5. Public Investment in Poland

© Adam Czerniak and Sebastian Płóciennik, CC BY 4.0 https://doi.org/10.11647/OBP.0280.05

Introduction

Nearly three decades of constant and relatively high economic growth has made it possible for Poland to initiate a catch-up with the most developed European economies. In 2000, GDP per capita amounted to less than €6500, representing only 29% of the average. Two decades later, in 2019, it reached €12,700, 48% of the average (Eurostat 2021a).

To continue this positive trend, Poland must fulfil several requirements―from a stable demographic situation, higher-level innovation, and efficient infrastructure to a better supply of public goods, like healthcare. One can hardly imagine a success in these areas without the government being ready to participate as a generous investor.

The purpose of this study is to analyse prospects for increasing the scale of public investment in Poland after the pandemic. It will indicate the most promising areas of the state’s activity and the priorities of the current government in investment. Further, it will offer an overview of the conditions required for rising public investment, including growth prospects and macroeconomic environments, as well as fiscal capacities, labour market features, and effectiveness of governance. A special place will be devoted to a new opportunity for a significant increase in public investment, which is Next Generation EU (NGEU)―the European Union’s programme aimed at combatting the long-term effects of the pandemic and the economic crisis.

The first part of the text is devoted to a short look at Poland’s experience in the field of public investment, both in terms of past policies and in more recent quantitative developments. The second part of the text focuses on the conditions required for a boost in public investment. The third part covers the analysis of the National Recovery Plan (Krajowy Plan Odbudowy, KPO)―the Polish vision of how the funds offered under the NGEU should be utilised in the national economy.

5.1 Historical Background

The topic of public investment in Poland is not free from political associations and ideological debates. Historical experiences play a significant role here.

On the one hand, there is a strong collective memory of the role of the government’s economic activity in recreating Polish statehood after the First World War. The challenge of sewing together the regions previously divided by borders required investment in transport infrastructure, of which the highlight was the seaport in Gdynia. Further achievements included the Central Industrial District (COP) in the south-east of the country, which aimed to create the economic backbone of the Second Republic (Grata 2019). The outbreak of the Second World War wiped out this promising effort.

The period after 1945―with the command economy and the communist state―is also a background for today’s discussions on public investment, albeit mostly in a negative sense. One of the crucial experiences of this time was the attempt to accelerate the growth of state investment financed by foreign loans in the 1970s. This did not lead to the expected increase in productivity, but rather a huge foreign debt, which also contributed to the collapse of the economy (Komornicka 2020). A both overwhelming and ineffective state, the domination of a “dirty” heavy industry and low-quality public infrastructure of the communist era largely explains the support that Poles gave in the late 1980s to the shock transformation aimed at a rapid shift to a free market.

5.2 Turning Points

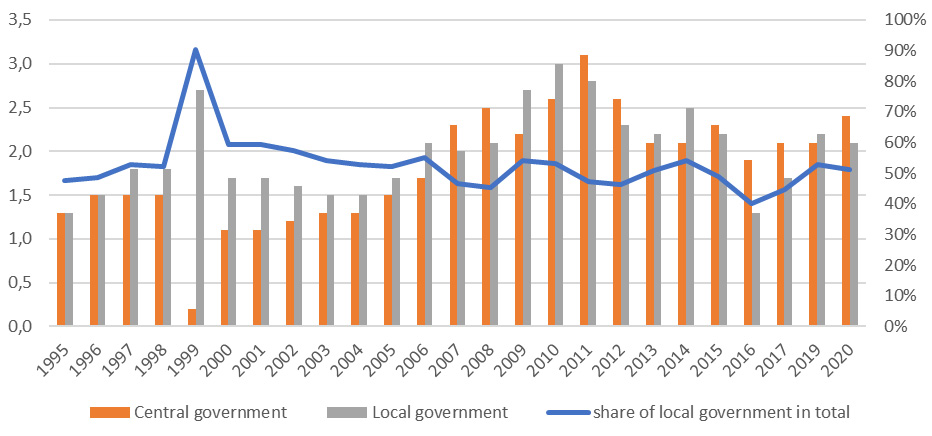

In the 1990s, the Polish economy entered a period of disinflation and budget constraints―conditions which are hardly favourable to public investment. The priorities of the post-communist transformation were the restructuring of the general governance sector and the acceleration of privatisation processes in areas previously treated as the sole domain of the state. The situation began to change in the second half of the 1990s, when economic growth significantly accelerated. Moreover, a far-reaching administrative reform was carried out and increased the role of local, self-government authorities in the economy. Across the last decades, the enlarged voivodeships and relatively autonomous districts and communes have undertaken around half of public investment (Figure 1). The reform was undoubtedly a turning point for public investment in post-communist Poland.

