9. Education, Human Capital, and Social Cohesion

© Chapter Authors, CC BY 4.0 https://doi.org/10.11647/OBP.0280.09

Introduction

The pandemic has speeded up many of the great transformations that are taking place in society. Pervasive digitalisation, green transition, major changes in job markets due to the new industrial revolution, the ageing society, growing inequalities and poverty, geo-political changes—the list goes on. In this sense, the pandemic has become an unexpected “experimental laboratory” for what may become our new world. The evolution of this new world can still be directed in one way or another, and it represents both risks and opportunities. We must be careful to think through and design the most effective policies and investments that leave no-one behind and protect us from the risks inherent in such transitions.

Indeed, it is of paramount importance that we invest massively in our human and social capital—and especially in education and lifelong learning.

In the 1950s and 1960s, scholars like Jacob Mincer, Theodore Schultz, and Gary Becker documented and explained the close connection between human capital (i.e., the stock of skills, abilities, and knowledge an individual possesses) and economic returns. Their groundbreaking studies stimulated a growing research agenda, which is still contributing to our knowledge concerning the relationship between the educational system and the economy. For example, we know that education, combined with other variables, significantly affects an individual’s social mobility, earnings, employability, and health too. But we also know that a better educated society is correlated with economic growth and prosperity.

However, the mere focus on the economic effects of human capital should not let us forget about the social and political “returns” of education. Indeed, not only is education one of the main drivers of economic growth, but it is also one of the great equalisers within and across societies. Social justice, intended as equality of opportunities, begins in the classroom, and gaps in the educational systems are gaps that we find in society. In order to go beyond the rhetorical commitment to inclusion and equality of opportunities, there is now, more than ever, a need to invest in an open and collaborative education, based on information-sharing where students are active contributors in connection with teachers.

Moreover, in a world where the spread of democracy cannot be taken for granted anymore, the goals of educating thoughtful citizens of and for a democratic society should permeate how we think about the classroom of the future. Indeed, education is not only about increasing knowledge and skills for personal and social growth, but it is also about the attempt to foster in pupils those values and ideas that make democratic life possible, such as critical reflection, the capacity to balance individual rights and responsibilities, the ability to judge and evaluate ideas on the basis of their intrinsic value rather than their popularity, etc.

In this chapter, we discuss the impact of digital distance learning during COVID-19, along with the need to transform our education and learning models and to invest in physical and intangible infrastructure, based on new needs. We discuss recent data on expenditures on education in the EU, make concrete proposals for a change in the Growth and Stability Pact (GSP)―especially with regard to social investment and infrastructure―and propose new models for financing social infrastructure. We show that the new expansionary policy will increase the demand for “safe assets”, which includes financial instruments for social and green infrastructure. We also stress the role of multi-lateral and national promotional banks and institutions in becoming new “market makers” by increasing “patient capital” going into the real economy. Finally, we look at the InvestEU programme and the Next Generation EU (NGEU) fund and discuss their potential contribution to education investment.

9.1 Digital Learning: A Boost During the Pandemic but and Increaser of Inequality and Stress on Public Investment

Twelve years after the financial and economic crash, Europe seemed to have passed the worst of the recession and the austerity response, only to find itself in the midst of a major health crisis with the COVID-19 pandemic. The response to the pandemic illustrates how austerity measures and a lack of investment in health and human capital left Europe poorly prepared—and how distance learning, tele-medicine, tele-working, and tele-education were boosted at great speed, while the growth and stability rules were upended in 2020.

For many years, the world has tried to reimagine education and lifelong learning for the digital age (Camara, Biglia, Van Looy et al. 2020), but nobody predicted that the greatest transformation would be caused by communicable disease spreading globally. While historically, crises have often been at the origin of major changes in social systems, COVID-19 changed socializing, learning, working, and parenting globally and at a scale never seen before. By mid-April 2020, more than 90% of Europe’s students had been locked out of classrooms for months, and teachers and parents were confronted with teaching, supervising, and guiding young people during a radically changed situation for all. The pandemic demonstrated that investing in human capital in the digital age is essential, while the socialising role of schools and peer groups has been highlighted as never before.

Digital learning received an enormous boost during the pandemic, forcing education professionals and learners to rapidly adapt their competences. It had a positive impact by limiting the loss of human capital for some (The World Bank Group 2020). But for others, adaptation has been slower and not well managed due to multiple factors including the lack of or asymmetric distribution of infrastructure and connectivity; inadequate preparation of teachers, parents, and pupils; some students’ low motivation for learning; social isolation; cyber risks; technical incompatibilities among the learning systems available; technology dependency; and higher costs for the institutions and the families involved.

Estimates for France, Italy, and Germany suggest that students suffered a significant learning loss (time spent on formal learning) when switching from offline to online learning. Using PISA 2006 data, it was demonstrated that one additional weekly hour of instruction over the school year increases test scores by about 6%. Therefore, the loss reported in France, Italy, and Germany reflects the reduction in test score students would be experiencing because of less time spent in learning compared to the amount of time they typically invest when they are in school (Di Pietro, Biagi, Costa, Karpinski, and Mazza 2020).

Learning loss does not impact all students in the same way. An analysis of learning loss during the COVID-19 school closures shows a substantial divergence by socioeconomic status. Therefore, addressing learning loss and implementing large-scale catch-up programmes should be a top priority of the recovery in Europe (Algan, Brunello, Goreichy, and Hristova 2021). Investment in targeted interventions for the most vulnerable could limit the inequality between rich and poor children—which widened during the months of school closure (Nugroho, Pasquini, Reuge, and Amaro 2020; Ionescu, Paschia, Nicolau, Stanescu, Stancescu, Coman, and Uzlau 2020).

