogen production within Germany, which is seen as a prerequisite for sustaining Germany’s technological leadership position (Krebs 2021).

When assessing the impact of the stimulus measures on investment, it is insufficient to look only at direct investment expenditures in the packages, as some measures have a beneficial indirect effect. As the municipalities play a central role in German infrastructure investment, their financial situation is vital. Depending strongly on the highly cyclical trade tax (Gewerbesteuer), the municipalities would have had to cut spending, investment in particular, if the federal and state governments had not reimbursed the revenue losses of the trade tax fully in 2020.6 In addition, the federal government raised its reimbursements of municipalities’ expenditure on accommodation and heating for long-term unemployed people substantially and permanently. This enabled the municipalities to continue investing strongly, albeit at a slightly slower pace than in the two preceding years, most probably also because of restrictions in the pandemic. As revenue losses continue in 2021, with federal and state governments not planning to compensate the municipalities for their revenue losses again, it remains to be seen whether the municipalities can sustain their dynamic investment activity.

3.3 German Recovery and Resilience Plan: Substantial Overlap with Stimulus and Future Package

In a major step forward for European integration, in late 2020, after fraught negotiations, the member states agreed to set up a Recovery and Resilience Facility (Watzka and Watt 2020). Under the scheme, the European Commission is empowered to borrow, on behalf of the EU, hundreds of billions of euros on financial markets. Up to €672.5 bn is to be made available to member states, roughly half as grants, and the other half as loans. The money is to be spent on agreed priorities. The mechanism, in a nutshell, is for member states to submit national plans which are approved first by the Commission, then the Council. Funds are then disbursed, providing member states achieve agreed milestones. Disbursement and programme expenditures are foreseen to run until 2026. The member states have committed to servicing these debts over the long term (until 2058) via the EU budget―if agreement can be reached by means of new “own resources”.

Germany submitted a first draft of its national plan at the end of 2020, and the final version―Deutscher Aufbau- und Resilienzplan (DARP)―on 27 April 2021. It runs to 1250 pages. Germany is seeking funding only under the grants pillar of the RRF: it is not applying for RRF loans, as the servicing costs of such loans are not lower than Germany can currently obtain on financial markets. The discussion here focuses on aspects that can be considered, in a broad sense, as public investment;7 planned reforms are not discussed.

3.3.1 Overview of the DARP

For Germany, the volume for grants available under the RRF is small. It is estimated to be €23.6 bn in 2018 prices and €25.6 bn in current prices; this is less than 0.8% of annual GDP (2020) and will be spread over a period of six years (2021–26). In macroeconomic terms, the RRF is of limited direct importance for Germany, much less than the domestic stimulus and recovery package. This reflects both the fact that the RRF is strongly redistributive in favour of low-income member states and those hardest hit by the pandemic (Watzka and Watt 2020) and also Germany’s decision to forgo the loans component. The country also benefits indirectly, however, via the boost the RRF gives to its close trading partners.

The German government puts a value of just under €28 bn on the forty measures brought together in the DARP, for which it is seeking EU funding. These are divided into six priorities which are structured a little differently, but overall are congruent with the six policy areas set out in the RFF. They are:

- Climate and energy

- Digitalisation of the economy and infrastructure

- Digitalisation of education

- Strengthening social inclusion

- Strengthening the health system, especially related to pandemics

- Modern administration/removing investment barriers

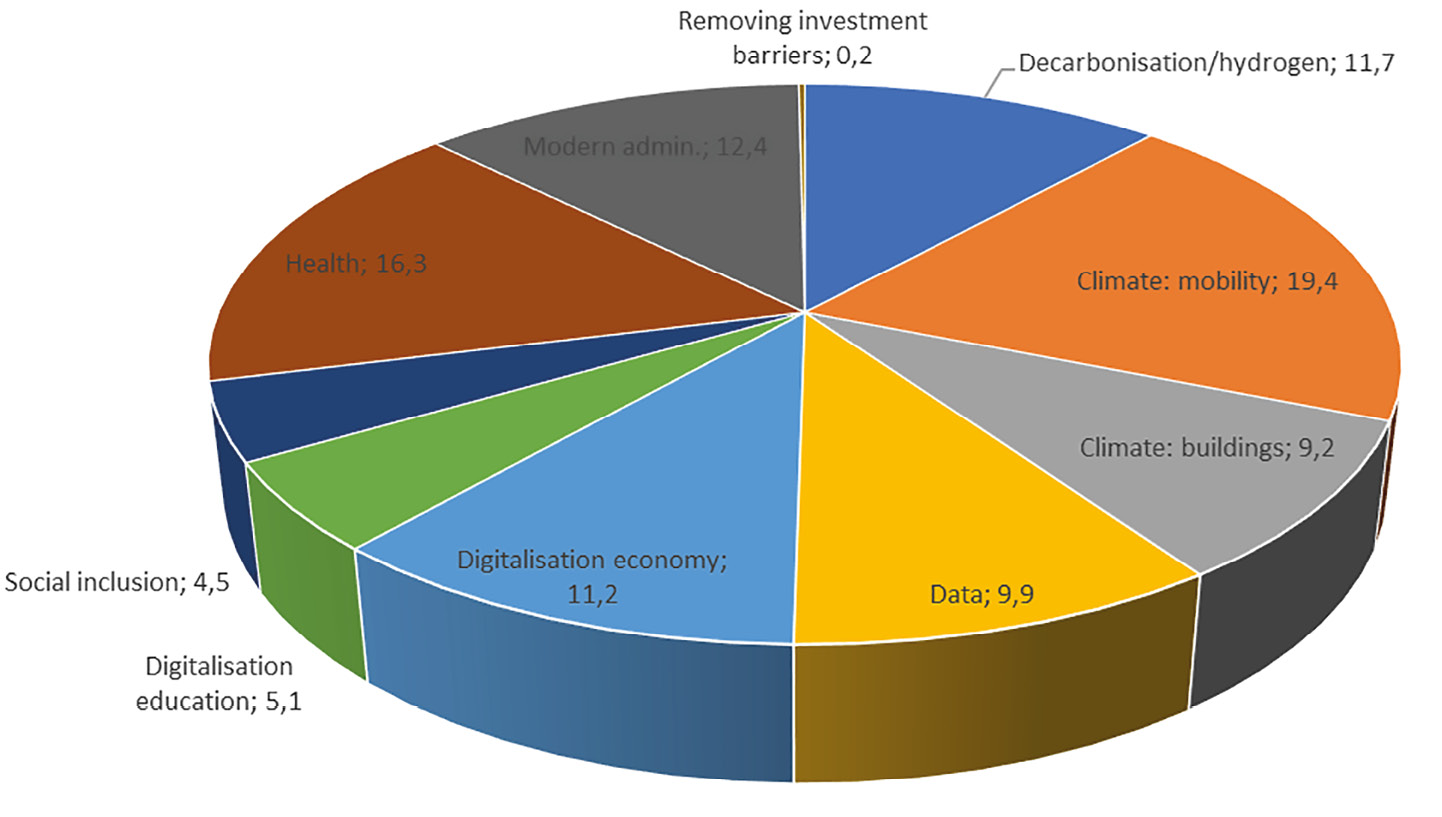

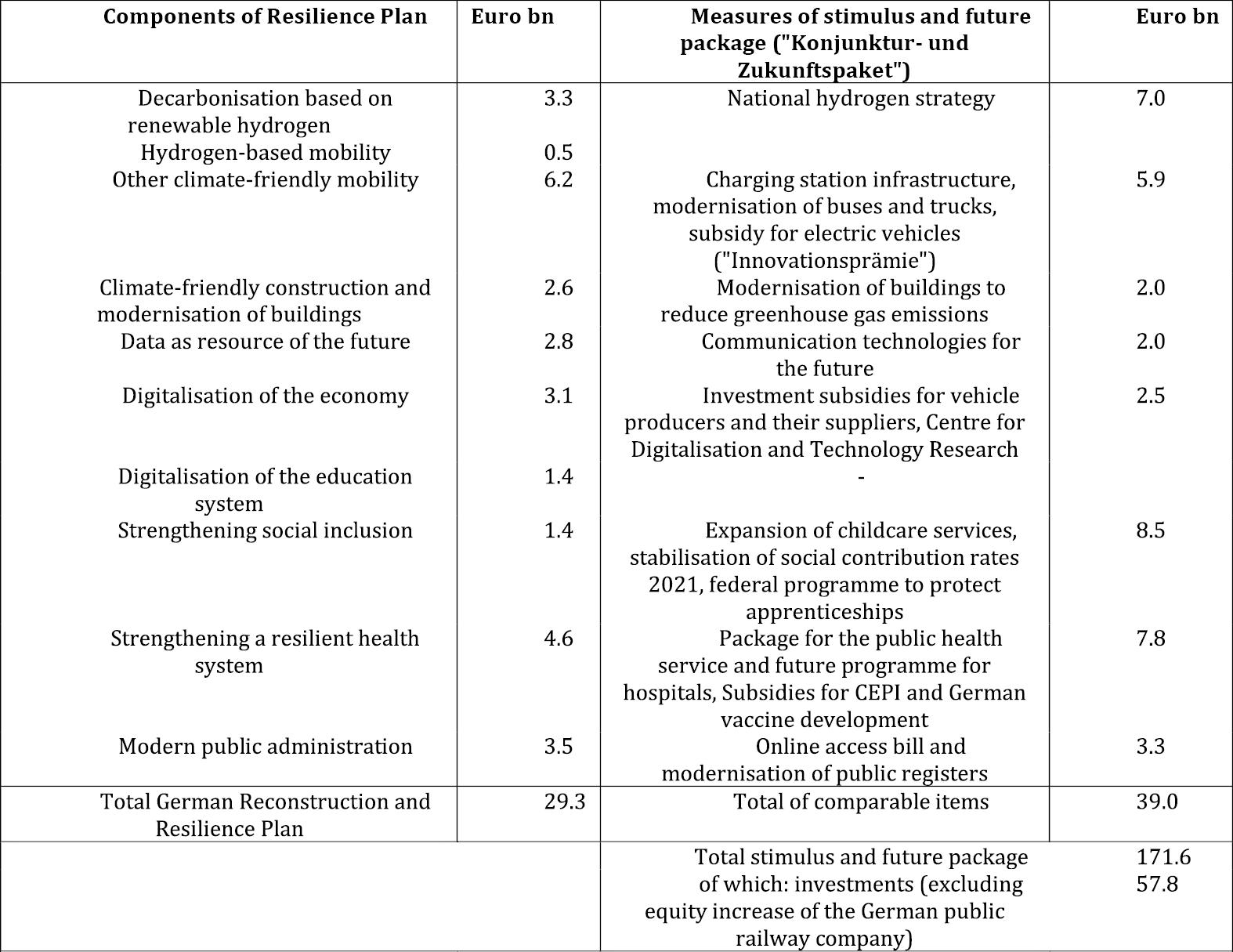

An overview of the division of planned expenditures between these six priorities (and some of the most important subcategories) is given in Table 1―which also shows spending plans in the national “stimulus and future package”―and in Figure 3.

Fig. 3 Contribution of Main DARP Sections to Total Expenditure, in %.

Source of data: DARP, p. 10.

Table 1 Comparison of German RRF and Domestic Stimulus Plan.

Source of data: German Reconstruction and Resilience Plan (Deutscher Aufbau und Resilienzplan, DARP), Written Statement of the German Council of Economic Experts on DARP, Table 7 of Annex, simplified and aggregated presentation of IMK, German Federal Government (2020).

EU rules stipulate that at least 37% of expenditure of the RRF should be on climate-protection projects; 20% is to be devoted to digitalisation. According to the German government, more than 40% of DARP-spending is concentrated in the first priority, climate/energy. Regarding digitalisation, Germany has made this goal explicit in pillars two and three of the DARP, which total more than 25%. Because digitalisation has been “mainstreamed” across other thematic areas, Germany claims that as much as 50% of spending under the DARP will contribute to the digitalisation goal.

There is considerable scope for applying false labels―“greenwashing”―and double-counting in such claims. With this in mind, we take a closer look at the main proposed projects. To simplify the exposition, Chapters 2 and 3, and 5 and 6 are considered together.