Fig. 1 Gross Fixed Capital Formation: Central Government and Local Government Expenditures as % of GDP, 1995–2020.

Source of data: Eurostat.

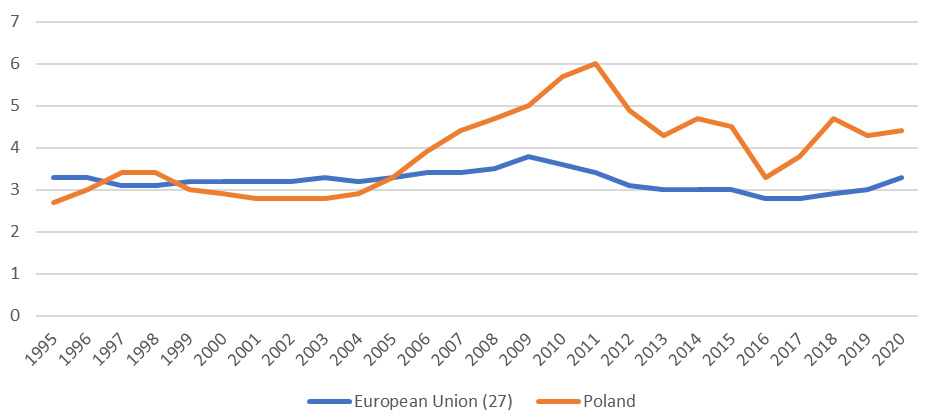

The next breakthrough came with the accession to the European Union in 2004. Poland gained access to huge community funds. This allowed for a systematic increase in the level of public investment, which was especially visible in the first Multiannual Financial Framework (6% in 2011―see Figure 2). The funds, combined with the means of central and local government, were allocated, e.g. to the development of previously neglected transport infrastructure. The inflow of capital through this channel has massively contributed to GDP growth and improved the competitiveness of Polish business. However, some experts have criticised the allocation key as being oriented too much towards the demand side in less developed regions, instead of boosting the growth potential of Poland (Gorzelak 2014).

Fig. 2 Gross Fixed Capital Formation: General Government Expenditure in Poland and the European Union (27 Member States) as % of GDP, 1995–2020.

Source of data: Eurostat.

The third important moment for the public investment sphere in Poland was the financial and economic crisis, which began in 2008 and weakened the neoliberal bias dominating after 1989. Political elites began to the see the state’s activity—more regulations, and involvement in the fight against the crisis—as a necessary precondition for a stable economic order. Thus, the government of the Civic Platform decided at that time in favour of a large fiscal stimulus. As part of this, large public projects emerged, like express inter-regional roads and the liquid-gas terminal in Świnoujście on the Baltic Sea. Afterwards, the crisis discussion about the rise of public investment continued. In the background stood the question of how to escape from the “dependent market economy” (Nölke and Vliegenthart 2009) to a more innovation-friendly system.

This line of thinking became mainstream when the United Right (Zjednoczona Prawica) came to power in 2015. One of the main goals of the new government was to accelerate the modernisation of the economy through large centrally-led projects. The Strategy for Responsible Development (Strategia na Rzecz Odpowiedzialnego Rozwoju, SOR; KPRM 2017), designed by the then-Minister of Finance Mateusz Morawiecki, has become the flagship declarative document. The government’s plans included spectacular ideas that had not been seen since the 1970s: for the construction of a state-owned electric car factory (Izera), the dredging of the Vistula Spit—which is to allow the development of the port of Elbląg—and the construction of the Central Airport (CPK), a transport hub located near Warsaw.

The last important turning point for the sphere of public investment in Poland was the outbreak of the pandemic and the economic crisis in 2020. It strengthened the belief that in the face of an external shock and a massive fiscal expansion is necessary. The government did not hesitate to boost deficit spending to 7% of GDP in 2020 (according to Eurostat)―mainly in the form of protective programmes for enterprises and employees. However, the government also declared new public investment plans. Their determinants, size, and content will be presented below.

