6. Trends and Patterns in Public Investment in Spain: An Update

© José Villaverde and Adolfo Maza, CC BY 4.0 https://doi.org/10.11647/OBP.0280.06

Introduction

After a good deal of both theoretical and empirical analysis on the issue, it is pretty obvious that there is a general consensus about the positive effects of public investment on the economy (for a recent survey, see Bom and Ligthart 2014). GDP, employment, and private investment trends are closely related to that of public investment, although the value of the corresponding multipliers is still a matter of certain debate. As is well known, it depends on a number of factors such as, for instance, the level of development and the stage of the economic cycle (for an analysis on influential factors, see, e.g., Gechert 2015). This direct and positive link between public investment and, amongst other things, the three aforementioned macrovariables, becomes particularly important in times of economic crisis, such as during the Great Recession of 2008 and the current COVID-19 pandemic.

In this update of our previous paper (Villaverde and Maza 2020), we pay attention to the key characteristics related to the evolution of public investment in Spain between 2000 and 2020. Specifically, although we have to admit the data is very scant and the period still too short, in Section 6.1 we focus our attention on the new economic crisis unleashed by the pandemic and, more precisely, try to shed some light on its effects on public investment. In the next part of the paper, Section 6.2, we make a brief reference to what Next Generation EU funds may imply for public investment in the country. Finally, in Section 6.3, we present the main conclusions from our research.

6.1. Public Investment in Spain: 2000–20

When evaluating the relevance and evolution of anything (be this a plant, an animal, an idea or an economic variable), the judgement critically depends on what or who we are comparing with. As for economic variables in the case of Spain, it seems natural to start, very briefly, by comparing them with those of Spain’s main partners and competitors, namely the EU countries.

According to its GDP, Spain is (after Germany, France, and Italy) the fourth largest economy in the EU, fifth before Brexit took place. In terms of public investment specifically, it is also the fourth European economy, and although its evolution from 2000 onwards has followed a similar path to that of the average of the EU, there is no doubt that it has also experienced much larger fluctuations. This is indeed true for each one of the three main subperiods we can split the period of 2000–19 into and, to a certain extent, for the year 2020. During the expansion period 2000–08, Spain registered, in 2015 constant prices, one of the highest increases in public investment among the EU countries, a rate (about 6% per year) much higher than that of both the EU and Eurozone averages (2.7%). The Global Financial Crisis that hit the EU, and the whole world, in 2008 and successive years had a very negative impact on Spanish public investment. More precisely, with a fall of around 12% per year between 2008 (€46.2 bn) and 2014 (€22.6 bn), Spain was, by far, the country that suffered the deepest decline among the big four. Not only this, but it also experienced a much larger drop than the EU and Eurozone (the annual drop was 3.2 and 2.1%, respectively). In 2014, however, the economic situation in Spain began to improve at a greater speed than in the EU; this is most probably the reason why Spanish public investment between 2014 and 2019 not only returned to positive rates of growth (see further below), but also its growth rate was, on average, much higher than that of the EU. Although quite understandable, the pro-cyclical performance of Spanish public investment is counterproductive in terms of stability, as this variable is supposed to play, at least in cases of severe recessions, an anti-cyclical role to limit the pressures from the economic cycle. Fortunately, and as stressed later on, this seems to be the case in the year 2020, when the health, social, and economic crisis hit the country most acutely.