3.3.2 Climate and Energy

The climate and energy pillar consists of three packages of measures: decarbonisation with a focus on renewable (green) hydrogen, efforts to promote climate-friendly mobility, and construction/housing. Representing 40.3% of the total, it is, by a considerable margin, the most important section of the DARP.

A total of €3.26 bn is allocated to decarbonisation. Notable is the cooperation with, in particular, France on developing electrolysis capacity to produce green hydrogen and distribute it to end-users. (By contrast, the DARP does not offer support for other mature renewable power sources such as wind and solar power.) But even with the addition of hydrogen-related research and innovation funding, only €2.2 bn is set aside to develop a technology that is still in its infancy. While the priority given to this area is appropriate, funding appears derisory (as already noted above for the national stimulus and future package). Similarly, the offer of carbon contracts for difference, in which the government subsidises firms undertaking long-term carbon-reducing investments that are not currently profitable at present carbon prices, is a promising approach. Against the background of political barriers to an adequate carbon price and the lack of a border-adjustment mechanism, it has a direct impact in carbon-intensive industries, and also substantial indirect effects, as it aids the breakthrough of new technologies. However, it is set up as a pilot scheme and has a budget of only a little over half a billion euros. For context: one study suggests that decarbonising part of the German steel industry alone (shifting the so-called primary route to hydrogen-based reduction) would require, in addition to a massive expansion of renewable energy supply, some €30 bn euros of investment by the steel companies themselves (Berger 2020).

What is striking about the section on climate-friendly mobility is the almost complete focus on road transport. Only €227 m of the €5.4 bn envisaged to promote climate-friendly mobility is dedicated to improving rail transport. And even that is focused narrowly on engine technology: there is no place for a more general expansion of the rail network or train services.8 Local public transport is included only via a subsidy program, albeit a sizable one (€1 bn), to purchase electric buses. Overwhelmingly, the aim of the policies in this section of the DARP is to promote the electrification of private motorised transport. Almost half (€2.5 bn) of the total is foreseen as an “innovation premium” of €9000 for new purchases of electrical vehicles (plug-in hybrids up to €6750). Not a single euro is foreseen to promote cycling—for instance, by improving inner-city cycling infrastructure or increasing the use of bikes for commuting.

While it is a valid policy goal, for economic and social reasons, to manage the transition of the German car industry from internal combustion engines, the almost complete focus on it at the expense of other interests is regrettable. A study by the Forum Ökologische Marktwirtschaft (2021) notes that the DARP represents an improvement on the original version of the plan which, notably, contained more than €1 bn in subsidies to upgrade heavy goods vehicles to lower-emission diesel engines. This expensive subsidy to fossil-fuel road transport was removed, primarily because it was thought likely to be rejected due to the “do no significant (environmental) harm” injunction applying to all RRF-funded measures (DARP, p. 1071). While the promotion of electrical vehicles is an important element in achieving climate goals―assuming a parallel move to decarbonise electricity generation9―the subsidisation of the acquisition of new vehicles and the expansion of the charging network primarily benefits upper-income households and firms providing company cars.

The section on climate-friendly construction/renovation is dominated by a €2.5 bn subsidy for renovation of buildings to reduce their energy use through insulation, and allow for the modernisation of heating systems, etc. This is to be used to expand an existing national scheme, permitting an estimated 40,000 additional housing units to benefit.

3.3.3 Digitalisation of the Economy and Infrastructure, and of Education

These two chapters of the DARP represent around €5.9 bn and €1.4 bn respectively, together more than a quarter of the DARP. German political discourse, accentuated by the experience during the pandemic, has been seized by the view that Germany lags behind its peers in terms of digitalisation. Germany is attempting via an IPCEI initiative10 to develop its (and Europe’s) potential in the areas of microelectronics (started in 2018) and, more recently, cloud infrastructure, to gain a foothold in these areas.