Data collected by OECD in 2018, prior to the pandemic, speak for themselves: on average, less than 40% of educators across the EU felt ready to use digital technologies in teaching, with divergences between EU member states (Tiven, Fuchs, Bazari, and Quarrie 2018).

More than one third of 13–14 year old who participated in the International Computer and Information Literacy Study (ICILS) in 2018 (European Commission 2018) did not possess the most basic proficiency level in digital skills. A quarter of low-income households have no access to computers and broadband, with divergences across the EU affected by household income (Eurostat 2019).

The Global Survey on Youth and COVID-19 by the International Labor Organization in 2020 (ILO 2020) found “the impact of the pandemic on young people to be systematic, deep and disproportionate.” The report mentions that COVID-19 left 13% of young people without access to learning; 65% reported having learned less since the pandemic began, and 51% believe their education will be delayed. The pandemic has also had a heavy impact on young workers: 17% stopped working and 42% reported a reduction in income.

The pandemic is clearly far more than a health crisis alone: it is affecting human capital formation and retention, affecting societies and economies, and will have long-term consequences.

To foster the consolidation and the resilience of education, training, and employment in Europe, the European Commission adopted a renewed Digital Education Action Plan, reflecting on the lessons learned from the crisis.

However, soon there will be even fewer resources and potentially lower investment in education and learning. Large debt and slower growth mean that education budgets will not rise in absolute terms as needed. Education budgets as a share of national spending are likely to be squeezed.

When the World Bank analysed education spending after the Global Financial Crisis in 2008, in lower-middle-income countries (LMICs) it observed a large dip in education spending in the immediate aftermath of the crisis that did not recover for several years (The World Bank Group 2020).

Despite high hopes that technology and connectivity would be the answer to learning continuity and reskilling during the crisis, there is not yet any evidence that those can replace teachers or reduce inequality. This isn’t surprising, because we are depending on technologies that many households around the world do not have access to or have not developed the skills to use or to help the students use. In low- and lower-middle-income countries, only 20% of households have access to the internet (The World Bank Group 2020). Even in the EU, stark digital divides along lines of income, race, and geography characterised distance learning experiences, particularly for low-income households.

9.2 Reforming Education and Lifelong Learning, and Ensuring Adequate Investment

|

Box 1. on definitions Formal learning takes place in the education and training system, in universities and in the high-level arts education institutions. It leads to a certification or a vocational qualification that can also be obtained through an apprenticeship. Non-formal learning is an intentionally chosen learning that takes place outside the formal education and training system. It takes place in any organization with educational and training purposes, also in voluntary bodies, national civil service organizations, organizations of the private social sector or enterprises. Informal learning refers to activities carried out in every-day life, at work, at home and in leisure time, even without an intentional choice. Source: European Commission 2018 |

Reform of education and lifelong learning is essential to raise and preserve human capital, facilitate life course transitions, provide a buffer against risks such as unemployment and disease, and guide long-term investors (Vandenbroucke, Hemerijck, and Palier 2011; Hemerijck and Santoni 2019; Fransen, Prodi, and Reviglio 2018).

The world today and the society our children will work and live in are very different to the world our schools and universities were designed to serve decades ago. Formal education was implemented around the time of the first Industrial Revolution; schools then were less about improving children’s human capital than producing a punctual and obedient workforce for the factories. This concept is no longer fit for purpose and reforms are long overdue.

The main drivers for education and lifelong learning reforms are:

- Changing work patterns (the need to work longer and on consecutive careers requiring a high degree of flexibility) and societal realities (new lifestyles) requiring regular upskilling.

- Opportunities offered for the creation of a large learning ecosystem because of the availability of new technologies.

- The need for transformation to adapt to demographic realities (ageing populations, low fertility rates, and economic and political migrations) and location changes (rural-urban movements).

Schools are now only one part of a far bigger learning ecosystem. In the digital age, learning can and must become a lifelong experience. We should aim to improve learning opportunities not only in schools but also in homes, community centres, museums, and workplaces. The internet has created new learning opportunities, enabling online learning communities in which children and adults around the globe collaborate on projects and learn from each other (Resnick 2020).

The unexpected boost for tele-education provided by the COVID-19 pandemic should now require major of structural reforms, and help boost and guide larger long-term investment in those areas. The Economist in January 2021 reported that: “Lots of children could benefit if the pandemic raises awareness that not all pupils are well-served by a one-size-fits-all approach to schooling, and if it directs attention and funding to improving alternative models.”

The content of learning activities, as well as how learning is organised, needs drastic transformation and adaptation. For example, digital native students simply search the internet for information, while many teachers and parents have not grown up with the same digital skillset. With information more widely available and theoretically more accessible, learners could take more ownership and initiative, and educators could provide mentorship, context, and more individualised guidance.

Providing equal opportunities and adequate attention to social and gender inclusion and participation implies that access to quality childcare and education should also be ensured from an early age, including for those children and students with special needs, migrants, minorities, those who are low-income, etc. (Muraille 2020).