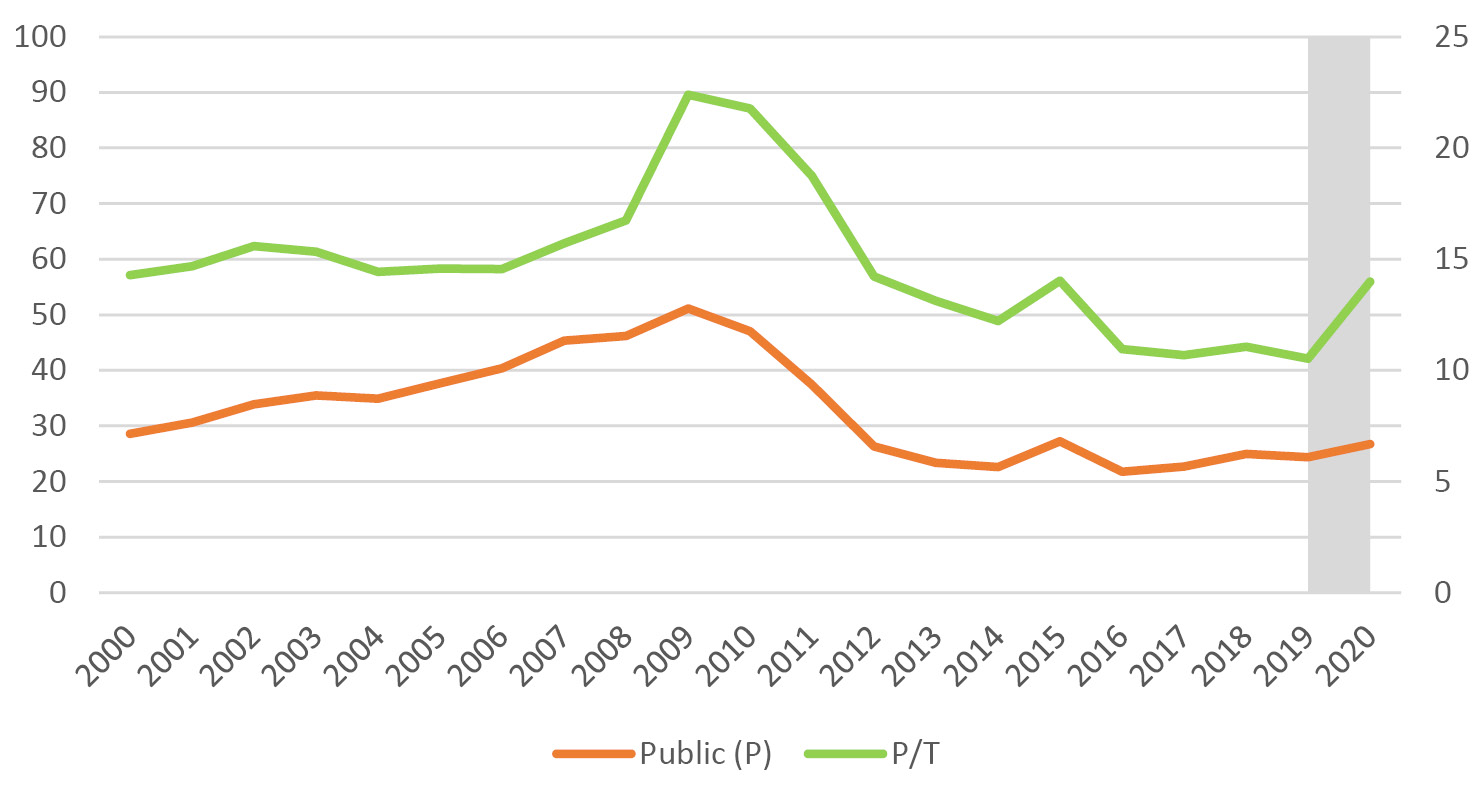

The aforementioned pro-cyclical role of public investment is depicted in Figure 1. As can be seen, public investment (measured in bn euros, 2015) exhibited a relatively steady upward path from 2000 to 2009, declined sharply from then to 2014, and has remained relatively stable afterwards. There are, however, two relevant exceptions to this pro-cyclical path. The first one refers to 2009: although this is a year of clear, huge recession in Spain, public investment grew even more rapidly than in previous years, most likely as a government’s attempt to reduce the depth of the crisis that erupted in 2008. The second exception refers precisely to 2020, the year of the COVID-19 outbreak, in which the Spanish government also tried to soften the effects of the pandemic on both GDP and employment. As depicted in the green line of Figure 1, the public-to-total (P/T) ratio grew very sharply, much more than in any other year of our sample period, both in 2009 and 2020.

Source of data: AMECO database. Figure created by the authors.

Note: Public investment is given in 2015 € bn. The ratio P/T is measured (in pp) on the right-hand axis.

