4. Relaunching Public Investment in Italy

© Giovanni Barbieri and Floriana Cerniglia, CC BY 4.0 https://doi.org/10.11647/OBP.0280.04

Introduction

The official outbreak of COVID-19 in Italy in March 2020 dealt a considerable blow to the national economy. Out of all the EU countries, Italy has suffered the most from the pandemic, and has experienced the worst contraction of its GDP since WWII. The economy has been further stressed by a reduction in consumption and a drop in tax revenues; furthermore, the health crisis has put the national healthcare system under severe strain. All of this has and will continue to contribute in the future to the redefinition of its budgetary policy.

However, 2020 was also a turning point for public investments in Italy, thanks to the widespread conviction that a robust socioeconomic structure, capable of resisting exogenous shocks such as those caused by the COVID-19 pandemic, can be obtained only by a thorough and consistent policy of tangible and intangible public investments. There are encouraging signs pointing in this direction. The new Italian government has not only planned an increase in public capital investments, but it has also committed to redefining the regulatory framework in many areas. These general policy objectives are strongly thought to be capable of jump-starting public investments in Italy, and overcoming the slow, cumbersome, and ineffective processes that have systemically affected Italy for more than two decades. At the European level, the COVID-19 pandemic has highlighted the limits of a rigorous conception of budgetary policy based solely on complying with the Stability and Growth Pact rules and with fiscal “austerity” rules. This is the foundation on which Next Generation EU (NGEU) has been developed and adopted. It is a programme which aims to relaunch the European economy through a massive plan of public investments in sectors that are considered strategic both for the survival of the economies of EU member countries and for the EU as a whole.

This chapter will provide an update of the data on public investments in Italy, which was presented and discussed in a previous work (Cerniglia and Rossi 2020). We will also address the measures taken by the Italian government to tackle the economic fallout caused by the pandemic, and consider the impact of NGEU funding on public investments in Italy in the coming years.

4.1 Public Investments in Italy

Public investments, which had declined from 3.7% to 2.1% from 2009 to 2018, gained new momentum in 2019 and 2020. In 2019, they went up to 2.3% of GDP. The increase in 2019 was in large part attributable to the measures adopted by previous governments that made it possible to overcome both the limits imposed by the Internal Stability Pact at different levels of government (regions and municipalities) and the freeze on spending surpluses. These two circumstances allowed the sublevels of government to release funds, thereby increasing their share of capital expenditure for infrastructure investments by an additional 20%.

In 2020, notwithstanding the slowdown due to the pandemic in the first half of the year, public investments increased from €41.4 bn to €44.2 bn. Due to a contraction in GDP, the investments-to-GDP ratio climbed to 2.7% (OCPI, 2021).1

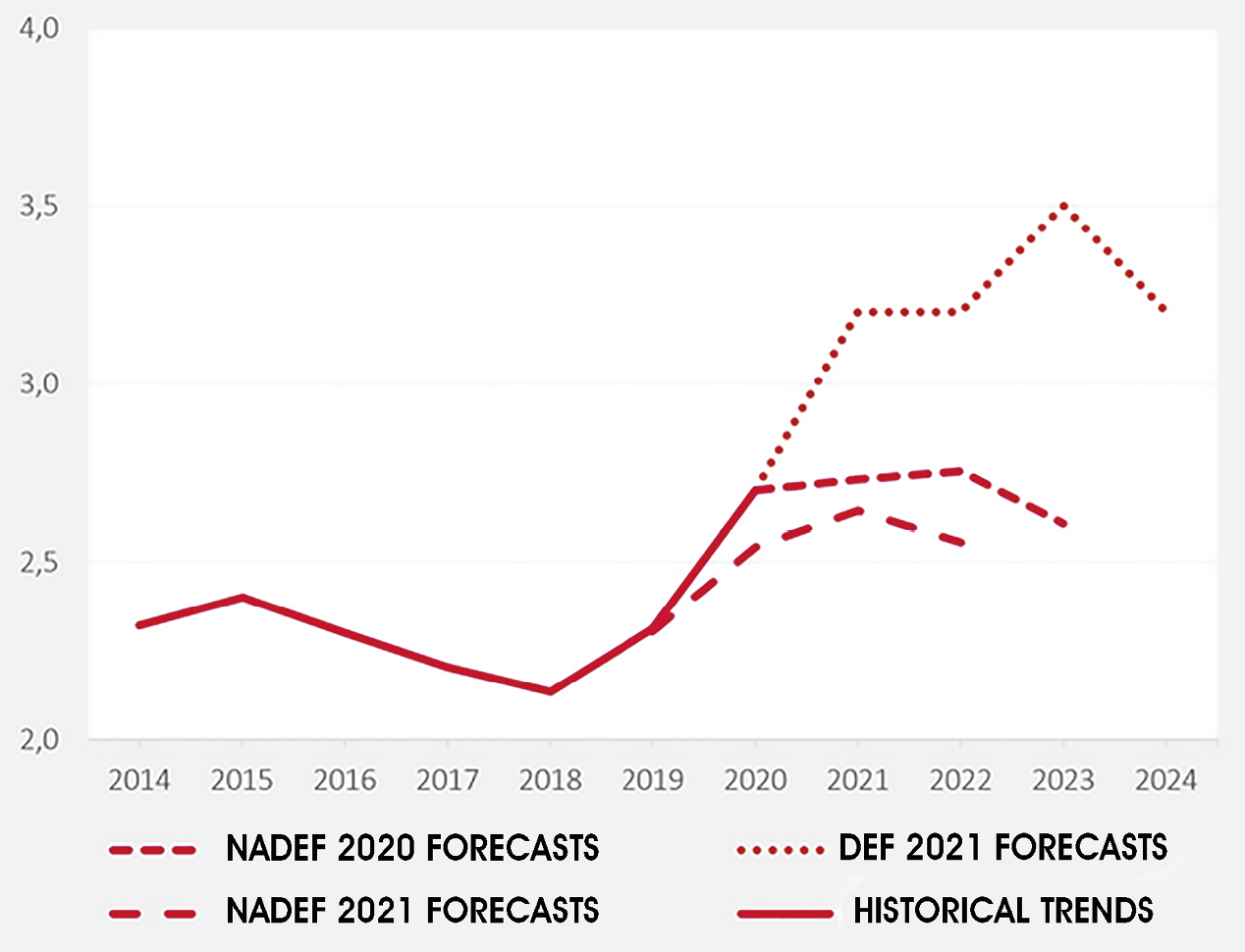

The state intends to continue its steady flow of public investments over the coming years, also with the help of the NGEU funds. The target for public investments in 2021 is €55.6 bn (3.2% of GDP). The DEF 2021 forecasts an increase to €62.9 bn by 2024 (3.2% of GDP). This level is higher than the average pre-pandemic level (3% for the period 1995 to 2009) and previous forecasts (NADEF 2019), as shown in Figure 1.

Fig. 1 Programmed Public Investments.

Source of data: OCPI (2021) on NADEF 2019, NADEF 2020, and DEF 2021 data.