Education in the future should be founded on multifunctional community learning centres that provide virtual and actual space, have reliable connectivity, and mobilise teachers/trainers and learners. The future community learning centre focuses on including all potential learners, with greater inclusion of pupils with socioeconomic disadvantages and special educational needs, equipping them with appropriate skills to improve their chances of finding rewarding work, leading independent lives, and actively contributing to society.

Transformation will require re-envisioning the spaces where learning takes place and changing how people learn by using multiple physical and virtual spaces in and outside of formal settings. This would see full individual personalisation of content and pedagogy enabled by leading-edge technology, and drawing on body information, facial expressions, neural signals, and AI (Khan, Ihalage, Ma, Liu, Liu, and Hao 2021).

As the distinction between formal and informal learning blurs and eventually disappears, individual learning can advance by taking advantage of collective intelligence being rapidly accessible through new technologies, helping us to solve real-life problems.

Technologies are changing not only what students should learn, but also what they can learn. Fresh ideas are now accessible through creative use of digital technologies. For example, you can now use simulations to explore ecosystems, economic systems, and immune systems in ways that were previously not possible.

In terms of bricks and mortar, the community learning centres should be constructed as passive buildings, with sustainable design working in two ways. First, because of low energy costs, additional costs will be earned back in the long run. Second, such designs trigger children to reflect on environmental and sustainability issues. Spaces can be used for different purposes, and areas such as sports facilities and libraries could be used by third parties in the evening or weekends. Investment must be made in digital and ICT facilities and connectivity, such as digital whiteboards and programmable robots.

The returns on investing (ROI) in such centres could include savings on welfare and assistance, in addition to economic returns.

Universities could become hubs for advanced learning, research, and innovation for a larger geographical area, and facilitate the provisions for a learning society. These hubs would be interconnected with local businesses, public bodies, and other research institutes, attracting private capital to develop innovative technologies, incubate startups, and develop new business models.

ROI from such advanced learning hubs would need to include the wider economic benefits of innovation and impacts on productivity and on competitiveness.

Current expenditure may not need to increase significantly everywhere, but instead be reallocated towards the new approaches. However, some geographic areas do have critically underfunded education and lifelong learning. This is especially the case in regions that cut investment in social sectors drastically with austerity measures after the financial crisis. This lack of investment in health, human capital, and connectivity left Europe poorly prepared for the COVID-19 pandemic.

Capital expenditure for education and lifelong learning in the EU was approximately €65 bn in 2015 (national accounts data from Eurostat), with the UK, Germany, France, and the Netherlands accounting for around two thirds of the total (Fransen, del Bufalo, and Reviglio 2018).

- Spain, Italy, Austria, Denmark, Ireland, and Slovakia invest 0.3 % of their GDP or less

- Czechia, Latvia, Lithuania, Estonia, Finland, and the Netherlands invest 0.8 % or more

Per pupil, Spain spends €183 and the Netherlands €1,283.

|

Box 2. On Education & lifelong learning Total estimated at +/- €65 bn. Education infrastructure spending by:

Source: Fransen, del Bufalo, and Reviglio 2018. |

It was estimated that a minimum additional capital investment is needed annually of 15 bn per annum (Fransen, del Bufalo, and Reviglio 2018).