5.3 Determinants for Public Investment Increases

5.3.1 Investment Needs

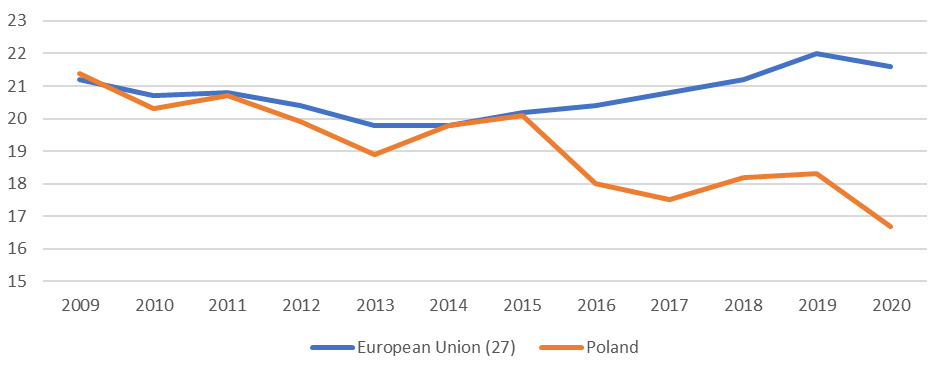

Poland is still one of the poorest countries in the European Union. Despite rapid economic growth and substantial real convergence over the last quarter of a century, in 2020, GDP per capita in Poland was equal to €13,640―the fourth lowest level among the twenty-seven EU member states, and only 46% of the EU27 average. Many factors contributed to this outcome, of which path dependence (i.e., a very low starting point at the beginning of the transformation period) is most likely the dominant one. Putting aside the discussion on the past, it is best to focus on future possibilities and investment needs, since achieving high capital intensity and the capacity to innovate is the only way to sustain the process of real convergence in times of an ageing society. This, however, seems to be a problem for Poland, as the total investment rate has been decreasing steadily in recent years (MFiPR 2020), reaching an all-time low of 16.7% of GDP in 2020 (see Figure 3). Such a process happened despite the government goal to increase the total investment rate (private and public combined) above 20% of GDP, as explicitly expressed in the Strategy for Responsible Growth in 2017.

Fig. 3 Gross Fixed Capital Formation in Poland and the European Union as % of GDP, 2009–2020.

Source of data: Eurostat.

The decrease in propensity to invest was mostly seen among private entrepreneurs, who hoarded a record amount of savings and restrained from engaging in long-term and large-scale investment activity. Moreover, their willingness to invest in R&D endeavours aimed at increasing their future efficiency was also relatively low-standing, at 0.83% of GDP in 2019 as compared to 1.46% on average in the EU27. However, no consensus has emerged on the reasons for this outcome. Some economists point out the relatively high margins and low labour costs of Polish companies, which decrease the incentives to invest in more efficient and capital-intensive technologies. Others focus on rising business uncertainty after the Global Financial Crisis, amplified by the increasing labour shortages in Poland―which are connected to low labour activity, low retirement age, and an ageing society—discouraging entrepreneurs from large-scale investment in increasing output capacity. Another group of experts focuses more on aspects of the political economy after the change of government in 2015. They argue that a more redistributive model of social policy—along with higher uncertainty relating to fiscal burdens and the deterioration of the rule of law―deemed high investment activity as too risky for entrepreneurs, who must be prepared for an unexpected increase in the tax wedge, nationalisation attempts, and higher demand volatility. Some analyses also indicate that a lower investment rate is a natural side effect of the economic transformation, away from capital-intensive heavy industry towards a service-oriented economy dominated by small and medium enterprises. In our opinion, the truth lies somewhere in the middle, as each factor exhibits its impact on different groups of entrepreneurs, leading to a substantial decline in private investment activity that calls for urgent government action. Without action, there is a serious threat that the convergence process in Poland will come to a halt, as economic growth led solely by consumption will eventually generate excessive inflation and push Poland in the direction of economic turmoil.