The most striking feature of the digitalisation of the economy section, however, is the quantitative predominance―at almost €1.9 bn―of support for a very specific sector, the automobile industry, which as shown above is also a prime beneficiary of projects under the climate pillar. Policymakers justify this focus (DARP, p. 455) with reference to the huge challenges facing the sector to shift to electric vehicles and to cope with cost competition, particularly among part-supplying SMEs. It is difficult, though, to see why this is really support for “digitalisation” rather than sectoral investment support, focused on a strategically important sector. On the other hand, this part of the DARP does contain an investment in rail infrastructure (identified above as missing from the mobility section) in the form of digitalisation of rail signalling and communication systems (€500 m).

The experience of the pandemic, with pupils forced to learn at home for extended periods, and local authorities and even individual schools forced to seek individual workarounds, has certainly revealed the need for a “digital education offensive”. The programme is of very modest size, however. Alongside the purchase of equipment for teachers and investment in their skills development (€500 m), it contains elements whose priority is not immediately obvious, such as support for the educational institutions of the German army (€100 m). The largest single project (€630 m) is to set up a “meta-platform” to systematise and improve access to digital educational content. The focus on the “meta” level―and the associated nebulous description of what this measure can achieve in practice―reflects the fact that, in Germany, education is the prerogative of the federal states.

3.3.4 Social Inclusion

The foreseen measures are small in volume, with a strong focus on children and young people, an explicit goal of the EU-level RRF. The two quantitatively most important schemes are to improve childcare (€500 m) and ensure an adequate supply of apprenticeships/dual training courses, particularly for disadvantaged groups. A goal is to increase labour market participation, and indirectly also to contribute to undergirding the pension system, one of Germany’s country-specific recommendations. In the case of childcare, the funds will enable investment needs that have become more acute due to the pandemic to be met. The apprenticeship promotion programme offers financial support to companies who, despite the impact of the pandemic, take on additional trainees (including, for example, those who have lost their trainee placement in another company as a result of the crisis).

In short, these are sensible programmes that respond to real needs rendered more pressing by the pandemic; however, the quantitative dimensions are very limited.

3.3.5 Strengthening the Health System and Modernising Public Administration

It goes without saying that the COVID-19 pandemic threw down huge challenges to national health systems. Just over 16% of DARP is allocated for health-related measures. Specifically in the case of Germany, problems with inadequate digitalisation became apparent, leading to delays in processing tests and patchy reporting on the progress of the pandemic, and a lack of coordination between local health authorities. In view of this, more than €800 m is foreseen to be invested in this area.

Germany―the home of BioNTech, whose vaccine (produced in cooperation with Pfizer) has been the mainstay of the European vaccination campaign―plans to invest an additional €750 m in COVID-vaccine research and development under the DARP. By a substantial margin the largest programme in this area, at €3 bn, it is a “future programme” for hospitals. The program is to be “frontloaded”, with spending concentrated in 2021; the corresponding legislation was already passed last year. Here, the main aim is to improve the digitalisation of hospitals. They will be able to claim financial support for the necessary physical and human-capital investment. This is arguably one programme where a specific need, occasioned by the recent crisis, has been identified, and a commensurately substantial sum set aside to address the issue; this programme alone represents around 10% of the entire DARP.

The considerations detailed in the specific case of the public health system apply more generally to the German public administration; the problems of a reticent adoption of digital hardware and processes are the same. Similarly, therefore, a programme has been launched to address these problems through investment in physical and human capital. Here, too, the main element is a €3 bn support programme for investment in digitalisation, to make it user-friendly for citizens while dealing with the complexities of Germany’s three-layered federal administrative system. Additionally, two specific initiatives have been launched, whose aim is to enable citizens to identify themselves in online communication with the administration, while avoiding data-protection pitfalls and abuse by criminals, and permitting interoperability between different parts and levels of the administration; a first crucial step is to have a single identification number for each citizen.

As in other areas, this section of the DARP is doubtless focused on an important reform area, one also identified as part of the European Semester in the country-specific recommendations. However, the specific contribution (and additionality) of the DARP is questionable. The legislative processes have been underway for many years in some cases. The corresponding investments are now being, to some extent, booked under the DARP, but they would have proceeded under purely national financing in the absence of the RFF.