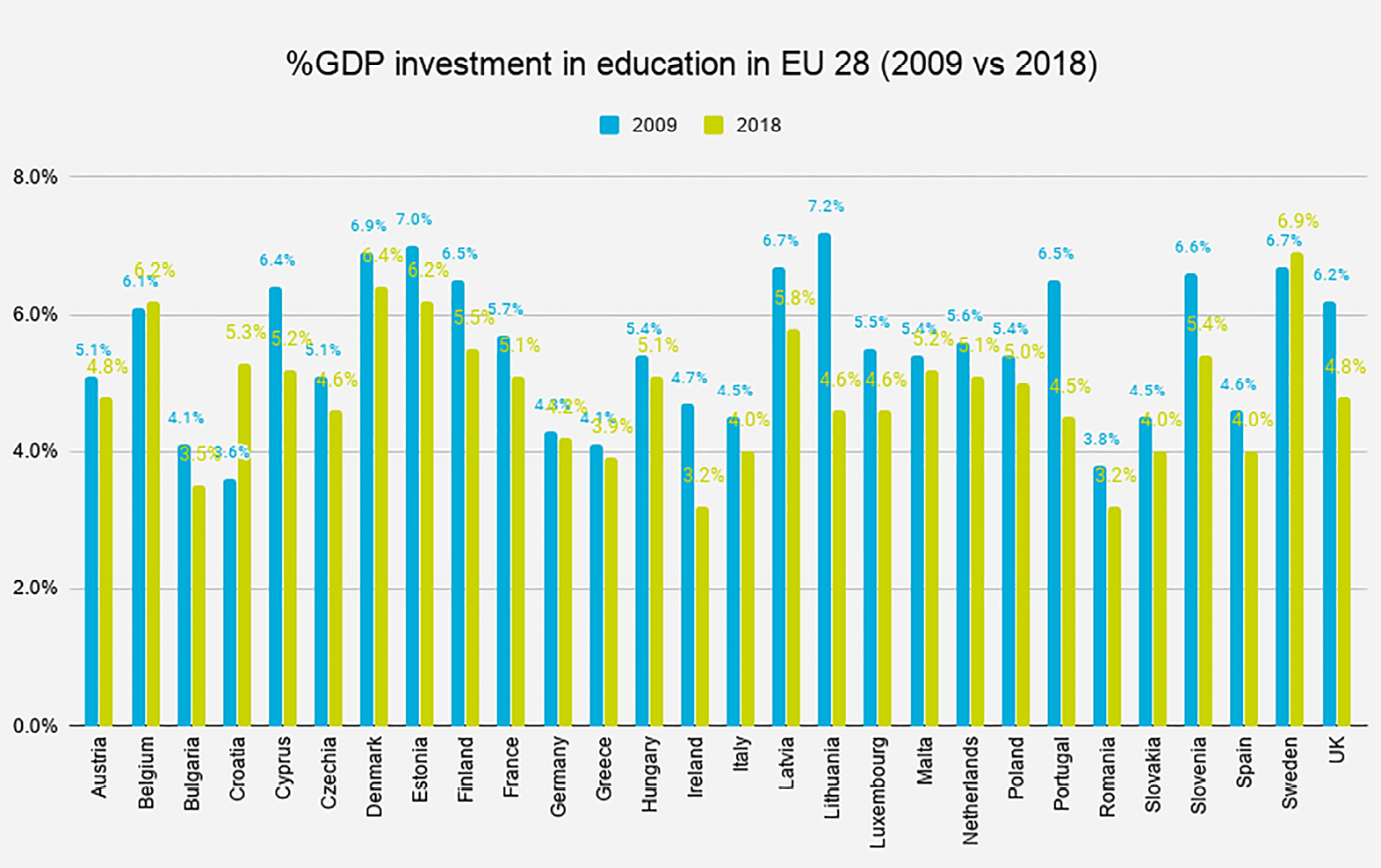

The total average public expenditures for education also decreased constantly from a share of 5.5% of GDP in 2009 to only 4.7% in 2018, representing a 17% disinvestment since 2009. While the absolute amount of resources destined towards education and training has increased, it is the percentage over GDP that gives the real measure of the importance.

The breakdown of the data by countries in 2018 gives us an even grimmer image. Only three countries have increased their percentage of investment in education: Belgium (+0.1%), Sweden (+0.1%), and Croatia (+1.7%). On the other side of the scale, most countries have registered a decrease: Cyprus (-1.2%), Slovenia (-1.2%), Ireland (-1.5%), Portugal (-2.0%), and Lithuania (-2.6%).

Fig. 1 % GDP Investment in Education in EU-28 (2009 vs 2018).

Source of data: Lifelong Learning platform 2021, Europe’s share of GDP for education and training has never been this low. A comparative analysis, 23rd March 2020.

However, while investing sufficient long-term resources in reformed education and learning is critical, according to OECD, the relation between expenditure and learning outcomes breaks down after a certain threshold is passed: after reaching a minimum level of inputs, more resources do not necessarily imply an improvement (Canton, Thum-Thysen, and Voigt 2018).

It is important to note that the figures mentioned above refer to formal education and do not capture potential investment effort made in informal and non-formal education contexts.

9.3 New Models for Financing Social Infrastructure for Education

How shall we finance such great needs of education infrastructure within the huge transition which we tried to describe above, which will characterise our educational system and lifelong learning in the future, without weighing too much on high public debts across the EU?

Schools and related education infrastructure were traditionally financed directly by local authorities, eventually with contributions from the state, by raising long-term debt from public institutions. The interest rates of debt were very close the one paid on sovereign debt, because institutions providing the financing were using funding guaranteed by the state. The technical capacity of local authorities was much better than it is today, but the infrastructure was also simpler and more basic. Today, as we have seen above, much more complex education infrastructure is needed, and technical capacities to project, build, and manage must be much more sophisticated.

In this section, we will try to describe the new innovative schemes which are emerging across the EU in financing education infrastructure.

To accommodate this changing world, the model that is used to finance infrastructure in the EU is rapidly changing. With public budgets under stress and a huge demand for new infrastructure due to green and digital revolutions, we will see a growing involvement of private and institutional investors in public-private initiatives, including infrastructure for education.

Institutional long-term investors with more than $130 tn of assets under management at the global level are looking at “education infrastructure” as a new, fully-fledged asset class to invest in (OECD 2013; Garonna and Reviglio 2015; Inderst 2021). Moreover, as we shall discuss later, there is a growing demand for “safe assets” by long-term investors, to match long-term assets to long-term liabilities.

Economic infrastructure, such as energy, transport, and telecommunications, produces cashflows on its own that can repay the cost of construction. Such infrastructure involves construction, tariffs, and market risks, and this makes their yield higher. With social infrastructure mostly financed by public money and paid for by taxpayers, it does not have the same risks (Figure 4) and the risk/yield profile is lower. Both types of infrastructure investment are attractive to institutional investors who like to diversify the risk in their portfolios.