More disaggregated data will be used to update the trends assessed in the previous work (Cerniglia and Rossi 2020). In this section, we will use the Conti Pubblici Territoriali dataset (hereafter CPT) released by the Italian Agency for Territorial Cohesion. We present data on capital expenditure by the Italian Public Administration (PA) and by the Enlarged Public Administration (Enlarged PA). The PA includes the central government as well as local and regional governments. EPA includes the PA and national and local public companies and utilities.2 The data cover 2017–18. The CPT data enable us to obtain a clear-cut picture of the share of capital expenditure in North-Central Italy and in the “Mezzogiorno”. Public capital expenditure consists of three components: 1) public investments (expenditure for infrastructure, machinery, and equipment) 2) money transfers, for example to private companies, public institutions, etc.; 3) shareholding and the provision of loans. The following tables and figures refer to capital expenditure without shareholding and loans.

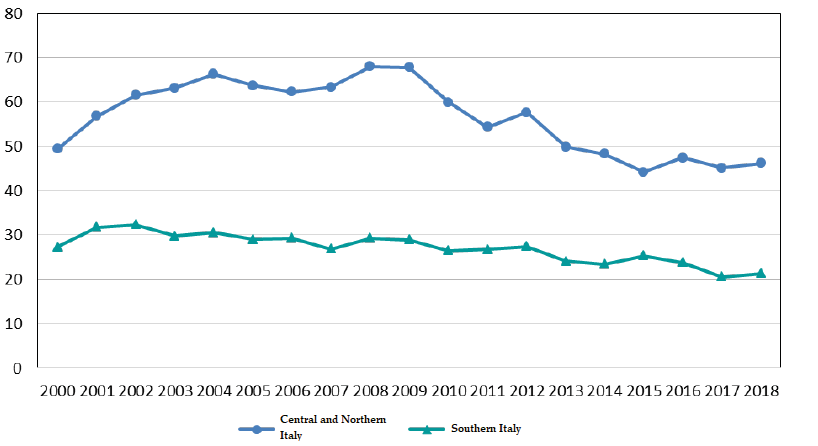

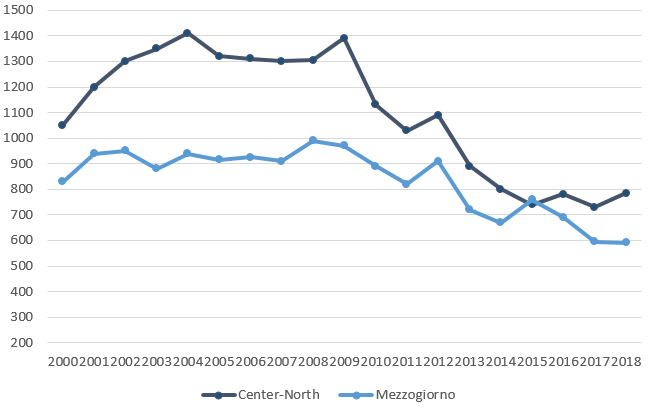

The capital expenditure in Italy of the Enlarged PA in 2018 amounted to €67.4 bn, a +2.7% increase from the previous year. In terms of macro areas, the figure can be broken down into €46.1 bn for the north-central area and €21.3 bn for the south, as shown in Figure 2.

Fig. 2 Capital Expenditure (billion euros at Constant 2015 Prices).

Source of data: CPT (2020).