3.3.6 Overall Assessment

The DARP (p. 1103) contains a study undertaken by the DIW research institute, according to which long-run GDP is expected to be almost 2% higher than in the absence of the programme. The counterfactual here, though, is that the measures enumerated under the DARP are otherwise not implemented (full additionality). The overlap between the national stimulus and future programme and the DARP measures is very substantial, however. For Germany, the RRF has very largely not been perceived as an opportunity to take on additional tasks or increase the ambition of planned projects. Already planned projects, which would otherwise have been funded by domestic borrowing, are now to draw on RRF funding.

As regards prioritisation, in broad-brush terms the DARF is in accordance with the required focus on climate change and digitialisation. Indeed, the latter is like a red thread running through much of the programme. This is in accordance with recent country-specific recommendations issued to Germany by the EU, and reflects perceived weaknesses revealed by the pandemic.

A more granular look, however, reveals some issues of concern. Striking is the focus, under the “green” and “digital” labels, on the automobile sector. While there are economic and social justifications supporting what is clearly a far-reaching adjustment in a strategically important sector, the neglect of other modes of transport stands out. Some measures, such as subsidisation of plug-in hybrid cars, are arguably inimical to environmental goals. An admittedly speculative interpretation is that this represents, in part, an attempt to show that “Europe” is supporting the German car industry against the background of criticism that EU-imposed fleet emission requirements have placed a heavy burden on German automobile production. In other areas (such as the hydrogen economy and support for industrial decarbonisation) envisaged measures are appropriate, but the scale of funding is very limited.

3.4 Substantially Higher Credit-Financed Public Investment Does Not Threaten Debt Sustainability

Some insight into the likely effects of additional public investment, whether under the purely domestic budget or as part of the German recovery plan, can be gained from a recent simulation of a credit-financed investment programme conducted by the IMK (Dullien et al. 2021).

Based on conservative estimates of unmet infrastructural needs (Bardt et al. 2019), the authors simulate a public investment programme totaling €460 bn (in 2019 prices, equal to around 13% of 2019 GDP) over ten years. At the end of the period, the public capital stock is about 25% higher than without the programme. The simulation is conducted using the macroeconomic model NiGEM. The investment is credit-financed. No monetary policy reaction is assumed during the first two years. The simulation runs for thirty years.

The simulations use three different assumptions. The first is with the standard version of NiGEM: here, the public and private capital stocks act as substitutes. The larger public capital stock depresses the marginal productivity of the entire capital stock. As this is neither theoretically not empirically plausible, two illustrative alternative simulations were undertaken. In a technological-improvement scenario, the rate of technical progress is assumed to be boosted by the higher public investment (for instance, due to the provision of a better broadband network). Secondly, in a more far-reaching intervention, the output-elasticity of the public capital stock is set at 0.3, in line with empirical evidence in the literature.

In the basic scenario, in which the short-run fiscal multiplier is only around 0.8%, substantially below most estimates in the current low-interest-rate environment, GDP is around 1.7% higher at the end of the programme compared to baseline. In the longer run, the multiplier is higher―around 2%, in line with much of the recent literature―and the GDP effect is substantial at 3–4%. Private investment is crowded in, the total capital stock is some 4% above baseline, and potential output is about 3% higher. The additional credit-financed investment means that initially the debt-to-GDP ratio is some 10 pp higher than without a programme. But this one-off cost is matched by permanently higher potential output. Because of this, the debt-to-GDP ratio is the same as without the programme at the end of the thirty-year simulation period. Even with low multipliers, the impact is positive: output is higher while the debt-to-GDP ratio is the same as without the investment offensive.

The positive impacts on output and potential growth are substantially higher in the two alternative simulations. Accordingly, the period after which the programme is self-financing (in the sense of a debt-to-GDP ratio no higher than baseline) is substantially shorter. While there is clearly considerable uncertainty about the real-world size of the multiplier, which in practice would depend, not least, on exactly which sorts of public investment received additional impetus, the two alternative simulations are considered more plausible and the quantitative effects given above are likely at the bottom of the plausible range.

The implications of this simulation are clear. Germany has substantial scope to increase credit-financed public investment with positive economic impacts and no longer-run negative effects on debt-to-GDP ratios. This could be done purely domestically or, if the financial terms become favourable, by taking up the loans available under the RFF.