Social infrastructure investment has distinctive features that distinguishes it from economic infrastructure (EDHEC-Risk Institute, February 2012; Fransen, Prodi, and Reviglio 2018). Generally, it tends to be illiquid investment. This type of investment has long time horizons and, if equity is invested, it becomes difficult to exit. However, on the debt side, ever larger, deeper, and more liquid social and green bond markets are emerging and may overcome this problem, making it far more attractive for institutional and even retail investors to invest in education infrastructure. Moreover, default rates and recovery rates of infrastructure debt, in general, are relatively lower than high-rated corporate debt.1

Infrastructure projects in education (and health) are usually relatively small. According to EDHEC-Risk Institute (EDHEC 2012), roughly 99% of existing social infrastructure projects in Europe entail a total capital investment of less than €1 bn, with the great majority of projects below €30 m. The small-average size is good for spreading risk (portfolio diversification), but it reduces cost synergies during the structuring and arranging phase. Unlike many economic infrastructure projects, such as toll roads, ports, airports, or power generation plants, which usually collect revenue from end users, social infrastructure projects often rely on the availability of fees paid by the public sector. Therefore, from a financial (and financing) perspective, it is key to bear in mind that the cashflow streams to repay the financing of social infrastructure investment come ultimately from public budgets. This means that education infrastructure investment risk is only slightly higher than sovereign bonds’ risk. To overcome the potential small-average capex size “bottleneck” while preserving the sought-after portfolio diversification, a solution could be the efficient “bundling” of similar education infrastructure projects. In fact, when bundled into a single, larger procurement, a beneficial structure can be implemented to address:

- A group of similar assets across multiple sites.

- An assortment of different assets at a single site.

- Different assets across multiple sites.

In addition, the bundling of similar assets can save on design and construction costs, as similar materials can be used and bought in bulk. More standardized design and construction processes also create the opportunity to save on long-term maintenance due to similar replacement parts and equipment used.

Availability payments from the public sector are usually agreed beforehand and tend to be inflation-linked. Predictable and steady real returns are attractive for investors.

The small-average capital investment size of social infrastructure projects, however, makes direct infrastructure investment unattractive to large long-term investors, as they face relatively high active management costs for such modest investment. Therefore, financial intermediaries are key to channeling institutional investors towards social infrastructure. Institutional investors have the possibility of investing in equity through listed infrastructure funds, unlisted intermediary funds, or directly at the SPV level.

Political and regulatory risks, often linked, are another key dimension of social infrastructure investment. Public policies might change over the extended life span of an asset. Governments may renege on commitments and regulators may change the regulatory framework.

Even so, innovative solutions for financing education, health, and social housing at a sustainable cost for European public finances are becoming more widespread. In the main, direct contracts by the public authority to a private enterprise are financed by long-term loans. Quantitative easing means the spreads between EU member states have been reduced significantly, but this will not last forever, and local authority debt offers little room for maneuvering.

It will be important to crowd in as much institutional and private investment in social infrastructure financing as possible. The added value is not merely providing financing so much as the quality of the schemes required to attract investors and others. The public sector, generally, does not have the necessary technical competencies to effectively plan, build, and manage complex projects. If they had such skills, as we already mentioned, it would be cheaper to finance schemes directly through sovereign funding. The complexity of today’s integrated and eventually bundled sets of infrastructures is typically handled by the many specialised players who are generally not within the public sector. To ensure that every single stakeholder play fair, promotional banks and the EIB, CEB, and other institutional regional platforms can play a crucial role in organising and giving technical assistance to public sector promoters. Moreover, other contributions from various sources can be “blended” to reduce direct costs to taxpayers (Prodi and Reviglio 2019).

In general, we need a clearer and friendlier system of rules by Eurostat to understand if a project is an on- or off-balance sheet (Fransen, del Bufalo, and Reviglio 2018).

Now consider, for instance, that a municipality, group of municipalities, or other public administration needs to invest in education or other social infrastructure. They can decide to implement it through innovative forms of institutional public-private partnerships or investment platforms:

- The local administration will pay for the work through an availability fee that will affect expenditure year after year.

- Costs can be kept down by a national or European grant, public guarantees, or tax incentives.

- Fiscal space can be provided through a special clause for social investment.

- Contributions in kind can be made using local public heritage assets, land, or buildings, for example.

- An institutional “technical assistance” system can ensure risks and profits are well distributed between public and private sectors.

This solution, known as “blending”, helps to contain the cost of public administration and increase the quality and timing of the construction of infrastructure (EPEC 2017; Fransen, Prodi, and Reviglio 2018; Inderst 2021). There is also the possibility of creating public-private-institutional vehicles that may bundle different projects to reach a critical mass for investors and to achieve similar high quality across several municipalities or regions involved in a bigger project.

Why are institutional investors so interested in infrastructure investment? Because infrastructure is a “safe asset”, and there was a huge shortage of this type of financial instrument after the 2008 financial crisis. Indeed, the importance of safe assets has become central since that crisis.

Safe assets are a pillar of an ordered financial system. They are a store of value for institutions, including pension funds and insurance companies, as they allow them to match long-term assets to long-term liabilities. They are also structural elements of commercial bank balance sheets (Reviglio 2020).

More generally, they are used by financial institutions to meet regulatory requirements and provide collateral for borrowing additional funds. These stores of value come in many forms: cash, bank deposits, US Treasury bills, European government bonds, projects bonds, recovery bonds, infrastructure bonds, green and social bonds, and bonds raised by the EIB and by national promotional banks and institutions. They can include high-rating corporate bonds, stocks, and equity in infrastructure funds and/or projects.

There is another reason why education and social infrastructure in general are considered good investments for institutional investors. They are generally “green” and/or come with strong social externalities at a point when markets’ short-termism has not yet priced upcoming taxation on polluting investment.

To hedge climate risks, investors can either divest polluting investment in their portfolio, invest in low-carbon indices, or invest in green and social bond companies.2 Indeed, investing in properly constructed decarbonised investments, such as those in education infrastructure, can allow long-term passive investors to hedge climate risk without sacrificing financial returns (Andersson, Bolton, and Samama 2015; see also Bolton, Depres, Pereira da Silva, Samama, and Svartzman 2020).