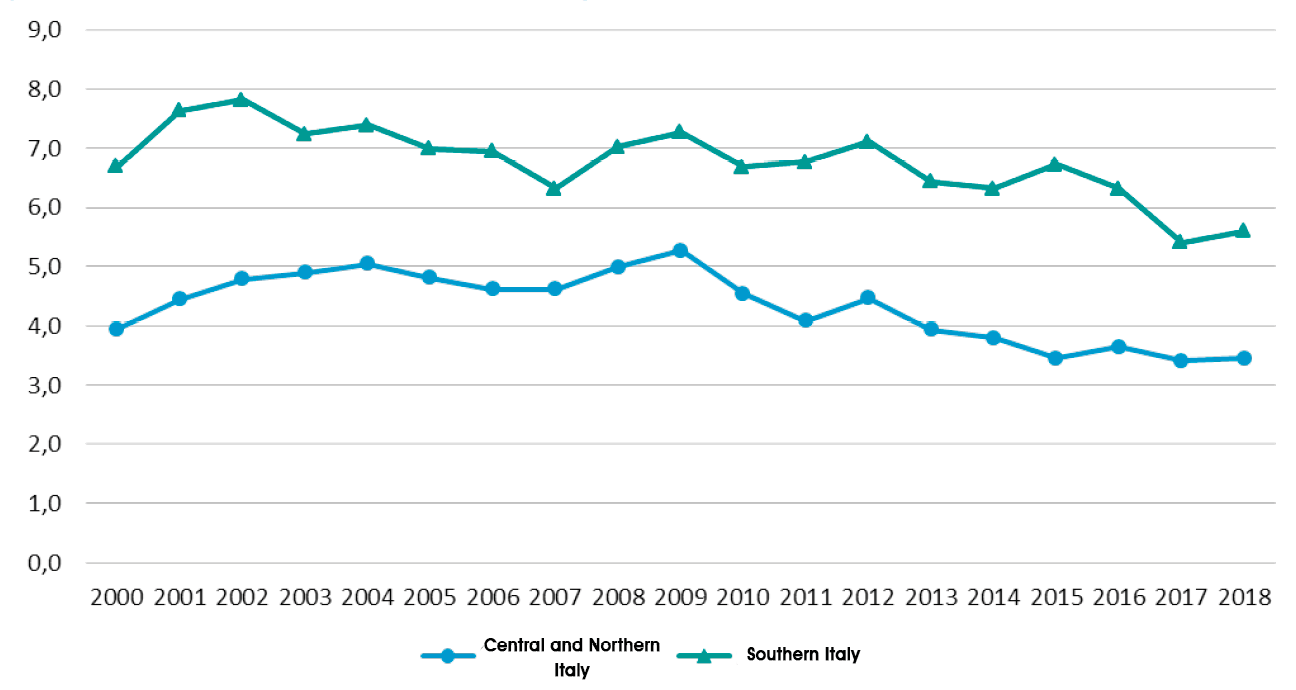

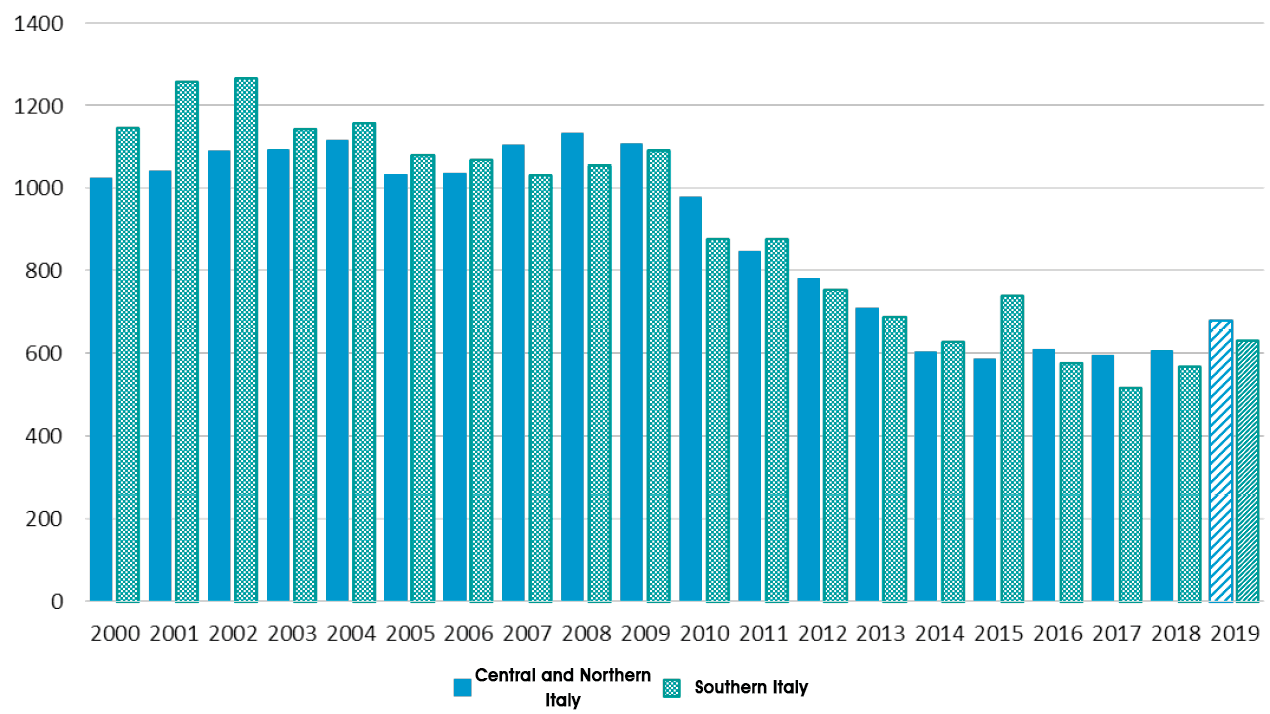

Looking at the per capita data, we see an increase in capital expenditure in both macro areas. In the north-central area there was an increase from €16,263 per capita in 2017 to €16,612 in 2018, with a real variation of +2.1%, while in the south it went from €12,403 per capita to €12.706 (+2.4%). Notice that the increase in capital expenditure follows an increase in GDP in both macro areas. In the “Mezzogiorno”, the capital-expenditure-to-GDP ratio was +5.4% in 2017 and +5.6% in 2018, as shown in Figure 3.

Fig. 3 Capital Expenditure (% GDP).

Source of data: CPT (2020).

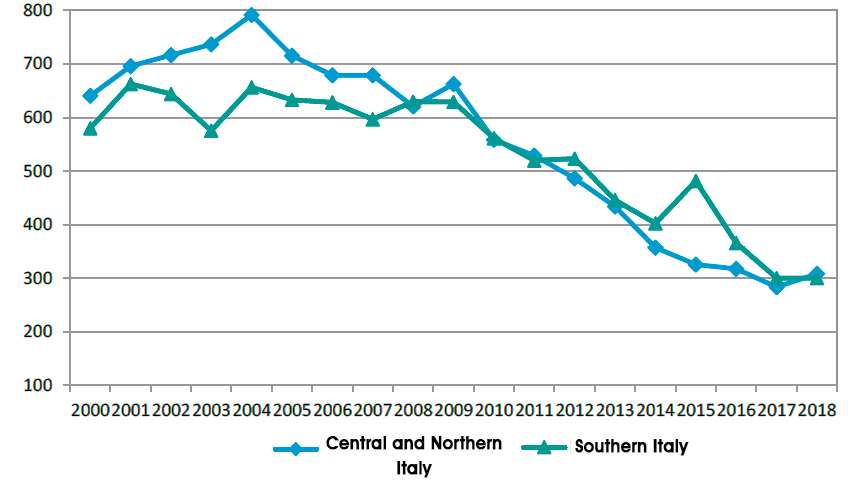

Figure 4 provides a snapshot of only public investments.

Source of data: CPT (2020).

In 2018, there was a +5% increase in investments in the Enlarged PA, bringing per capita expenditure back to €768. The largest increase in spending occurred in the energy sector (Eni, Enel).

In the “Mezzogiorno”, on the other hand, per capita investment expenditure remained stagnant at €583. This is mainly due to a decrease in investments by Anas, Poste Italiane, and local public utilities.

In the following graphs we now consider only the PA.

Fig. 5 Capital Expenditure by Macro Area.

Source of data: CPT (2020).

Note that at the territorial level (CPT 2020), the “Mezzogiorno” saw an increase of 23% in central government expenditure, but not much growth in expenditure by regional and local governments. The north-central area, on the other hand, registered an increase in expenditure by the central government (+11%) as well as by the regional and other sublevels of government (+14%).

Figure 6 shows the expenditure trend when considering only investments. In the north-central area in 2018, there was an +8.8% increase in investments compared to the previous year, mainly due to positive actions by regional and local governments. The “Mezzogiorno” stabilised, after its economic collapse in 2017, but with lower levels of investments by national and local public companies and utilities (CPT 2019).

Fig. 6 Capital Expenditure for Investments by Macro Area (Net of Financial Items).

Source of data: CPT (2020).