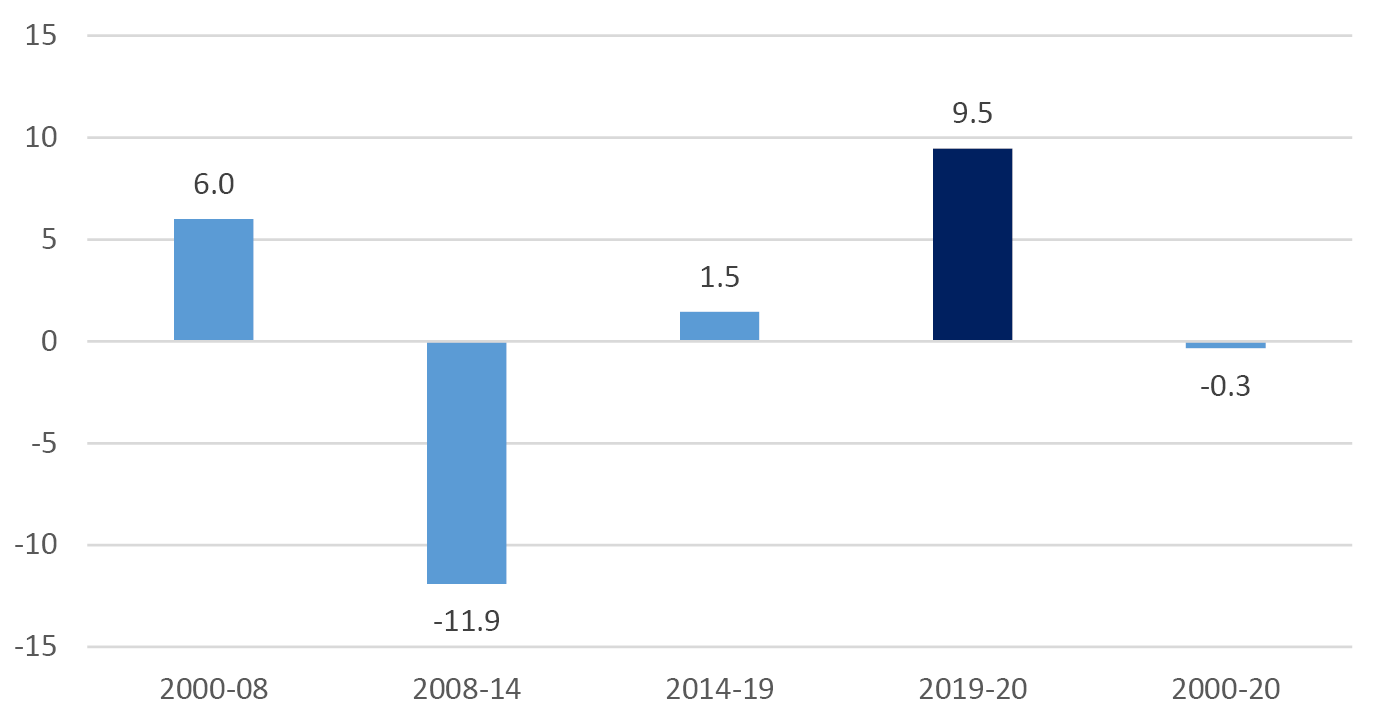

Be that as it may, the pro-cyclical role of public investment in Spain can be seen even more clearly in Figure 2, in which the period under consideration has been split into expansion and contraction subperiods. Concerning the expansion ones and in line with previous comments, it is observed that public investment grew at a very high rate (6% per year) between 2000 and 2008 and, once again, although at a much lower one (1.5% on an annual basis), between 2014 and 2019. As for the contraction subperiods, it is shown that, despite the significant growth in 2009 noted above, public investment experienced a severe decline during the 2008–14 subperiod, with an average yearly rate of -11.5%. The revival of public investment in 2020, with an increase of 9.5%, effectively illustrates, and confirms, the second exception to the pro-cyclical tendency mentioned in the previous paragraph.

To conclude with the public investment evolution, we think another additional trait needs to be highlighted: expressed in 2015 constant euros, public investment in Spain declined over the 2000–20 period at an average annual rate of -0.3% (Figure 2), a fact that explains why its level in 2020 is lower than that in 2000 (Figure 1).

Fig. 2 Public Investment: Growth Rate (%).

Source of data: AMECO database. Figure created by the authors.