The most urgent public investment needs are clearly pointed out in recently-published government documents―Strategy for Responsible Growth in 2017, Poland’s Energy Policy adopted in 2021, the forthcoming healthcare strategy for 2021–27, and almost all of the National Recovery Plan and the Polish Deal (Polski Ład), drafted and presented by the governing party PIS (Law and Justice) in mid-May of 2021. After studying these documents, a clear-cut picture emerges. The most important issues that need to be addressed are the transformation of the energy sector, digitilisation of the economy, society and public administration, housing affordability, improvement of the quality and availability of the healthcare system, and modernisation of transport infrastructure, both through building new motorways and investing in railways. Solving these issues requires a coherent plan with multi-source financing, as the joint costs of all these ventures can be estimated at a mind-blowing amount of over one trillion PLN―to be spent over this decade. If these plans succeed and the government can satisfy its financing needs at a low interest, then the fulfilment of this changeover strategy will bring long-term benefits to the economy and society. However, there are plenty of pitfalls that need to be avoided in the process, especially connected to large-scale government projects, such as the plan to build a central airport hub in the crop fields of Central Poland.

5.3.2 Macroeconomic and Institutional Environment

The pandemic disrupted a long period of fast economic growth in Poland. The recessions triggered by lockdowns caused GDP to decline by 2.7% in 2020―relatively little compared to most EU countries. The mild course of the crisis is owed to the structure of the economy, of which key sectors are industrial branches and business-oriented services. The most vulnerable branches, like tourism, play a lesser role than in the southern EU member states.

The outlook for the post-pandemic rebound is very positive. According to the Spring Forecast of the European Commission, GDP growth is expected to accelerate to 4% in 2021 and 5.4% in 2022. High levels of savings, consumer confidence, and the expected rise of investment in the private sector create a solid base for recovery. An additional factor driving growth will be external demand, boosted by the also rebounding euro area economy (European Commission 2021a, p. 110).

Under these circumstances, inflation―already high before the pandemic―may pose a difficult challenge. In 2020, the HICP index increased by 3.7%. The European Commission predicted in the Spring Forecast that the indicator will reach 3.5% in 2021 and start falling slowly to 2.9% in 2022―more than twice what it is in the euro area (European Commission 2021a). There is a lively debate in Poland on how much this development is caused by temporary and external factors, and when the central bank should react by exiting from its ultra-expansionary monetary policy. Concerns about overheating the economy are on the rise and it may provoke questions if additional boosts in spending within the area of public investment make the problem worse.

The next determinant is the fiscal situation. The pandemic forced the Polish government to increase public spending. As a result, in 2020, the general government deficit amounted to 7% of GDP. In 2021, the situation should improve due to an increase in tax revenues and lower expenditure on “shields” for enterprises. In 2022, the indicator should already have dropped below 3%. Despite a clear deterioration of the fiscal situation, Poland still meets the public debt criterion. In 2020, the debt level increased to 57.5%, but by 2022 it should drop to 55%. There is not so much spending space left to reach the warning thresholds written in the law, which foresees austere measures against further rise of debt. In the context of higher public investment, there is a lively debate about a possible revision of the legal framework for the fiscal policy in Poland towards more permissive rules.

The labour market situation also constitutes a potential limit for the boost of public investment. Poland has spectacularly low unemployment levels— with a level of 3.2% in 2020, it belongs to best performing countries in the EU. Even considering the near completion of aid programmes launched during the pandemic, unemployment levels should not, according to the European Commission, exceed 3.5% in the next two years. However, a potential emerging problem may be a deficit in workforce and the fast rise of wages, which could further boost the already high inflation levels. Political constraints on immigration, as well as a quickly deteriorating demographic situation (with an expected two-million drop in population by 2040; Eurostat 2021b), combined with the low retirement age, will not make the situation easier. Under these circumstances, public investment plans may face the problem of quickly rising labour costs or even a lack of sufficient workforce to achieve its goals.

Finally, the factor which should be taken into account when increasing public investment is the effectiveness of the administration in preparing projects, organising tenders, and controlling the spending of funds. A good point of reference for the assessment of this criteria is the ability to absorb EU funds. Luckily, Poland does not look substandard in comparison with other member states. According to the Multiannual Financial Framework 2007–16, it performed slightly better than the EU average, and the rate of absorption was higher than in neighbouring countries (the Czech Republic, Hungary, Slovakia, and Germany; Darvas 2020).