Now, with the Next Generation EU fund (2021–27), the American Rescue Plan Act (2021–31), and other recovery plans in many countries, the number of safe assets will grow at unprecedented levels. This is a unique opportunity to move to a more long-term finance approach that is oriented towards infrastructure and the real economy.

9.4 The Golden Rule for Social Investment, Reforming the Stability and Growth Pact, and Next Generation EU

For many years, it was argued that investing in education and health should be an investment and not a cost in budgetary terms, and it was vital to boost investment in social infrastructure. But despite fine words and new instruments doing some of this, the pandemic has shone a light on failings.

Because of the pandemic, the EU institutions suspended the Stability and Growth Pact (SGP) rules for government spending and debt reduction through activation of the General Escape Clause. This will remain in place until the end of 2022. The pandemic led to a remarkable consensus among EU member states on the need to provide fiscal stimulus beyond the levels allowed by the rules. As the recovery continues, different views on debt consolidation are likely to emerge and old differences to re-emerge. However, returning to pre-coronavirus rules would be counterproductive. The need to reform the EU’s fiscal framework has, in the meantime, gained traction and could be an opportunity to introduce meaningful reforms to boost social investment and social infrastructure investment sooner rather than later.

The priority now should be to allow for more long-term public investment, including in social sectors. This raises the question of whether fiscal rules can be amended to encourage countries to step up their national social investment strategies while maintaining the overall integrity of a rules-based budgetary framework, including the Stability and Growth Pact (SGP) 3% deficit and 60% debt limits, and crowding in private sector investment at the same time.

Public investment in general, as a % of GDP, continued to decrease years after the Global Financial Crisis and only recently started picking up, slightly before the pandemic. However, the slight increase in public investment suffers from a pro-cyclical bias and a short-term orientation, while still insufficiently targeting social investment in human capital formation and in social infrastructure.

Investing in education and in social infrastructure in general should be given special consideration, and it is unclear if the new financing instruments of the EU will do so at all. In the 2021 European Outlook on Public Investment, in the chapter on Social Investment and Infrastructure (Hemerijck, Mazzucato, and Reviglio 2020), a Golden Rule was proposed to exempt human capital stock spending from the euro area fiscal rulebook for 1.5% of GDP for around a decade, as a flagship initiative of the new European Commission. Today, this move has become even more urgent.

The Next Generation EU fund comprises the Recovery and Resilience Facility and several other EU programmes. It is clearly a missed opportunity that social infrastructures did not receive a unique dedicated “window”, but instead are spread across other missions and programmes. This is most likely because they include strong digital, green, and social cohesion components. However, this approach goes against EU best practices around highly integrated systems (school, health, housing, etc.). In InvestEU, for example, more than sixty-five guaranteed funds and twelve financial instruments are combined in only four policy windows, as also recommended in the 2018 “Prodi Report” on social infrastructure (Fransen, del Bufalo and Reviglio 2018). The policy windows in InvestEU are sustainable infrastructure, research, innovation and digitalisation, SMEs, and social investment and skills. From this perspective, Next Generation EU is a step backwards. Digital, green, and transport are undoubtedly essential elements of EU recovery, competitiveness, and social cohesion. However, integrated social infrastructure and investment will be as important, if not more so, especially early in the post-pandemic period. Next Generation EU does not have such an integrated view. As a result, education, health, and social housing are spread here and there without a coherent view, and with fewer resources directly dedicated to these sectors, including education. Therefore, we should aim to integrate more successfully the elements contained in the EU Plan, including digital and green, alongside renewed investment in education, health, and social housing.

9.5 Conclusion

Since the 2008 crisis, investment in education has been greatly reduced. The austerity policies which have characterised the EU have had a strong negative impact on education, health, and social housing. This is partially because social infrastructure is largely financed by local authorities, which have seen their budgets substantially reduced.

We demonstrated that the gap between the actual investment and the needs is large in most of the EU member states. Now, because of the suspension of the Growth and Stability Pact since the COVID-19 pandemic, more resources should be available, at least temporarily. Moreover, the Next Generation EU instrument provides substantial funds for digital and green transition, including education infrastructure.

The world today and the society our children will work and live in are very different. Our schools and universities were designed to serve the needs of a very different society. Formal education was implemented around the time of the first Industrial Revolution; schools then were less about improving children’s human capital than producing a punctual and obedient workforce for the factories. This concept is no longer fit for purpose and reforms are long overdue.

The schools of the future are going to be very different from those of the past. Changing models of education, plus more pervasive digitalisation, will lead to the need to restructure and build new schools. Moreover, lifelong learning has become even more important than in the past due to the transformation of the job market. Much more mobility from one type of job to another is going to be required.

How will those great needs of education infrastructure be financed in the future?

We described innovative schemes which are emerging across the EU in financing school and other education infrastructure.

It will be important to crowd in as much institutional and private investment in education infrastructure financing as possible. The added value, we argued, is not merely providing financing so much as the quality of the schemes required to attract investors and others. The public sector, generally, does not have the necessary technical competencies to effectively plan, build, and manage complex projects. If they had such skills, it would be cheaper to finance schemes directly through sovereign funding. The complexity of today’s integrated and eventually bundled sets of infrastructures is typically handled by the many specialised players who are generally not within the public sector. To ensure that every single stakeholder play fair, promotional banks and the EIB, CEB, and other institutional regional platforms can play a crucial role in organising and giving technical assistance to public sector promoters. Moreover, other contributions from various sources can be “blended” to reduce direct costs to taxpayers.