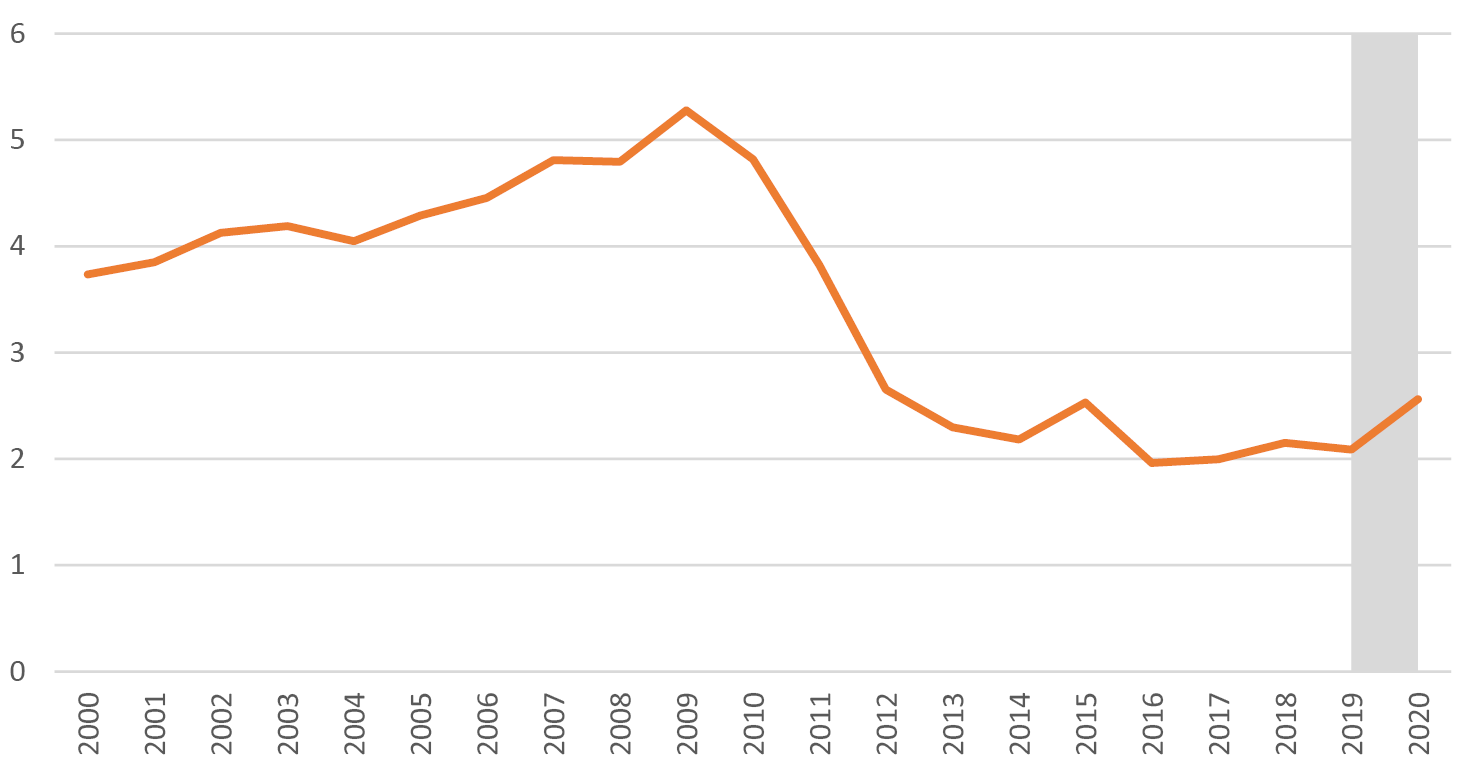

An indirect but complementary, as well as quite significant, way of analysing the evolution of public investment is by paying attention to the investment effort made by the government. Measured through the ratio “public investment/GDP (in pp)”, Figure 3, apart from confirming what was previously reported, shows that Spain made a great investment effort during the first boom subperiod 2000–08 (4.3% per year) and the first year of the Great Recession, 2009 (5.3%). Afterwards, and due to the guidelines issued from Brussels regarding the consolidation of public finances, the investment effort dropped very sharply until 2014, and then remained more or less stable at a level of just over 2%. Fortunately, in 2020, and because of the more relaxed and anti-cyclical policy stance emanating from Brussels, the investment effort grew once more, but to a meagre 2.6%; in any case, it is evident that it falls far short of what is needed, since its level in 2020 is around 50% lower than the average between 2000 and 2009.

Fig. 3 Public Investment Effort: Public Investment over GDP (%).

Source of data: AMECO database. Figure created by the authors.