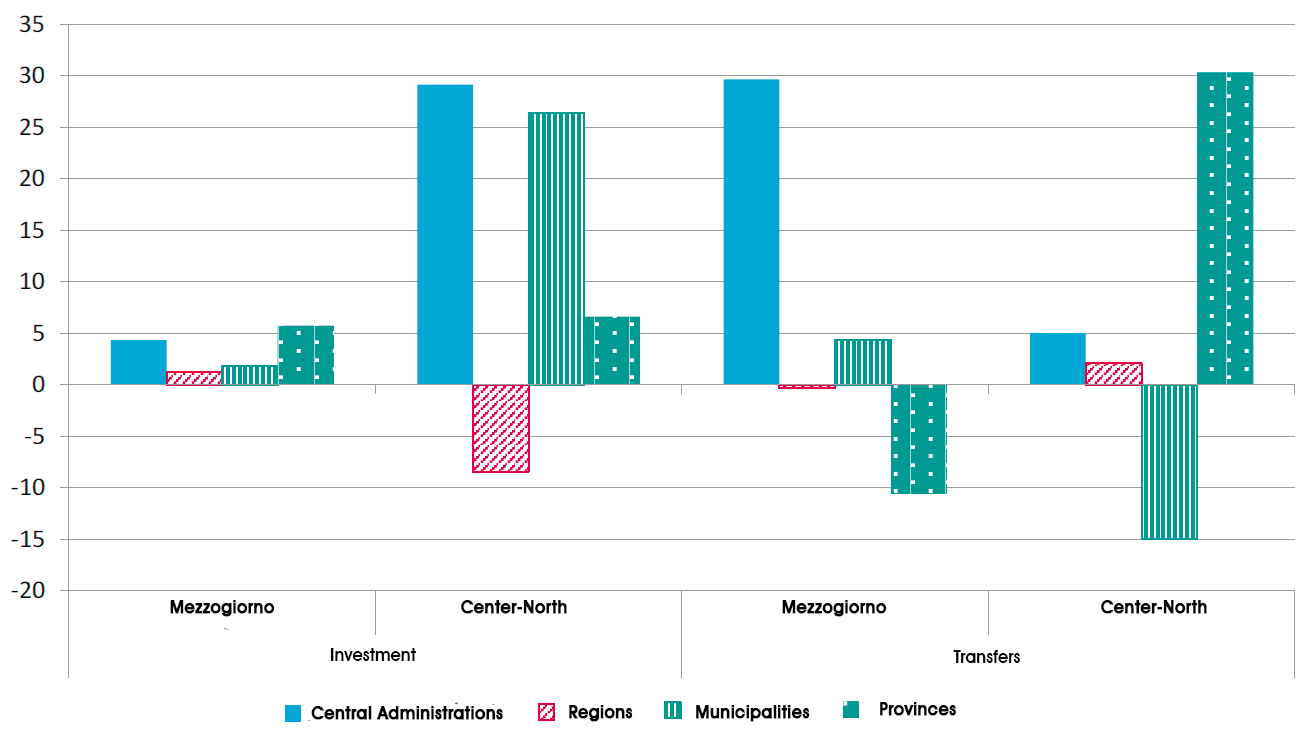

Last, Figure 7 shows the variations in investments and transfers for 2017 and 2018 across the macro areas and levels of government.

Fig. 7 Variations in Expenditure in 2017 and 2018 for Investments and Transfers in the Main PA Compartments by Macro Area (Calculations Based on Constant 2015 Prices).

Source of data: CPT (2020).

The increase in expenditure by the central government in the “Mezzogiorno” was limited for investment (+4.4%), but significant for transfers to households and businesses (+29.7%).

In the north-central area, the positive trend of the central government’s expenditure in investment and transfers was inverse to that of the south: investment expenditure grew by +29% while transfers increased by +5%. When considering the sublevels of government, there was considerable stability in both investment and transfer expenditures in the south (+1.3% and -0.3%, respectively), while the north-central area saw a contraction in investment expenditure (-8.4%) and limited growth in transfers (+2.1%).

Municipal expenditure was positive, though limited, in the south for both investment and transfers (+1.9% and +4.4%, respectively). In the north-central area the trend was positive for investment (+26.4%), but negative for transfers (-14.9%). Expenditure by province increased for the “Mezzogiorno” in terms of investment (+5.7%), but decreased for transfers (-10.6%). In the north-central area, the trend was positive for both items, but it was considerably more significant for transfers (+30.3%) than for investment (+6.6%).

4.2 The National Recovery and Resilience Plan: Financial Resources for Public Investment3

In 2020, the Italian gross domestic product (GDP) decreased by -8.9% in real terms compared to 2019. Final consumption decreased by -7.8% and gross fixed capital formation by -9.1%. At the same time, the deficit-to-GDP ratio was -9.5% compared to -1.6% in 2019 (DEF 2021).4 The general government debt-to-GDP ratio rose to 155.6%, growing by 20.8 points compared to 2019 (134.8%) (ISTAT 2021a).

The deterioration in tax revenues contributed to the worsening of the Public Administration’s net borrowing indicators. In 2020, tax revenues decreased by €25,183 bn compared to 2019 (-5.3%). The change was also determined by legislative measures5 implemented to defer tax and social security contributions for businesses, the fine arts, and other professional activities. In order to address the economic damage caused by the pandemic, in 2020 the Italian government adopted fiscal stimulus measures amounting to approximately €130 bn through a series of decrees.6 The “relaunch” decree, the largest economic measure in Italy’s recent history, is a set of measures worth a total of €55 bn in net borrowing, primarily aimed at alleviating the strain caused by the lockdown measures on the Italian healthcare system, and the affected productive sectors and workers who, as a consequence, lost their jobs. All these measures led to an increase in 2020 in the general government deficit of approximately €108.1 bn (-6.5%/GDP). The deficit is expected to increase by €31.4 bn in 2021 (-1.8%/GDP), €35.3 bn in 2022 (-1.9%/GDP), €41.4 bn in 2023 (-2.2%/GDP), and €41.3 bn in 2024 (-2.1%/GDP).7 As for GDP growth, the government forecast (DEF 2021) is of a substantially flat trend for the first half of 2021, followed by a robust rebound in Q3, and a continued notably positive shift in the latter part of the year. At the time of writing, both the Bank of Italy (2021) and the European Commission (2021) had estimated an annual growth rate of approximately 5% for GDP in 2021.8 A return to pre-crisis levels of economic activity is expected to occur in the last quarter of 2022, according to the DEF (2021). As for the rate of unemployment, in 2018 it was 10.6%, in 2019 it was 10%, and in 2020 it was 9.2%.9

The EU has put in place substantial stimulus measures to counteract the economic crises caused by the pandemic. Italy presented its National Recovery and Resilience Plan (PNRR) to Brussels at the end of April 2021. It is an ambitious plan, 266 pages long. Italy is among the main beneficiaries of the NGEU, i.e., of more than €200 bn. It is also the second country, after Spain, which will benefit from the highest share of grants, a circumstance that could prove favourable for implementing short-term investments and stimulating economic recovery.