Institutional long-term investors are looking at “education infrastructure” as a new fully-fledged asset class to invest in.

Social infrastructures have interesting characteristics for private/institutional investors, such as low volatility of returns (payments from the public sector are generally agreed ex ante and tend to be linked to inflation) and low correlation with the resulting risks from other assets (the nature of a social infrastructure investment reduces exposure to market risk and capital market volatility), high value of physical assets that can act as collateral for loans, and a stable long-term investment prospect term (twenty to thirty years).

Institutional investors have the option of investing capital through infrastructure funds, investment platforms, or directly into projects.

Why are institutional investors so interested in infrastructure investment? Infrastructure is a typical “safe asset”, and there was a huge shortage of this type of financial instrument after the 2008 Global Financial Crisis. Indeed, the importance of safe assets has become central since that crisis.

Public debt of advanced economies is projected to raise from 87% in 2019 to 109% in 2021 (IMF data 2021): in the US from 103% to 125%, in the Eurozone from 86% to 99%, in the UK from 84% to 111%, and in Japan from 232% to 258%.

The US has passed an Infrastructure and Job Bill worth $1 tn (with a very large component in social investments); the Next Generation EU fund, at the level of current prices, is worth around €800 bn over the next six years.

Finally, COVID-19 may help capital markets overcome the so-called “safe asset trap” (i.e., the lack of long-term financial instruments that match the long-term liabilities and assets of institutional investors, such as pension funds and insurance companies).

Investment in education infrastructure should be as great as it ever has been in the history of the EU. So, it is time to be brave. Much of the future of our new generation depends on education systems which properly prepare students and workers for a changing world.

References

Khan, A.N., A.A. Ihalage, Y. Ma, B. Liu, Y. Liu and Y. Hao (2021) “Deep Learning Framework for Subject-Independent Emotion Detection Using Wireless Signals”, PLOS ONE, 16(2): e0242946, https://journals.plos.org/plosone/article?id=10.1371/journal.pone.0242946 .

Algan, Y., G. Brunello, E. Goreichy and A. Hristova (2021) Boosting Social and Economic Resilience in Europe by Investing in Education, February 2021.

Arezki, R., P. Bolton, S. Peters, F. Samama and J. Stiglitz (2016) “From Global Savings Glut to Financing Infrastructure: The Advent of Investment Platforms”, IMF Working Paper 16(18), https://www.imf.org/external/pubs/ft/wp/2016/wp1618.pdf.

Bassanini, F. (2012) “Financing Long Term Investment after the Crisis: A View from Europe’, in Sovereign Wealth Funds and Long-Term Investing, ed. by P. Bolton, F. Samama, J. E. Stiglitz (New York: Columbia University), pp. 37–44, https://doi.org/10.7312/columbia/9780231158633.001.0001.

Bassanini, F. and E. Reviglio (2011) “Financial Stability, Fiscal Consolidation and Long-Term Investment after the Crisis”, OECD Journal: Financial Markets Trends 1:37–75, https://doi.org/10.1787/fmt-2011-5kg55qw1vbjl.

Bassanini, F. and E. Reviglio (2015) “From the Financial Crisis to the Juncker Plan”, in Investing in Long-Term Europe. Fixed, Re-Launching Fixed, Fixed, Network and Social Infrastructure, ed. by P. Garonna and E. Reviglio (Rome: LUISS University Press), pp. 59–80.

Bassanini, F., G. Pennisi and E. Reviglio (2015) “Development Banks: From the Financial and Economic Crisis to Sustainable and Inclusive Growth”, in Investing in Long-Term Europe. Re-launching fixed, Network and Social Infrastructure, ed. by P. Garonna and E. Reviglio (Rome: LUISS University Press), pp. 312–16.

Bolton, P., M. Depres, L.A. Pereira da Silva and P. Samama (2020), The Green Swan―Central Banking and Financial Stability in the Age of Climate Change, January 2020.

Caballero, J. and E. Farhi (2017) “The Safety Trap”, The Review of Economic Studies Limited. Harvard University and NBER.

Camara, A., A. Biglia, B. Van Looy, D. Guttieres, D. Tilbury, E. Artvinli, G. Kostakos, J. M. Hughes, K. Ohnishi, L. Fransen, L. Neves, M. Hartnett, M. van der Ree, M. Denis, N. Selwyn, N. De Smyter, N. Oliver, P. Seshaiyer, P. Bettelli, R. Linturi, S. Downes, V. Vandeweerd and W. Liu (2020) Adapting Education Systems to a Fast Changing and Increasingly Digital World. Covid 19 education alliance (Covidea), Website Platform for transformative technologies (P4TT).

Cantillon, B. and F. Vandenbroucke (eds) (2014) Reconciling Work and Poverty Reduction. How Successful are European Welfare States? Oxford: Oxford University Press.

Canton, E. A. Thum-Thysen and P. Voigt (2018) Economists’ Musings on Human Capital Investment Efficiency in Public Spending on Education in EU Member States, Discussion paper 081, June 2018, European CommissionDella Croce, R. and J. Yermo (2013) “Institutional Investors and Infrastructure Financing”, OECD, November 6 2013.