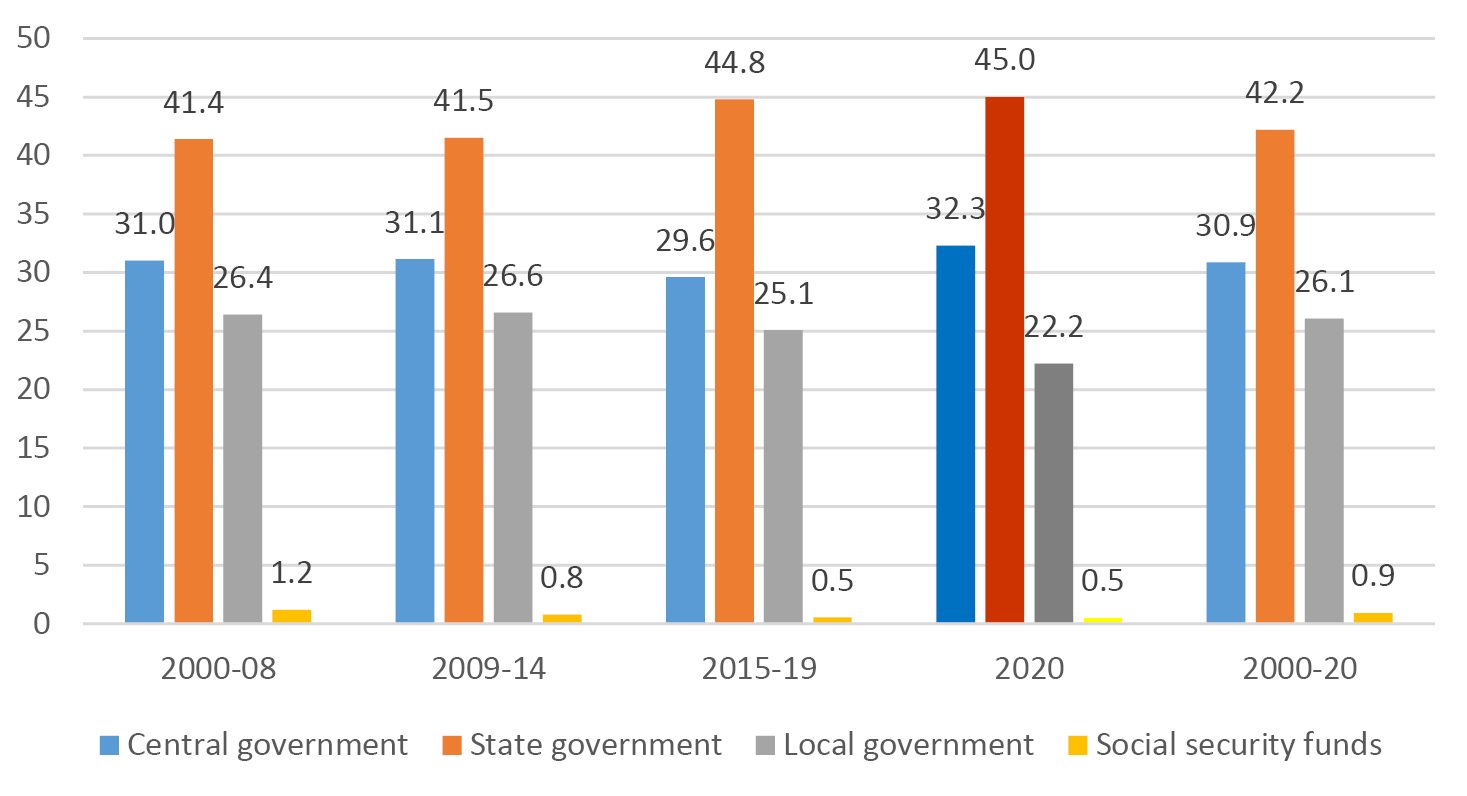

Up to now, we have referred to public investment without considering the level of government that acts as the effective investor. This might not be relevant for a country with a highly centralised way of governing, but it is important for a country, such as Spain, with a very decentralised one (for an analysis of fiscal policy across levels of government, see OECD 2010). In this respect, Figure 4―in which, for the sake of clarity, we once again split the whole period into expansion and contraction subperiods―shows the shares corresponding to the three tiers (central, state or regional, and local) of government, plus the social security share. Three features need to be highlighted: first, that the state governments are the main public investors in Spain; second, that their share in total public investment increased over time; and third, that this share has peaked up precisely in 2020, reaching a value of 45%. On average, more than 42% of public investment in Spain comes from state governments, around 31% from the central government, and 26% from local governments; as expected, the share corresponding to social security has been almost negligible (less than 1%).

Fig. 4 Distribution of Public Investment by Government Level (%).

Source of data: EUROSTAT database, along with an extension for the year 2020 based on IGAE data (IGAE stands for ‘Intervención General de la Administración del Estado’). Figure created by the authors.

Finally, it is important to note that just as relevant as the level and evolution of public investment is its composition, the areas in which public funds are being invested. According to Table 1―which only covers the period 2000–19, because there is no official, reliable data about 2020―it is obvious that, making use of the so-called Classification of the Functions of Government (COFOG), the share devoted to “economic affairs” (which includes subheadings such as general economic, business, and labour affairs; agriculture, forestry, fishing, and hunting; fuel and energy; mining, manufacturing, and construction; transportation; communications; other activities; and R&D related to economic affairs) is always the most relevant, with figures accounting for more than 40% of the total. As can be seen by looking at the three subperiods, and in what may be considered as a government attempt to play, to a certain extent, an anti-cyclical role, the amount of investment in “economic affairs” reached its maximum share during the huge economic contraction that took place between 2009 and 2014. As for the rest of assets, it is worth mentioning that the second position in the ranking always corresponds, and with increasing values, to the “general public services” (including subheadings such as executive and legislative bodies; financial, fiscal, and foreign affairs; foreign economic aid; general services; basic research; R&D related to general public services; public debt operations; and general intergovernmental transfers). The third position is occupied by either “health”, also with increasing values, or “housing and community amenities”, in this case with decreasing ones. Although, as mentioned before, there is no information about what happened in 2020 from this perspective, it is very likely that, due to the efforts made to overcome the severity of the COVID-19 crisis, the share devoted to investment in health had reached a new peak. Even being higher, this new peak will not probably be much higher than the previous one, considering that most of the spending in this area was current and not capital spending.

Table 1 Distribution of Public Investment by Type of Asset (%)

|

2000–08 |

2009–14 |

2015–19 |

2000–19 |

|

|

General public services |

11.00 |

12.58 |

16.59 |

12.54 |

|

Defence |

7.00 |

5.32 |

8.26 |

6.69 |

|

Public order and safety |

3.09 |

2.86 |

3.07 |

3.01 |

|

Economic affairs |

41.52 |

45.27 |

40.71 |

42.59 |

|

Environmental protection |

5.67 |

4.75 |

4.56 |

5.17 |

|

Housing and community amenities |

9.82 |

6.93 |

4.65 |

7.94 |

|

Health |

6.67 |

8.21 |

9.82 |

7.75 |

|

Recreation, culture, and religion |

6.92 |

6.26 |

4.97 |

6.35 |

|

Education |

6.50 |

6.09 |

6.34 |

6.34 |

|

Social protection |

1.79 |

1.73 |

1.01 |

1.63 |

Source of data: EUROSTAT database following COFOG. Figure created by the authors.

6.2. Next Generation EU: Some Insights from Spain

As is well known, due to the severe economic crisis caused by the COVID-19 pandemic, the EU institutions (the European Commission, the European Parliament, and the European Council) launched a recovery plan, branded Next Generation EU (NGEU). This plan, which breaks with the rules of no common debt issuance (de la Porte and Jensen 2021), aims to stimulate the economic recovery of the EU member countries by laying the foundations for a modern and more sustainable Europe, agreed on a European recovery fund of up to €750,000 m (in 2018 constant prices). Spain, the EU country hardest hit in economic terms, is expected to receive, over the period 2021–26, up to €140,000 m, about half of them in direct transfers and the other half in soft credits. However, at the time of writing, and due to the uncertainty and the difficulty of setting actions for a longer period, the current Spanish recovery plan—the so-called “RTRP”, which stands for Recovery, Transformation, and Resilience Plan (see Spanish Government Agenda 2030)—revolves around the reforms and investment to take place between 2021 and 2023 only.