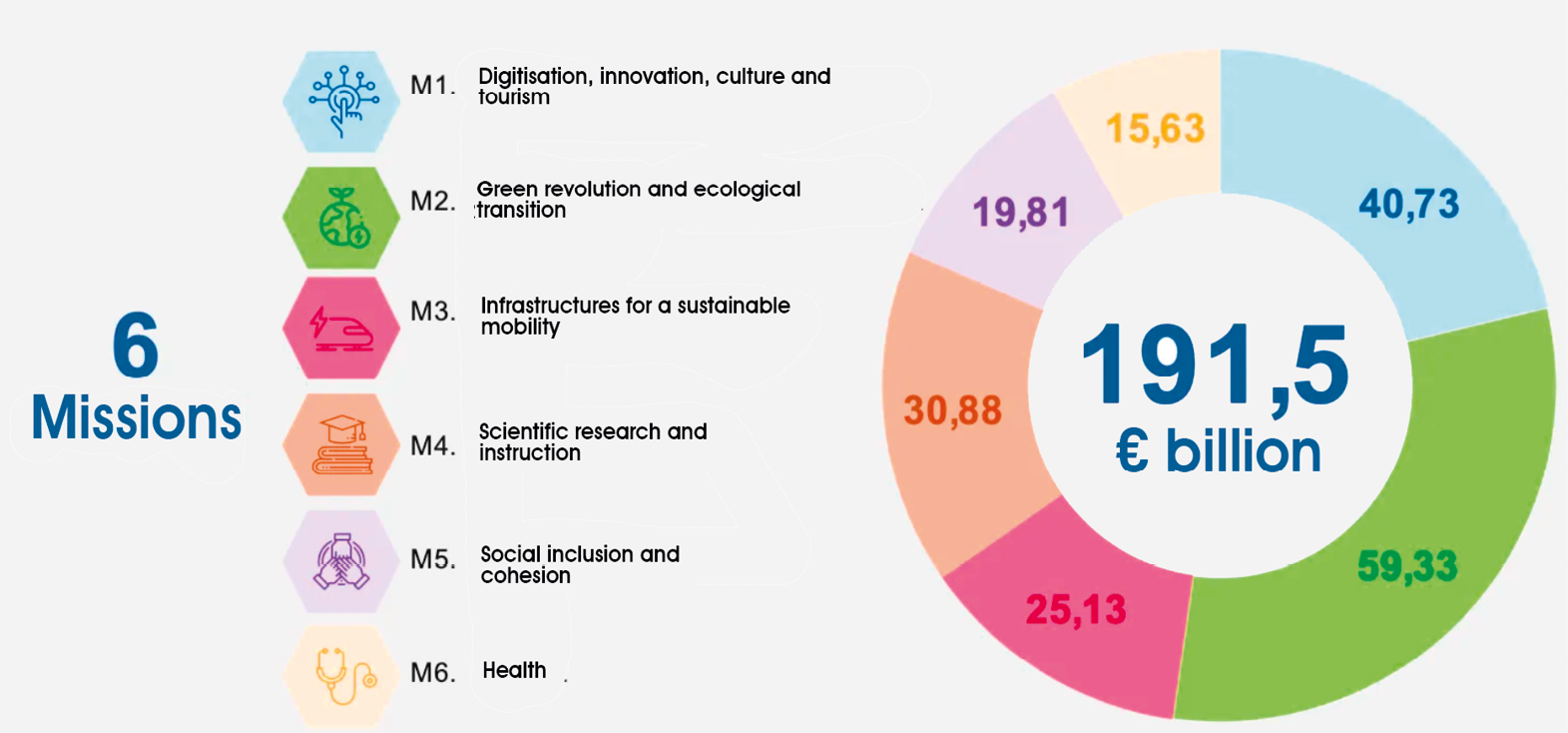

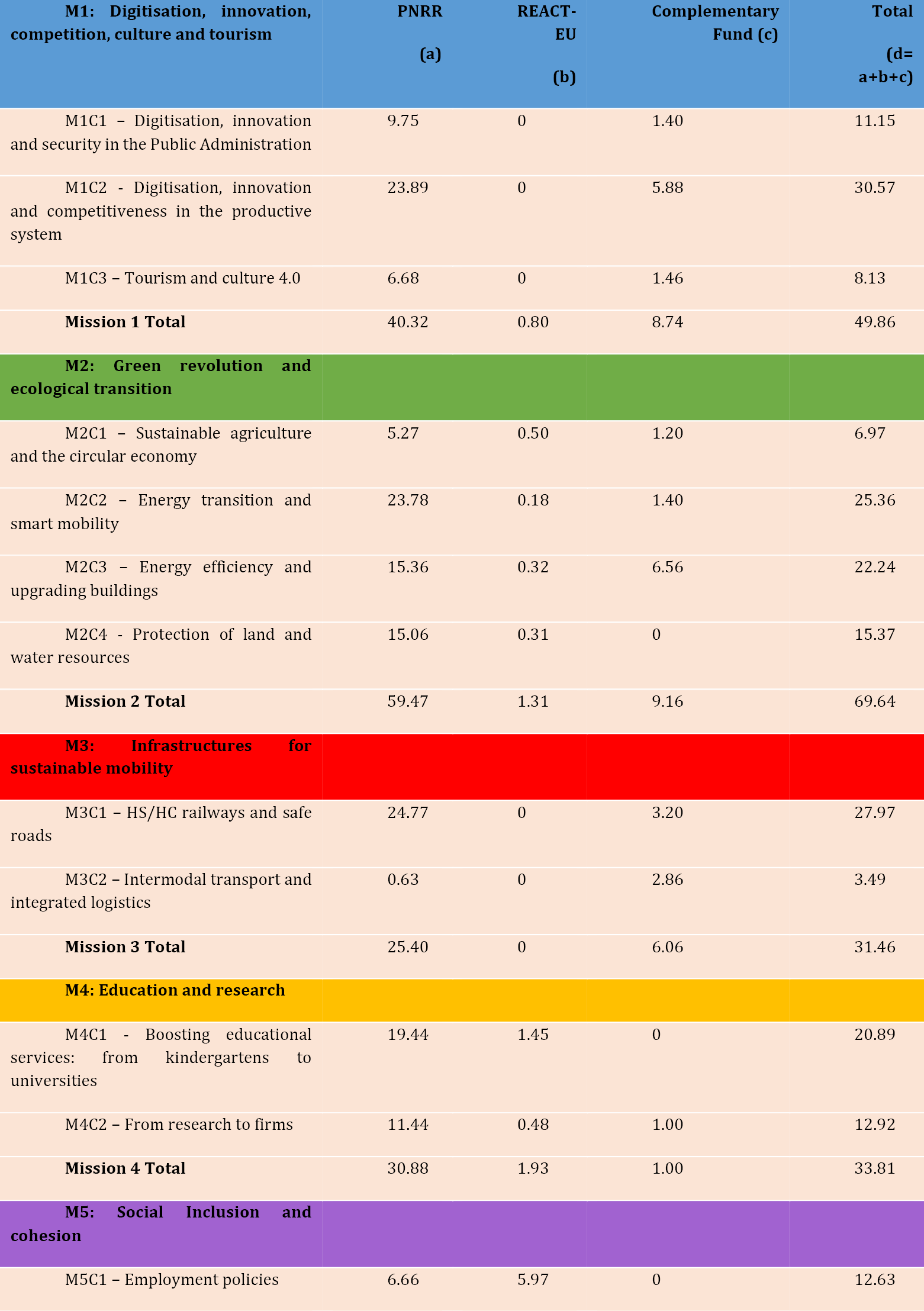

The Italian PNRR has six main missions, which follow the six-pillar structure defined by Regulation 2021/241 of the European Parliament and the European Council.10 The six missions are: 1. Digitisation, innovation, competitiveness, culture and tourism; 2. Green revolution and ecological transition; 3. Infrastructure for sustainable mobility; 4. Education and research; 5. Social inclusion and cohesion; 6. Health. These missions are in turn further broken down into sixteen components covering a variety of fields of action.11 The six missions and sixteen components translate into 133 different types of investment and 49 economic-institutional sectoral reforms worth a total of €235.12 bn, of which €191 bn is financed by the Recovery and Resilience Facility (RRF), €13 bn by REACT-EU for 2021–23, and a further €30.6 bn by the Complementary Fund12 through the budget changes approved by the Italian Council of Ministers on 22 April 2021. These capital expenditure commitments have been allocated for the period 2021–26 by D.L. no. 59 of 6 May 2021. On 22 June 2021, the Italian PNRR was officially approved by the European Commission, which described it as the most substantial, innovative, and courageous European transition and recovery plan.