5.4 The National Recovery Plan

5.4.1 General Information

The National Recovery Plan (Krajowy Plan Odbudowy―KPO) is the Polish agenda for disbursing EU funds from the Recovery and Resilience Facility (RFF). Poland’s allocation from the RFF is €34.6 bn, out of which €23.9 bn comes in the form of subsidies and €10.8 bn in the form of loans granted within the RFF to Poland. This translates into ca. 156 bn PLN of funds (6.7% of GDP per year from 2020) that should be disbursed until 2026. According to the KPO, the majority will be used to increase public investment (87.1 bn PLN) and the rest to stimulate private gross fixed capital formation (68.9 bn PLN). As shown in Figure 4, the government wants to start injecting the EU funds into the Polish economy as early as 2021, and expects the expenses to peak between 2023–25. In our opinion, this process will be delayed, as at the time of writing (August 2021), the KPO has not yet been accepted by the European Commission, minimising the probability that money will reach the real economy before early 2022.

Table 1 National Recovery Plan Funds by Purpose and Expected Year of Disbursement, 2020–26, in bn PLN.

|

2020 |

2021 |

2022 |

2023 |

2024 |

2025 |

2026 |

2020–2026 |

|

|

Public investment |

0.0 |

1.9 |

12.9 |

20.7 |

19.3 |

20.9 |

11.4 |

87.1 |

|

Private investment |

0.7 |

2.3 |

9.8 |

14.6 |

14.7 |

13.4 |

13.4 |

68.9 |

|

TOTAL |

0.7 |

4.2 |

22.7 |

35.3 |

34 |

34.3 |

24.8 |

156 |

Source of data: Ministry of Finance, 2021.

The start date of the disbursement of EU funds is additionally uncertain due to several inconsistencies between the KPO and the European Commission’s policy agenda, including the European Semester. There are also some doubts whether the disbursement of the funds properly addresses the requirement to spend at least 37% of the funds on Green New Deal projects and at least 20% on acceleration of the digitilisation process.

These incoherencies can be traced back to the eclectic mode of preparation. The Polish government began to write the KPO in July 2020 (Klub Jagielloński 2021). In theory, the process was coordinated by the Ministry of Funds and Regional Policy, which is responsible for spending EU funds in Poland, but in practice it became a process of multilateral struggles between various ministries to get the biggest chunk of the funds, with the Minister of Economic Development being in the leader’s seat. Eventually, the Prime Minister’s Chancellery took over the coordination of the process and decided case-by-case which projects to include in the KPO.

This process transformed the KPO into a collection of bottom-drawer legislatives, i.e., various ideas from ministries, state agencies, state-owned companies, and local governments that had been put aside due to lack of funding. Many of them were of poor quality or based on unrealistic assumptions. It was only at the final stage that they were combined into larger sets of initiatives, but still requiring better coherence and a stronger link to the RFF agenda.

Eventually, in the autumn of 2020, the Prime Minister’s Chancellery arranged the KPO agenda into a plan matrix and, after a period of internal consultations, it will open the discussion to social partners and the general public at the end of February 2021. After some minor amendments, the National Recovery Plan was approved by parliament in May 2021. The final version of the KPO consists of five main parts (or components): (A) resilience and economic competitiveness (B) green energy and lower energy consumption (C) digital transformation (D) efficiency, availability, and quality of the healthcare system, and (E) green and smart mobility.

5.4.2 Five Components of the National Recovery Plan

Resilience and economic competitiveness (€4.7 bn)

This is the most general part of the plan. It consists of policies from various institutional areas (e.g., the labour market, housing, and social protection) that should help the economy to recover from the pandemic. The first element of this component (A1) consists of measures that are aimed at reducing the impact of COVID-19 and the effects of the crisis on enterprises to the amount of more than €2 bn. Companies are the major direct beneficiaries of this element, but some public investment is also planned, including money for preparing land for greenfield investment and financing for the acceleration of spatial planning. In the second element (A2), activities for the development of the national innovation system are grouped. Although most of the €500 m earmarked for this purpose is to go to companies, there are also public projects here, such as the construction of a museum of architecture and design in Krakow. The third element (A3) is aimed at improving education and the lifelong learning system to match the skills of employees with what is needed within the economy. This part also covers a plan to spend €500 m on the creation of 120 industry vocational skills and career guidance centres, so as to promote education and training in general. The last element (A4) contains an increase in the structural adjustment, efficiency, and crisis resilience of the labour market. An important goal is to increase the professional activity of women, part of which involves investment in nurseries and daycare centres, especially outside large urban areas (€400 m). Significant amounts are also earmarked for improving the operation of employment offices and e-administration. In the loan part, €150 m will be earmarked for increasing the use of satellite data—for instance, for monitoring weather risks. The government also plans reforms to strengthen the stability and transparency of public finances, reduce the regulatory burden, and increase the role of public consultation in law-making.