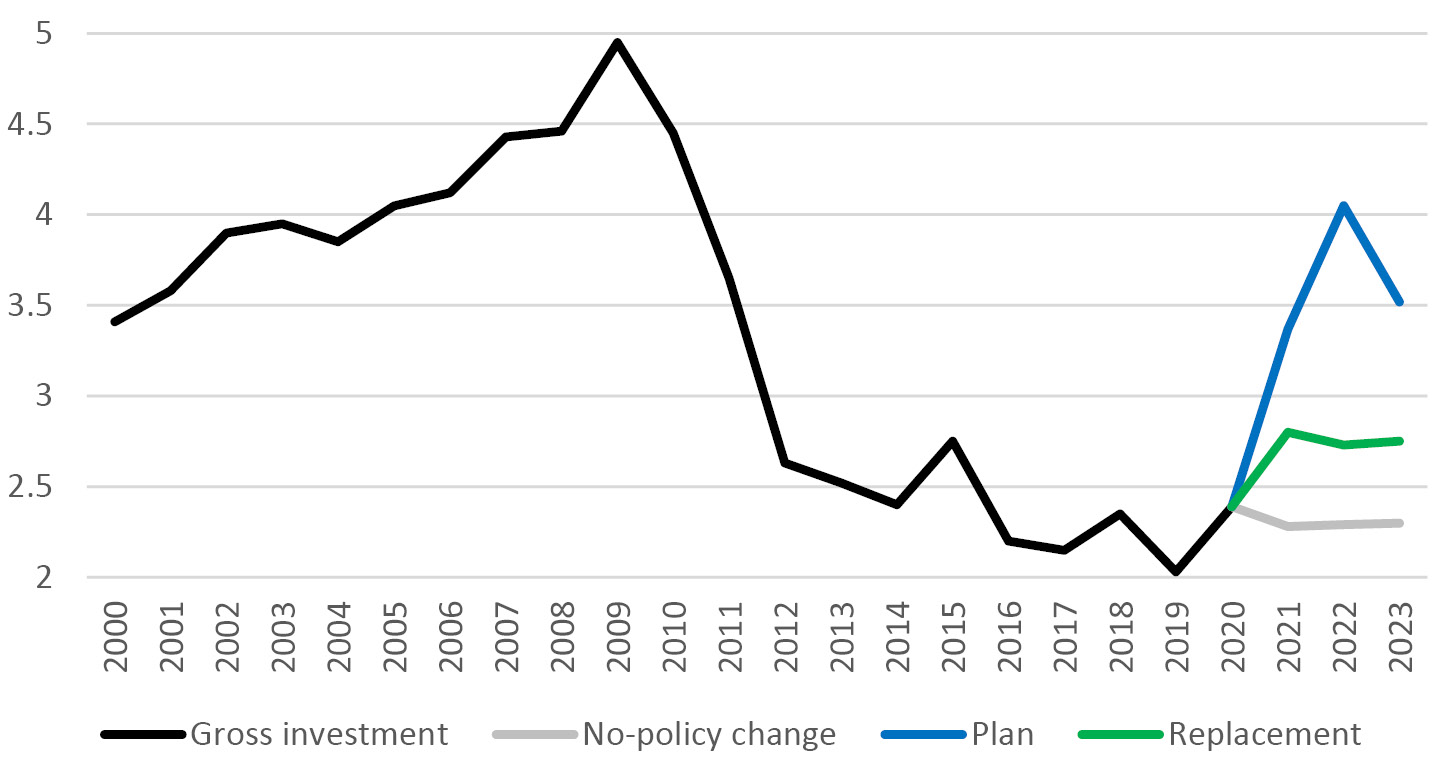

Regarding public investment, it is important to note that, as pointed out in the RTRP, without the support of direct transfers from the European funds, it would be practically nil because of a context of limited fiscal space and a great need for current spending on health and education. In a trend scenario, it would mean, in practice, assuming a continued deterioration of the capital stock, as can be seen in Figure 5, since the tendency line (referred to as “no-policy change”) is below the “replacement” line. There is no doubt this situation would have a negative effect on long-term growth and, consequently, on social and territorial cohesion (since many of these public investments are territorialised). However, the investment foreseen in the RTRP (represented by the “plan” line in Figure 5), with its additive nature, will make it possible to reach an investment effort of around even 4% of GDP some years and always appreciably higher than the “no-policy change” scenario; this will not only imply closing the gap with the EU average, but also allow net investment to be positive for the first time since 2011.

Fig. 5 Investment Recovery: Gross Public Investment (% GDP).

Source of data: Valencian Institute of Economic Research (IVIE) dataset and AMECO dataset. The figure is an adaptation created by authors of the original published in Spanish Government Agenda 2030 (2021).

As shown in Table 2, the nearly €70,000 m of investment from direct transfers will be mainly devoted to two large areas, in line with the EU climate and digitalisation agendas: green transition and digital transformation. Human capital formation and R&D are two other important areas in which a large amount of the European funds will be invested. The main aim of this investment is to boost productivity and, in so doing, to increase the potential growth rate of the economy. In short, its purpose is to make the Spanish economy more modern, more resilient, and more competitive.