Figure 8 below shows the subdivision of the RRF’s funding (€191 bn) for the six missions, and Table 1 shows the complete and detailed breakdown of PNRR expenditure by source of financing.

Fig. 8 RRF’s Allocation of Resources by Mission.

Source of data: Italian PNRR plan.

Table 1 PNRR Expenditure by Source of Financing (in billion euros)

Source of data: Authors’ own elaboration on PNRR data.

The PNRR stipulates that at least 37% of its resources must be allocated to green transition and 20% to digital transition across missions. The component of the PNRR which, in absolute terms, has received the largest share of resources is “Digitisation, innovation, and competitiveness in the production system”, with an allocation of €30.57 bn (M1C2).

As already stated, the plan foresees 133 different types of investment and 49 economic-institutional sectoral reforms (public administration, the justice system, streamlining rules and procedures, public procurement, the tax system, and strengthening social protection schemes).

Italy must now address both the consequences of the pandemic and its long-standing system frailties. In fact, the potential for real growth over the next years will not only depend on the considerable resources available, but also on the significant reforms foreseen by the PNRR. The government expects the transversal reforms to provide the required structural innovations for improving fairness, efficiency, and competitiveness, and consequently to boost the general state of the economy.

In short, the resources and reforms are necessary for unclogging three bottlenecks that have plagued Italy for decades. The PNRR has thoroughly identified them and stated that the cross-sector reforms aim to bridge the generational, territorial, and gender divides. These objectives are somewhat intertwined given that the employment issue for women and the youth in Southern Italy is decidedly worse. In fact, Daniele Franco, Minister of Economy and Finance, when presenting the Plan on 28 April 2021, clearly stated that: “only if we close the gender, generational and regional gaps can we obtain robust and sustainable growth in the medium term”.

Unemployment among young people in Italy is quite high.13 Furthermore, the employment gender gap in Italy, which was already pronounced before the pandemic, has now worsened further. Prior to the pandemic, one out of two women in Italy did not work. The employment rate was much worse in the south (33.2%) than in the north-central area (60.4%). In 2019, the male employment rate was 68%, while the female rate was 50.1%. The pandemic has affected economic sectors where higher rates of females are employed (food and beverage, tourism, etc.). In 2020, the rate of unemployment dropped to 49% for women and 67.2% for men.14 The PNRR tackles the gender gap issue by dedicating resources to social infrastructure (building more child daycare facilities, increasing full-time school classes, etc.), and incentives for women-owned businesses and more women entering STEM fields.15

The final, or fourth part, of the PNRR provides an assessment of the macroeconomic impact of the measures included in the Plan. As can be seen from Table 2, when considering the best possible scenario, in 2026 (thanks to the effect of the investment multiplier), Italy’s GDP should increase by 3.6 pp with respect to the baseline scenario.

Table 2 GDP Impact of the PNRR: Different Investment Efficiency Hypotheses (% Deviation with Respect to the Baseline Scenario)

|

2021 |

2022 |

2023 |

2024 |

2025 |

2026 |

|

|

GDP―Best scenario |

0,5 |

1,2 |

1,9 |

2,4 |

3,1 |

3,6 |

|

GDP―Medium scenario |

0,5 |

1,1 |

1,6 |

2,0 |

2,4 |

2,7 |

|

GDP―Baseline scenario |

0,5 |

0,9 |

1,4 |

1,5 |

1,7 |

1,8 |

Source of data: PNRR Table 4.3, p. 249.

4.3 Conclusion

The year 2020 marked a turning point in terms of infrastructure investment in Italy. Foremost, notwithstanding the pandemic, investment has not decreased thanks to measures adopted during the previous two years. Furthermore, the conviction (in Italy and Europe) that investment is needed for promoting growth and as a tool for maintaining the essential resilience needed to face other fundamental challenges (the environment, for example) has been strengthened as a consequence of the pandemic. Therefore, the growing investment trend set in motion in the first months of 2020, before the COVID-19 outbreak, was also the result of measures taken since 2018. From a qualitative and quantitative stance, 2020 marked a break from the previous “austerity-led” decade. The national programming agenda went from a policy approach focused on current spending and the compression of capital expenditure to a strategy based on growth-oriented infrastructure investment, geared toward the newly established objectives of energy and digital transition. The pandemic, with its recessionary effects on the economic system, stimulated this trend, and led to the current PNRR where investment is explicitly oriented towards a green and digital transition.

The PNRR also contains a seminal strategy for “restoring” the Italian economy and a specific focus on economic convergence and territorial cohesion for the south and the rest of the country. As already stated, inverting the tendency toward increasing the north-south divide is one of the primary objectives of the PNRR: the gap has existed since 1861, when Italy became a nation state, but it has gotten worse in recent years, especially since the economic and financial crisis of 2008–09.16 The average per capita investment in infrastructure in the “Mezzogiorno” over the past decade was around €780, which is 17% less than the €940 per capita average in the north-central area.17 The absence of impactful growth-oriented policies has thrust this part of the country down the path of economic stagnation and constant deindustrialisation. It is no coincidence that Southern Italy is one of the most economically depressed areas in the European Union (Senato della Repubblica 2018). Even before the outbreak of the pandemic in 2019, the Conte II government, aware of the problem, formulated an ad hoc plan aimed at countering and addressing the critical issues afflicting the south.18 The sustained effort to redirect Italy’s economic trajectory, characterised by low growth and increasing inequalities, is particularly evident in the PNRR’s allocation of funds for the south. In fact, around 40% of the PNRR’s resources (approximately €82 bn) will go to the eight regions that make up the “Mezzogiorno”. According to the PNRR, this funding is pivotal to the south’s economic development—in fact, its share of GDP is forecasted to increase to 23.4% in 2026. This is a significant objective given that, currently, the south accounts for 34% of the overall population, but it contributes to only 22% of Italy’s GDP. Moreover, in addition to the funds allocated by the PNRR, another €58 bn will be provided by the Development and Cohesion Fund (DCF), €54 bn by the 2021–27 Structural Funds, €8.4 bn by React-EU, and another €9.4 bn by the planned investment in the Salerno-Reggio Calabria railway line. Despite the flow of funds, there are also many risks that the convergence objectives will not be achieved. To begin with, the Plan lacks a precise breakdown of investment by territory for each mission and component.19 In addition, there are no clear criteria for allocating the resources, which creates the tangible risk that funds could be diverted, including for the south, to projects and networks that already exist and need to be completed, rather than to areas in which investment (especially social investment) needs to be created from scratch in order to generate the inclusion and development necessary for lasting and generative growth. It is also important to note a further risk that many of the resources will be allocated through incentive mechanisms for firms; however, the existing firms who are in a position to benefit from them prevail in the richest regions of the country. Another risk is the fact that many of the resources will be allocated through public procurement. It is not unreasonable to hypothesise that in the weaker areas, like the “Mezzogiorno”, the local administrations will not be sufficiently equipped for these projects and could remain outside the allocation of the resources mechanism. The PNRR’s impact on the “Mezzogiorno” will depend on its implementation. On this, the Minister for the South, Mara Carfagna, has stated on numerous occasions that every effort will be made to guarantee that Southern Italy receives at least 40% of the PNRR’s resources.20

In a nutshell, the actual implementation of the PNRR will depend on the governance mechanism and on the decision-making process that a multilevel government, as is the case for Italy, must undertake in defining public policies through consultation and coordination between the State, regions, and municipalities. Part 3 of the PNRR is dedicated to implementation and monitoring, and refers to a series of dispositions that must be adopted on governance. As we write this chapter, some of the measures have just been approved or are in the process of being defined.