Green energy and reduction of energy consumption (€14.5 bn)

This KPO component coincides with the EU’s long-term financial perspective and the Just Transition Fund, which is aimed at helping communities affected by coal mining closures. The overall goal in this area is to transform key sectors of the economy to a low-carbon model, while maintaining competitiveness and energy security. The plan consists of three elements. The first (B1), worth €3.2 bn, is the improvement of energy efficiency. Much attention has been paid to supporting the transition to a less energy-intensive mix of heat generation in residential buildings. As far as the sphere of public investment is concerned, the most important thing is the thermal modernisation of schools envisaged in the plan. The second part (B2) focuses on increasing the use of renewable energy sources. A considerable amount of funds has been allocated to the development of transmission networks, development of hydrogen technologies, and intelligent infrastructure increasing energy consumption efficiency. By the end of 2024, an installation terminal for the construction of offshore wind farms is to be built and launched, and by 2026, offshore farms with a capacity of 2.6 GW and electrolysers to produce green hydrogen with a capacity of 400 MW will be completed. The last element (B3) includes activities aimed at adapting the Polish economy to climate change and limiting environmental devastation. It is planned, amongst other things, that degraded and post-industrial areas will be revitalised, including the cleaning of the bottom of the Baltic Sea. Additional funds will be allocated to facilitate the creation of “green” cities, e.g., those with limited traffic. Loans will be used to finance―in addition to offshore wind energy farms―green urban transformation, including “green multifamily housing”. The government is planning to establish a Green Urban Transformation Fund co-managed by local governments. The loan component also includes support for sustainable water management in rural areas.

Digital transformation (€4.9 bn)

Poland will allocate 20.9% of the funds to digital transformation―only 0.9 pp more than the minimum set by the European Commission. That is, in our opinion, an important deficiency of the plan, as there are significant deficits in the field of digital competence in society and in the computerisation of state institutions in Poland. The first element of this component (C1) is aimed at improving access to high-speed internet (>30 Mb/s), with a goal of increasing the proportion of households that have such access from around 65% to more than 80% in 2026. In this element, state support for private investment activity is planned, especially in regions with lower population density. For example, the loan component will help to finance the construction of 5G networks by telecommunication companies. In turn, element C2 focuses on the development of digital services, also within public administration and between businesses, society, and the state. For example, the introduction of dozens of new e-services (e.g., e-invoicing and the digitalisation of construction permits) by public institutions is a planned development, as well as the creation of new communication platforms. Significant funds are to be spent on expanding the digital infrastructure of schools and improving teachers’ competence, which should result in an increase in the overall level of digital skills in society. The last part of this component (C3) is devoted to investment in increasing digital security.

Efficiency, accessibility, and quality of the healthcare system (€4.5 bn)

This component is compliant with the Polish Deal—the government’s newly published economic and social policy programmet―that also prioritises the improvement of healthcare services. The basis for reforms and investment in both documents is the Polish healthcare strategy for 2021–27. The EU funds will be used to expand the public healthcare infrastructure, especially in oncology, psychiatry, and geriatric care, and to digitise healthcare and provide financial support for the education of medical students. The government also wants to finance the development of medical research and the pharmaceutical industry―for example, by creating a research centre for epidemic safety in Poland. The loan component will be used to facilitate the development of the pharmaceutical sector, primarily the production of active substances―manufacturers will be able to apply for €300 m in loans. Initially, the government wanted to finance the purchase of COVID-19 vaccines (€1.4 bn) using RRF funds, but they were forced by the European Commission to drop this idea.