3.5 What Germany Needs after the COVID-19 Crisis: Reform of Fiscal Rules and Stabilisation of Investment at a High Level

In parallel to the European Union’s upgrade of its climate goals, the German government also raised its ambitions, aiming to reach climate neutrality by 2045. On top of already considerable investment needs, this requires even more capital spending much earlier. The investment projects of the stimulus and future package cover only a fraction of Germany’s massive investment requirements. The Recovery and Resilience Plan is even smaller in size and overlaps substantially with the national stimulus and future investment package; it therefore provides only limited additional investment. This is not a problem in itself: it is right that the EU RRF has a strongly redistributive function and supports states hit hardest by the COVID-19 crisis. Germany has the means to do much more on its own.

From early on in the COVID-19 crisis, both the European fiscal rules and the German debt brake were suspended, which allowed both federal and state governments to incur substantial additional debt to fight the crisis. While nobody knows when the pandemic will finally be over, the debate about fiscal consolidation after the crisis is already in full swing and was a key issue in the autumn general election. There is a high probability that there will be neither substantial reforms of the debt brake nor tax increases to finance the massive additional investment requirements. Current discussions of financing options focus on a variety of measures ranging from making use of public companies to cutting ecologically harmful subsidies. This are unlikely to be enough, however.

Germany and the whole of the EU needs a sustained investment strategy. In Germany, public investment, which has recently been determined much more by the availability of current revenues than an assessment of longer-run needs, must be stabilised at a satisfactory level in the medium- to long-term. This is particularly important for the municipalities, which play a vital role for infrastructure investment. They will only employ the additional staff needed to implement investment projects if they receive sufficient funds on a permanent basis instead of having to rely on successive small-scale federal programmes. This would also provide the planning certainty that the construction industry needs to increase its capacities. As the municipalities receive substantial investment grants from the states, they are also affected indirectly by the debt brake, which prevents federal states taking on any new debt in normal times.

The federal level has slightly more fiscal space, being allowed to incur structural debt of 0.35% of GDP per year. This is only about a quarter of the additional requirements. Furthermore, the current cyclical adjustment method tends to underestimate cyclical effects and thus has a procyclical bias (Heimberger 2020; Heimberger and Truger 2020).

At EU level, the current economic governance review should be used to modernise the fiscal rules. A viable option would be an expenditure rule combined with a “golden rule” for investment as proposed by Dullien et al. (2020b). At the same time, the debt limit of 60% of GDP should be defined more flexibly, taking account of the macroeconomic environment (especially negative real interest rates). This would also be a good opportunity to reform the German debt brake, which in many respects is not fully consistent with the European rules (Dullien et al. 2021, pp. 18–19).

References

Bach, S., G. Baldi, K. Bernoth, B. Bremer, B. Farkas, F. Fichtner, M. Fratzscher and M. Gornig (2013) Wege zu einem höheren Wachstumspfad, DIW Wochenbericht 26: 617.

Bardt, H., S. Dullien, M. Hüther and K. Rietzler (2019) For a Sound Fiscal Policy: Enabling Public Investment, IMK Report 152e, November. Düsseldorf.

Berger, R. (2020) “The Future of Steelmaking: How the European Steel Industry Can Achieve Carbon Neutrality”, Roland Berger Focus, 05/2020, https://www.rolandberger.com/publications/publication_pdf/rroland_berger_future_of_steelmaking.pdf.

BMWi (2020) Öffentliche Infrastruktur in Deutschland: Probleme und Reformbedarf Gutachten des Wissenschaftlichen Beirats, Bundesministerium für Wirtschaft und Energie, Berlin.

Bundesministerium der Finanzen, BMF (2021) Vorläufiger Abschluss des Bundeshaushalts 2020, BMF-Monatsbericht, January.

Bundesministerium der Finanzen, BMF (2020) Corona-Folgen bekämpfen, Wohlstand sichern, Zukunftsfähigkeit stärken, Ergebnis des Koalitionsaus-schusses vom 3. Juni 2020, Berlin.

Dullien, S., K. Rietzler and S. Tober (2021) Ein Transformationsfonds für Deutschland, IMK Study 71, January.