The “simplification” decree (D.L. of 31 May 2021 no. 77, adopted into law in July 2021) first of all contains a series of measures that should simplify the planning phase, allocation of resources, implementation of projects, and definition of the Plan’s governance. More specifically, a steering committee acting as a “control room” has been established, chaired by the President of the Italian Council of Ministers, in which the relevant ministers and undersecretaries participate depending on the issues being discussed. It is essentially a variable-geometry mechanism. Others can be invited to join the meetings, such as the President of the Conference of Regions and/or of the Municipalities. Even more important is the provision whereby the President of the Council is substituted in the case of delays or non-compliance by other organs or institutions of the public administration. The decree also includes simplification measures that affect some of the sectors covered by the National Reform Programme (including ecological transition, public works, and digitalisation), in order to facilitate their complete implementation.

To conclude, for Italy, the main challenge will be to utilise PNRR funds effectively and break free from a past characterised by poor performance in managing public infrastructural investment. Italy, as one of the main beneficiaries of the NGEU, has an important role in ensuring its success. If the resources provided effectively boost investment and promote convergence and growth in Italy, the NGEU will have been a success and it will have provided a significant contribution to European integration.

References

Agenzia per la Coesione Territoriale (2019) Nucleo di Verifica e Controllo, Area 3 Monitoraggio dell’attuazione della politica di coesione e Sistema Conti Pubblici Territoriali, Relazione Annuale CPT 2019, Politiche nazionali e politiche di sviluppo a livello territoriale, CPT Temi, Roma, https://www.agenziacoesione.gov.it/wp-content/uploads/2019/11/Temi_11_Rap portoCPT_2019.pdf.

Agenzia per la Coesione Territoriale (2020) Nucleo di Verifica e Controllo, Area 3 Monitoraggio dell’attuazione della politica di coesione e Sistema Conti Pubblici Territoriali, Relazione Annuale CPT 2020, Politiche nazionali e politiche di sviluppo a livello territoriale, CPT Temi, Roma, https://www.agenziacoesione.gov.it/wp-content/uploads/2020/12/Relazione_annuale_CPT_2020_Politiche_naz_svil.pdf.

Banca d’Italia (2021), Proiezioni Macroeconomiche Per L’economia Italiana, June 11, https://www.bancaditalia.it/pubblicazioni/proiezioni-macroeconomiche/2021/Proiezioni-Macroeconomiche-Italia-giugno-2021.pdf.

Bucci, M., E. Gennari, G. Ivaldi, G. Messina and R. Moller (2021) I divari infrastrutturali in Italia: una misurazione caso per caso, Questioni di Economia e Finanza (Occasional Papers) n. 635, Banca d’Italia, https://www.bancaditalia.it/pubblicazioni/qef/2021-0635/QEF_635_21.pdf.

Camera dei Deputati e Senato della Repubblica (2021) Il Piano Nazionale di Ripresa e Resilienza―Schede di lettura NN. 06, N. 219, Servizio studi, 27 maggio 2021, http://documenti.camera.it/leg18/dossier/pdf/DFP28.pdf.

Cerniglia, F. and F. Rossi (2020), “Public Investment Trends across Levels of Government in Italy”. In F. Cerniglia and F. Saraceno (eds) A European Public Investment Outlook. Cambridge: Open Book Publishers, pp. 63–81, https://doi.org/10.11647/obp.0222.04.

European Commission (2021) Summer 2021 Economic Forecast: Reopening Fuels Recovery, European Economy, Institutional Paper 156, https://ec.europa.eu/info/sites/default/files/economy-finance/ip156_en.pdf

Franco, D. (2021) Dichiarazione del ministro Franco sul PNRR con i colleghi di Francia, Germania e Spagna, Ministero dell’Economia e delle finanze, Roma, 28 aprile, www.mef.gov.it.

ISTAT (2020) Livelli di istruzione e ritorni occupazionali. Anno 2019, Istituto Nazionale di Statistica, Roma, https://www.istat.it/it/files//2020/07/Livelli-di-istruzione-e-ritorni-occupazionali.pdf.

ISTAT (2021a) Conto trimestrale delle Amministrazioni Pubbliche, reddito e risparmio delle famiglie e profitti delle società, Istituto Nazionale di Statistica, Roma, https://www.istat.it/it/files//2021/04/comunicato-QSA-2020Q4.pdf.

ISTAT (2021b) Rapporto Annuale 2021. La situazione del paese, Istituto Nazionale di Statistica, Roma, https://www.istat.it/storage/rapporto-annuale/2021/Rapporto_Annuale_2021.pdf.

ISTAT (2021c) Indicatori territoriali per le politiche di sviluppo, Statistiche sez. indice, indicatori e dati Lavoro, Istituto Nazionale di Statistica, Roma, https://www.istat.it/storage/politiche-sviluppo/Lavoro.xls.

MEF (2020) Nota di Aggiornamento al Documento di Economia e Finanza, http://www.dt.mef.gov.it/modules/documenti_it/analisi_progammazione/documenti_programmatici/nadef_2020/NADEF_2020_Pub.pdf.

MEF (2021) Documento di Economia e Finanza, Sezione 1―Programma di Stabilità, http://www.dt.mef.gov.it/modules/documenti_it/analisi_progammazione/documenti_programmatici/def_2021/DEF_2021_PdS_15_04.pdf.

MEF (2021) Le diseguaglianze di genere in Italia e il potenziale contributo del PNRR per ridurle, July 9, https://www.mef.gov.it/focus/Le-diseguaglianze-di-genere-in-Italia-e-il-potenziale-contri buto-del-PNRR-per-ridurle/.

OCPI (2021) La ripresa degli investimenti pubblici, Osservatorio sui Conti Pubblici Italiani, June, https://osservatoriocpi.unicatt.it/ocpi-pubblicazioni-la-ripresa-degli-investimenti-pubblici.

Presidenza del Consiglio dei Ministri (2021) Piano Nazionale di Ripresa e Resilienza, aprile 2021, https://www.governo.it/sites/governo.it/files/PNRR.pdf.

Senato della Repubblica (2018) The Impact of Cohesion Policies in Europe and Italy, Research Paper no. 11, Impact Assessment Office, https://www.senato.it/service/PDF/PDFServer/BGT/01083823.pdf.

SVIMEZ/ENBIC (2021) Il lavoro nella pandemia: impatti e prospettive per persone, settori e territori, Report 2021, http://lnx.svimez.info/svimez/wp-content/uploads/2021/06/REPORT-SVIM EZ-ENBIC.pdf.