Green and smart mobility (€7.3 bn)

In this component, the government plans, amongst other things, to promote a low-carbon economy in private companies and zero-emission public transport—in part, due to the approaching Fit for 55―and aims to cover the costs of the sector with ETS. There is, for example, over €1 bn’s worth of funds available for the purchase of EV buses and an additional €200 m for the purchase of new trams. Over half of the funds will be used to develop the Polish network of railway transport, including the modernisation of railway lines, purchases of new passenger rolling stock, and the construction of intermodal terminals. The government has also pledged to rewrite the e-mobility roadmap and increase the competitiveness of railways by reducing fees for access to infrastructure (charged by the railway network company PKP PLK). Almost all the expenses in this part of the plan will be procured by local governments.

5.4.3 Macroeconomic Impact of the National Recovery Plan

The disbursement of the funds according to the National Recovery Plan will have both direct and indirect effects on the economy. In the short term, it will stimulate aggregate demand and, through multiplier effects, increase employment, GDP, and tax income, speeding up the economic recovery. On the other hand, the programme might also lead to an increase in inflation, as companies are having supply-side problems with satisfying the fast-increasing demand, which provides incentives to increase prices in the wake of full capacity utilisation. In the long term, the disbursement of EU funds can stimulate the growth of the potential output by increasing the amount of working-age population in good health as well as boosting total factor productivity, thanks to higher energy efficiency, lower bureaucratic burden, and better labour skills.

According to baseline economic simulations of the Ministry of Finance, as presented to the European Commission in the regular update of the Convergence Programme (Ministry of Finance 2021), in the short term the implementation of the KPO will increase the real GDP level by 1.2% in 2024, compared to the baseline scenario without additional spending.

In the first three years of using the funds, the real economic growth rate will increase by an average of 0.56 pp compared to the baseline scenario. In 2027, the GDP level will be 1.3% higher than in the baseline scenario presented in the plan. The implementation of the KPO will also have a positive impact on the labour market. It is estimated that, after two years, 0.3% more jobs will be created, and after five years of using the funds in line with the KPO project, the number of jobs created will increase by 0.4% compared to the baseline scenario (see Table 2).

Table 2 Macroeconomic Impact of the National Recovery Plan

|

2024 |

2027 |

2042 |

|

|

difference to the no-policy change scenario |

|||

|

GDP |

+1.2% |

+1.3% |

+1.9% |

|

Employment |

+0.3% |

+0.4% |

+1.3% |

|

General government balance |

+0.3% |

+0.3% |

+0.9% |

Source of data: Authors’ own assumptions based on Ministry of Finance 2021 calculations.

The long-term effects (i.e., twenty years after the beginning of the programme) of using funds from the RFF are related mainly to reforms and investment in green transformation, digital transformation, and the healthcare system. Moreover, as the RFF will be distributed across the European Union, it will translate into the greater economic growth of Poland’s main trade partners (on average, +0.9 in the EU27, according to the European Commission; European Commission 2020), boosting the external demand for goods produced in Poland. The Ministry of Finance estimates that introducing the KPO will yield a 1.9% higher GDP over the long term than in the baseline scenario. Of these, 1.3 pp will be the result of high labour supply and better matching of workers’ skills (translating into lower natural unemployment rate), and the remaining 0.6 pp will result from the accumulation of productive capital.

In the long term, the main factors supporting Poland’s economic growth under the influence of KPO, apart from the increase in productivity, will be favourable changes in the population resulting from the improvement of the efficiency, availability, and quality of the healthcare system, and the increase in labour market activity. According to the Ministry of Finance’s forecast, the population in 2042 will increase by 303,000 inhabitants, and the economic activity rate will increase by 0.9 pp compared to the baseline scenario. As a result, along with the increasing qualifications of employees and the demand for labour, employment is expected to increase by 1.3% compared to the baseline scenario in the horizon of twenty years.

According to the European Commission, the disbursement of grants from the RRF will have a neutral impact on the public deficit path of EU member states (European Commission 2021b). In the case of debt, grant flows may have a temporary negative impact due to the mismatch in cash expenditure and receipts over time. In line with these assumptions, the Ministry of Finance expects that, despite some minor short-term negative effects, the KPO will increase the general government balance due to higher tax incomes and lower expenditure needs from domestic funds. In total, the public deficit will be reduced by 0.3 pp in the short term and 0.9 pp in the long term, providing additional fiscal space to stimulate the economy in times of a slowdown, making Poland more resilient to negative external shocks.