More specifically, in the classification by investment levers (again, see Table 2), the lever related to the modernisation and digitalisation of industry stands out (23.1% of total investment), which includes the development of the Spain 2030 Industrial Policy, strategies to enhance small and medium-sized enterprises, the plan for the modernisation and competitiveness of the tourism sector, and the promotion of digital connectivity and 5G. Another very important target of the funds will be the development of a rural and urban agenda that will, among other things, modernise agriculture and promote territorial cohesion (20.7%). It includes, amongst other things, an action plan for sustainable mobility in urban and metropolitan environments, housing rehabilitation and urban regeneration, and the environmental and digital transformation of agriculture and fisheries. The third investment lever we want to highlight is that devoted to the development of resilient infrastructures and ecosystems (15%). Given the structural impact that infrastructures can have on the economy and on society, the aim is to develop nature-based solutions and strengthen their capacity to adapt to climates―and, thus, their resilience. To this end, investment will focus on the conservation and restoration of ecosystems and biodiversity, the preservation of the coastal zone and water resources, and, again, progress in terms of sustainable, safe, and connected mobility.

|

Lever Policies |

Amount (%) |

|

I. Urban and rural agenda, territorial cohesion, and modernisation of agriculture |

14.407 M€ (20.7%) |

|

II. Resilient infrastructures and ecosystems |

10.400 M€ (15.0%) |

|

III. A fair and inclusive energy transition |

6.385 M€ (9.2%) |

|

IV. An administration for the 21st century |

4.315 M€ (6.2%) |

|

V. Modernisation and digitalisation of industry and SMEs, entrepreneurship and business environment, recovery and transformation of tourism and other strategic sectors |

16.075 M€ (23.1%) |

|

VI. Promotion of science and innovation and strengthening of the capabilities of the National Health System |

4.949 M€ (7.1%) |

|

VII. Education and knowledge, lifelong learning, and capacity building |

7.317 M€ (10.5%) |

|

VIII. The new care economy and employment policies |

4.855 M€ (7.0%) |

|

IX. Promotion of the culture and sports industry |

825 M€ (1.2%) |

|

X. Modernisation of the tax system for inclusive and sustainable growth |

- |

|

Total |

69.528 M€ |

Source of data: The table is an adaptation created by authors of a figure published in Spanish Government, Agenda 2030 (2021).