Viesti, G. (2021a) Il PNRR determinerà una ripresa dello sviluppo?, Rivista il Mulino, giugno 2021, https://www.rivistailmulino.it/a/il-PNRR-determiner-una-ripresa-dello-sviluppo.

Viesti G. (2021b) Gli investimenti del PNRR e del Fondo Complementare nel Mezzogiorno, https://www.forumdisuguaglianzediversita.org/gli-investimenti-del-pnrr-e-del-fondo-complementare-nel-mezzogiorno/.

1 If the public investment-to-GDP ratio is calculated assuming that the nominal GDP growth in 2020 is equal to that of 2019 (i.e., excluding the effects of the crisis), Italy’s ratio would still have grown from 2.3% to 2.4%. This is a remarkable performance, even if it is not possible to assess to what extent the increase in expenditure is due to a rise in the price of investments, rather than to an actual increase in the volume of investments.

2 Further details on this data source can be found in Cerniglia and Rossi (2020).

3 Most of the data in this section are taken from “Il Piano Nazionale Di Ripresa E Resilienza―schede di lettura n.06 and n.219”, and were compiled by the Servizio Studi di Camera e Senato, 27 May 2021 http://documenti.camera.it/leg18/dossier/pdf/DFP28.pdf.

4 The DEF (“documento di economia e finanza”) is the government’s medium term budgetary framework and is presented to parliament every April. It is a substantial document that describes the government’s financial objectives and the pertaining reforms in compliance with the constraints of the Stability and Growth Pact. The Nadef (nota di aggiornamento al DEF) is an update of the DEF in relation to the new data and information on trends within the macroeconomic and public finance framework; this update is presented to parliament every September.

5 Legislative Decree DL8 April 2020, n.23.

6 Cura Italia (D.L. n.18 /2020), Liquidity (D.L. n.23/2020), Relaunch (D.L. n.34/2020), August (D.L. n.104/2020), Ristori (D.L. n.137/2020), Ristori-bis (D.L. n.149/2020), Ristori-ter (D.L. n.154/2020), Ristori-quater (D.L. n.157/2020).

7 Among the largest expenditures are those provisions benefiting businesses (€56.1 bn in 2020), institutions providing ordinary and exceptional wage subsidies, COVID-19 subsidies, ordinary and emergency solidarity funds, and the NASPI and DIS-COLL unemployment subsidies. A one-off benefit totalling €9.2 bn in 2020 has also been established for self-employed workers, employees in the tourism sector, agricultural workers meeting specific requirements, VAT-registered professionals, workers enrolled in the entertainment pension fund, and domestic workers.

8 The real GDP growth rates were +0.9% in 2018, +0.3% in 2019, and -8.9% in 2020 (Source: Ameco).

9 As this work goes to print, employment in Italy has not yet returned to pre-pandemic (February 2020) levels. There are still at least 260,000 more people unemployed, the rates of employment and unemployment remain lower than before, and the rate of inactivity has increased by +0.7. A territorial analysis has highlighted a similar employment trend in the two macro areas for the fourth quarters of 2019 and 2020: an overall decrease by -2% in the “Mezzogiorno” and -1.9 in the north-central area. Women and young workers have been impacted the worst: female employment has decreased more in the “Mezzogiorno” (-3.0%) than the north-central area (-2.4%). The same is true for young workers under 35: -6.9% in the “Mezzogiorno” vs -4.4% in the north-central area. See https://www.istat.it/it/files//2021/09/CS_Occupati-e-disoccupati_LUGLIO_2021.pdf and Svimez/Enbic 2021.

11 The sixteen components are listed in Table 1. For example, the first mission has three components indicated as M1C1, M1C2, and M1C3.

12 The Complementary Fund, established by D.L. No. 59 on 6 May 2021, is an instrument provided by the PNRR with a total endowment of €30.6 bn for the period from 2021 to 2026. The Italian government has expressed its willingness to set up this fund to finance specific actions that complement and supplement the PNRR. These spending commitments comply with the provisions in EU Regulation 2021/241: https://www.gazzettaufficiale.it/atto/serie_generale/caricaDettaglioAtto/originario?atto.dataPubblicazioneGazzetta=2021-05-07&atto.codiceRedazionale=21G00070&elenco30giorni=true.

13 Italy has the third worst level of youth unemployment in Europe, with high peaks especially in the south. In 2019, the two regions worst off were Sicily and Campania—both had a youth unemployment rate of 53.6%.

14 While the initial impact of the pandemic was decidedly harsher on women, it now seems that, as in other advanced economies, it is more balanced. There have been some signs of positive and more balanced changes in female labour force participation in Q1 of 2021.

15 From the outset of the pandemic, the gender gap issue was immediately addressed by Elena Bonetti, Minister for Families and Equal Opportunities; see: “Women for a New Renaissance” (2020) and “The National Strategy for Gender Equality” (2021): http://www.pariopportunita.gov.it/news/pari-opportunita-bonetti-presentata-la-strategia-nazionale-per-la-parita-di-genere-2021-2026/.

16 For further details on the north-south divide, see the data provided by Svimez (http://lnx.svimez.info/svimez/), a research centre established in 1946 for the purpose of studying the economy of the “Mezzogiorno”. It publishes annual reports and other studies on the north-south divide.

17 See a recent study by the Bank of Italy (Bucci et al. 2021) based on CPT 2020 data. This study is also a seminal analysis of the infrastructure endowment by region: from infrastructure for transport (road and rail) to infrastructure for telecommunications, from the quality and types of services provided for water and energy to essential public services like healthcare and waste management. Reducing the north-south infrastructure gap was one of the declared objectives of delegation law n.42 in 2009 on fiscal federalism. It is an objective that exists only on paper, since nothing has been done in all these years to bridge the infrastructure gaps, albeit this is partially due to budget cuts and a lack of explicit measures and data on the infrastructural gaps. The PNRR could finally be the means through which to enact a specific strategy.

18 The plan, drawn up by Giuseppe Provenzano, Minister for the south, is called PianoSud2030 (Plan for the South 2030); it envisages a strategic investment programme of €21 bn over a three-year period, from 2021 to 2023, through national budgetary funds and the recovery of the last round of financing from the Development and Cohesion Fund and the European Structural Funds. The Plan also counts on new funds from the EU Programming for 2021–27 of approximately €123 bn for Southern Italy through the same instruments. The mission of PianoSud2030 has been partially absorbed by the National Recovery and Resilience Plan. https://www.governo.it/sites/new.governo.it/files/PianoSUD2030.pdf.

19 A precise and binding allocation of resources at the territorial level for the “Mezzogiorno” exists only in 33 of the 133 different types of investment and in 5 from the Complementary Fund. According to certain estimates, it amounts to approximately €23 bn, a bit more than one fourth of the overall resources (€82 bn) allocated for the “Mezzogiorno”. See Crf Viesti (2021a; 2021b).

20 In July 2021, an article was hinged to the “simplification” decree (D.L of 31 May 2021, no. 77) guaranteeing Southern Italy 40% of the total funds to be allocated through the PNRR.