Dullien, S., E. Jürgens, C. Paetz and S. Watzka (2021) Makroökonomische Auswirkungen eines kreditfinanzierten Investitionsprogramms in Deutschland. IMK Report 168.

Dullien, S., S. Tober and A. Truger (2020a) “Wege aus der Wirtschaftskrise: Der Spagat zwischen Wachstumsstabilisierung und sozial-ökologischer Transformation”, WSI Mitteilungen, 73, June 2020.

Dullien, S., C. Paetz, A. Watt and S. Watzka (2020b) Proposals for a Reform of the EU’s Fiscal Rules and Economic Governance, IMK Report 159e, Düsseldorf.

Dullien, S., E. Jürgens and S. Watzka (2020c) ”Public Investment in Germany: The Need for a Big Push”. In F. Cerniglia and F. Saraceno (eds) A European Public Investment Outlook. Cambridge: Open Book Publishers, pp. 49–62, https://doi.org/10.11647/obp.0222.03.

Deutscher Bundestag (2020) Beschlussempfehlung des Haushaltsaus-schusses (8. Ausschuss) zu dem Entwurf eines Gesetzes über die Feststellung des Bundeshaushaltsplans für das Haushaltsjahr 2021 (Haushaltsgesetz 2021)―Drucksache 19/22600―Einzelplan 60. Bundestagsdrucksache 19/23323. Berlin.

Elmendorf, D.W. and J. Furman (2008) “If, When, How: A Primer on Fiscal Stimulus”, The Hamilton Project Strategy Paper, Brookings Institution: Washington, DC.

Forum Ökologische Marktwirtschaft (2021) Deutscher Aufbau- und Resilienzplan: Verpasste Chance für eine klimafreundliche und soziale Mobilität, Policy Brief, aktualisierte Version 28.04.21.

Heimberger, P. (2020) “Potential Output, EU Fiscal Surveillance and the COVID-19 Shock”, Intereconomics 55(3): 167–74, https://doi.org/10.1007/s10272-020-0895-z.

Heimberger, P. and A. Truger (2020) Der Outputlücken-Nonsense gefährdet Deutschlands Erholung von der Corona-Krise, https://makronom.de/der-outputluecken-nonsense-gefaehrdet-deutschlands-erholung-von-der-corona-krise-36125.

Scheller, H., K. Rietzler, C. Raffer and K. Kühl (2021) “Baustelle zukunftsfähige Infrastruktur: Ansätze zum Abbau nichtmonetärer Investitionshemmnisse bei öffentlichen Infrastrukturvorhaben”, Friedrich Ebert Stiftung, Wiso-Diskurs 12/2021.

Watzka, S. and A. Watt (2020) The Macroeconomic Effects of the EU Recovery and Resilience Facility, IMK Policy Brief 98, October 2020, Düsseldorf, https://www.imk-boeckler.de/de/faust-detail.htm?sync_id=9110.

1 Data as of early August 2021.

2 Since the introduction of the ESA 2010 in 2014, public investment in machinery and equipment includes military spending on weapons.

3 Other investment consists mostly of investment in research and development.

4 The future investment package also includes measure such as additional staff in the health sector (€4 bn), humanitarian aid in the pandemic (€3 bn), or an equity increase for Deutsche Bahn (€5 bn), which mostly covers losses of the German rail company during the crisis.

5 With an additional €2 bn earmarked for international cooperation on hydrogen and €3 bn from European sources, the total hydrogen budget adds up to €12 bn (Krebs 2021).

6 Federal and state governments each bore half of the trade tax revenue losses. The Federal Ministry of Finance reported the federal share as €6.1 bn (BMF 2021).

7 In its analysis of the DARP (DARP, p. 1110), the DIW classifies around 61% of spending as either public investment or an investment subsidy. But a substantial proportion of what is termed government consumption in the naitonal accounts (just under 21% of DARP spending) can be considered investment in a broader sense (e.g., salaries of additional educational or healthcare staff).

8 But see also the section on digitalisation.

9 Plug-in hybrid vehicles are also eligible for support although their ecological impact is, to say the least, disputed.

10 Important Project of Common European Interest.