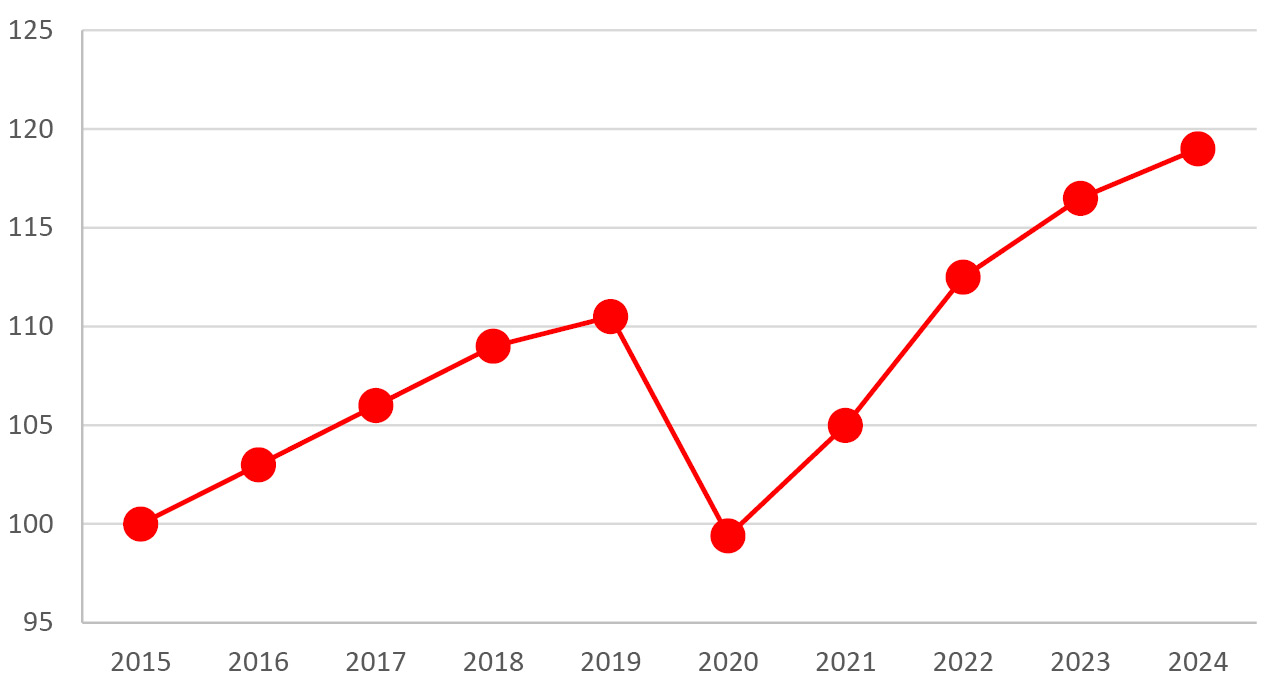

According to the RTRP, it is foreseen that this new stream of public investment will give, on average, an approximate boost to the GDP of 2 pp per year, something that, hopefully, will allow Spain to return to its pre-COVID-19 GDP growth trend by, approximately, the end of 2022 (GDP forecast can be seen in Figure 6). As for the labour market, it is expected that, in aggregate terms, the employment generated by the RTRP could exceed 800,000 jobs at the end of the plan´s execution period. Not only this, but they will be quality jobs which, in principle, should increase the productivity of the Spanish economy, one of its well-known weaknesses. Finally, and in a similar vein, although admittedly a little more difficult to assess, it is also foreseeable that the investment from the RTRP will affect Spanish foreign trade positively. More precisely, a 0.2 pp increase in the long-term growth rate of exports is expected.

Fig. 6 Macroeconomic Impact (GDP Forecast 2015 = 100).

Source of data: National Statistical Institute of Spain, Ministry of Economic Affairs and Digital Transformation. The figure was taken from Spanish Government Agenda 2030 (2021).

6.3. Conclusion

The aim of this chapter, apart from summarising the main findings of a previous one (Villaverde and Maza 2020), was twofold. First, to present new evidence on the evolution of public investment since 2000 and, above all (and despite the fact that in this case the evidence is necessarily partial due to the scarcity of data), to present evidence from during the COVID-19 pandemic. Second, to briefly discuss the key points of the content of the Spanish recovery plan, the RTRP. By doing so, the paper has reached some interesting conclusions.

First, and contrary to what is expected, public investment in Spain has mainly played a pro-cyclical role in the new century. There were just two exceptions to this general trend: the years 2009 and 2020, precisely when the two recent economic recessions were at their strongest.

Second, the investment effort made by the public authorities in Spain has been very volatile and, on average, lower than that of the EU. After the outbreak of the pandemic, nevertheless, it has increased markedly and is expected to continue in the same vein.

Third, state (regional) governments have not only carried out most of the public investment in the country, but also their share of total public investment has grown over time, even after the outbreak of the COVID-19 pandemic. In any case, the largest increase in public investment in 2020 corresponded to the central government.

Fourth, the economic affairs category of the Classification of the Functions of Government (mainly infrastructure) is the one that received the lion’s share of Spanish public investment―on average, more than 40% of the total. Although we are unable to give precise figures due to the paucity of data, it seems clear that we can point to the existence of a strong increase, yet to be quantified, in health investment during the current COVID-19 crisis.

Fifth, between 2021 and 2023, in the context of the NGEU plan and as a way to promote economic recovery, Spain will receive an amount close to €70,000 m in the form of direct transfers. According to the RTRP, this will bring net public investment back into positive figures for the first time since 2011.

Sixth, this additional public investment spending will hopefully give an important boost to the Spanish economy, namely to GDP (an additional increase of 2% per year) and employment (about 800,000 new jobs by 2024).

Although very promising, we consider that the positive expectations for the future of the Spanish economy linked to the European funds are a bit too optimistic and, therefore, have to be tempered. This opinion is based, on the one hand, on the foreseeable delays in the implementation of the NGEU plan and, therefore, in the effective delivery of funds to Spain and, on the other, on the fact that the investment projects that will benefit from these funds are not yet sufficiently detailed. In any case, there is no doubt that the arrival of the EU funds (the sooner the better) will give a big push to the economy, helping it, as mentioned before, to become more modern (productive), resilient, and competitive. This is an opportunity that Spain cannot afford to miss.

References

Bom, P.R. and J.E. Ligthart (2014) “What Have We Learned from Three Decades of Research on the Productivity of Public Capital?”, Journal of Economic Surveys 28: 889–916, https://doi.org/10.1111/joes.12037.

De la Porte, C. and M. Jensen (2021) “The Next Generation EU: An Analysis of the Dimensions on Conflict behind the Deal”, Social Policy and Administration 55(2): 388–402, https://doi.org/10.1111/spol.12709.

Gechert, S. (2015) “What Fiscal Policy is Most Effective? A Meta-Regression Analysis”, Oxford Economic Papers 67(3): 553–80, https://doi.org/10.1093/oep/gpv027.

OECD (2010) “Fiscal Policy across Levels of Government in Times of Crisis”, COM/CTPA/ECO/GOV/WP 12, OECD, Paris.

Spanish Government, Agenda 2030 (2021) Plan de Recuperación, Transformación y Resiliencia (Recovery, Transformation and Resilience Plan). Madrid, https://www.lamoncloa.gob.es/presidente/actividades/Documents/2021/130421-%20Plan%20de%20recuperacion%2C%20Transformacion%20y%20Resiliencia.pdf.

Villaverde, J. and A. Maza (2020) “Trends and Patterns in Public Investment in Spain”. In F. Cerniglia and F. Saraceno (eds), A European Public Investment Outlook, Cambridge: Open Book Publishers, pp. 83–95, https://doi.org/10.11647/obp.0222.05.