5.5 Conclusion

The long-term investment plans of the Polish government are ambitious. If they are accomplished, both society and the economy will benefit, as real convergence will be sustained, the adaptation to the new climate policy will be faster, and private investment outlays will flourish, being made more attractive by high infrastructure quality, low transaction costs, and a skilled labour force. However, there are many pitfalls that need to be avoided―there is the risk of overheating the economy in the case of demand growing too quickly, the risk of engaging in investment projects that are deemed to fail (as it is constantly the case with motorway construction contracts in Poland), and finally there is the risk of over-politicising the investment process, which in our opinion might be the biggest risk, taking into account the polarisation of the Polish political scene and the partisan cycle it induces (i.e. consecutive periods of radical policy U-turns).

Moreover, there are also some intrinsic risks stemming from the weaknesses of the current programmes, especially the National Recovery Plan. Its text exhibits a lack of significant measures to increase the economic activity of the elderly and the disabled, and it leaves us with doubts regarding the achievability of the goals in society’s “digital” activation. For example, providing wider access to education does not always translate into the improvement of skills, if proper incentives and nudges are not provided simultaneously. In turn, long-term effects of the KPO are strongly dependent on the way in which the available money will be spent. As the disbursement of EU budget funds shows, the selection of qualified projects―as well as tender design―can largely affect the quality and adequacy of public investment outlays. There is also a political risk the KPO is exposed to. In the event of an escalation of disputes with the European Commission over the rule of law, access to funds may be suspended―which would mean immeasurable economic damage.

References

Darvas, Z. (2020) “Will European Union Countries Be Able to Absorb and Spend Well the Bloc’s Recovery Funding?” BlogPost Bruegel (24.9.2020), https://www.bruegel.org/2020/09/will-european-union-countries-be-able-to-absorb-and-spend-well-the-blocs-recovery-funding/ .

European Commission (2020) European Economic Forecast, Autumn 2020, https://doi.org/10.2765/878338 .

European Commission (2021a) European Economic Forecast, Spring 2021, https://ec.europa.eu/economy_finance/forecasts/2021/spring/ecfin_forecast_spring_2021_pl_en.pdf .

European Commission (2021b) Debt Sustainability Monitor 2020, https://ec.europa.eu/info/publications/debt-sustainability-monitor-2020_en .

Eurostat (2021a) Real GDP per Capita, https://ec.europa.eu/eurostat/databrowser/view/sdg_08_10/default/table?lang=en .

Eurostat (2021b) Europop 2019: Population Projections at National Level 2019–2100, https://ec.europa.eu/eurostat/databrowser/view/proj_19np/default/table?lang=en .

Grata, P. (2019) “Central Industrial District as an Attempt to Implement the Principles of Sustainable Development in the Inter-War Period Poland”, European Journal of Sustainable Development 8(5), European Center of Sustainable Development: 137, https://doi.org/10.14207/ejsd.2019.v8n5p137 .

Komornicka, A. (2020) “From ‘Economic Miracle’ to the ‘Sick Man of the Socialist Camp’: Poland and the West in the 1970s”, European Socialist Regimes’ Fateful Engagement with the West: National Strategies in the Long 1970s, 78–106. Taylor and Francis, https://doi.org/10.4324/9780429340703-5 .

KPRM (2017) Strategia Na Rzecz Odpowiedzialnego Rozwoju Do 2020 (z Perspektywą Do 2030 r.), https://www.gov.pl/documents/33377/436740/SOR.pdf .

MFiPR (2020) Raport: Inwestycje w Polsce. Okres: I Kw. 2018―4 Kw. 2019, https://www.ewaluacja.gov.pl/media/93243/DSR_Raport_Inwestycje2018_IV2019_web2.pdf .

Ministry of Finance (2021) Convergence Programme 2021 Update, https://www.gov.pl/web/finance/convergence-programme .

Nölke, A. and A. Vliegenthart (2009) “Enlarging the Varieties of Capitalism: The Emergence of Dependent Market Economies in East Central Europe”, World Politics 61 (4): 670–702, https://doi.org/10.1017/S0043887109990098 .