EDHEC-Risk Institute (2012) Pension Fund Investment in Social Infrastructure. Insights from the 2012 Reform of the Private Finance Initiative in the United Kingdom, https://www.edhec.edu/sites/www.edhec-portail.pprod.net/files/publications/pdf/edhec-publication-pension-fund-investment-in-social-infrastructure-f_1332412681078.pdfjpg.

Habib, Livio Stracca, L. and F. Venditti (2020) The Fundamentals of Safe Assets, Working Paper Series No 2355, January 2020.

Engel, E., R. Fischer and A. Galetovic (2020), When and How to Use Public-Private Partnerships: Lessons from the International Experience, NBER Working Papers Series 26766.

Ehlers, T. (2014) Understanding the Challenges for Infrastructure Finance, BIS Working Papers 454, https://www.bis.org/publ/work454.pdf.

EIB (2018) EIB Investment Report 2018/2019: Retooling Europe’s Economy. Luxembourg: European Investment Bank, https://www.eib.org/attachments/efs/economic_investment_report_2018_en.pdf.

EPEC (2016) A Guide to the Statistical Treatment of PPPs, https://www.eib.org/attachments/thematic/epec_eurostat_statistical_guide_en.pdf.

European Commission (2016) Report on Public Finances in EMU, Institutional Paper 045, https://ec.europa.eu/info/sites/info/files/ip045_en_0.pdf.

European Commission (2018) The International Literacy Study (ICILS) Findings and Implications for Education Policies in Europe. European Commission, Validation of Formal and Non formal learning, eacea.ec.europa.eu, https://ec.europa.eu/education/resources-and-tools/document-library/the-2018-international-computer-and-information-literacy-study-icils-main-findings-and-implications-for-education-policies-in-europe_en.

European Commission (2020) Macroeconomic Database, Ameco.

European Expert Network on Economics of Education, EENEE (2020) Analytical Report No.42, prepared for the European Commission.

Eurostat (2019) Digital Economy and Society Statistics―Households and Individuals.

Foster, S. and C. Iaione (2016) “The City as a Commons”, Yale Law & Policy Review 34: 281–349, https://digitalcommons.law.yale.edu/cgi/viewcontent.cgi?article=1698&context=ylpr.

Foster, S. and C. Iaione (2019) “Ostrom in the City: Design Principles and Practices for the Urban Commons”, in Routledge Handbook of the Study of the Commons, ed. by D. Cole, B. Hudson and J. Rosenbloom (London: Routledge), pp. 235–55, https://doi.org/10.4324/9781315162782-19.

Fransen, L., G. del Bufalo and E. Reviglio (2018) Boosting Investment in Social Infrastructure in Europe. Report of the HLTF Force on Investing in Social Infrastructure in Europe chaired by Romano Prodi and Christian Sautter. Luxembourg: Publications Office of the European Union, https://www.fondazioneifel.it/notizie-ed-eventi/item/download/2376_ee5d868e16ae749 daced6f41cce3709c.

Garonna, P. and E. Reviglio (eds) (2015) Investing in Long-Term Europe. Fixed, Re-Launching Fixed, Fixed, Network and Social Infrastructure. Rome: LUISS University Press.

Gorton, G. (2017) “The History and Economics of Safe Assets”, Annual Review of Economics, 9(1): 547–86.

Gourinchas, P.-O. and O. Jeanne (2012) Global Safe Assets, BIS Working Papers 399, Bank for International Settlements.

Hemerijck, A. (2013) Changing Welfare States. Oxford: Oxford University Press.

Hemerijck, A. (ed.) (2017) The Uses of Social Investment. Oxford: Oxford University Press, https://doi.org/10.1093/oso/9780198790488.001.0001.

Hemerijck A. and M. Santoni (2019) Rescue, Not Renewal: Social Investment for the Future Wellbeing for Social Europe.

Hemerijck, A. and S. Ronchi (2020) “European Welfare States’ Detour(s) to Social Investment”, in The Oxford International Handbook of Public Administration for Social Policy: Promising Practices and Emerging Challenges, ed. by J. Boston, E. Ferlie, F. Filgueira, Y. Jing, E. Ongaro and V. Taylor. Oxford: Oxford University Press.

Hemerijck, A., M. Mazzucato and E. Reviglio (2020), “Social Investment and infrastructure”, in F. Cerniglia and F. Saraceno (eds), A European Public Investment Outlook. Cambridge: Open Book Publishers, pp. 115-34, https://doi.org/10.11647/obp.0222.07.

Inderst, G. (2017) “Social Infrastructure Investment: Financing Sources and Investor Perspective”, HLTF SI, Draft for discussion, June 15.

Inderst, G. (2020) “Lessons learned from the United Kingdom and Europe” in Innovation in Infrastructure Delivering: How Government and Institutional Investors Can Lead an Infrastructure Renaissance”, in Institutional Investing in Infrastructure, A Supplement to the November 2020 i3, a publication of Institutional Real Estate, Inc.

Ionescu, C.A., L. Paschia, N.L.G. Nicolau, S.G. Stanescu, V.M.N. Stancescu, M.D. Coman and M.C. Uzlau (2020) “Sustainability Analysis of the E-Learning Education System during Pandemic Period—COVID-19 in Romania,” Sustainability, MDPI, Open Access Journal, 12(21): 1–22, October.

Di Pietro, G., Biagi, F., Costa P., Karpiński Z., Mazza, J. (2020) The Likely Impact of Covid 19 on Education, 30275 EN Publication office of the European Union, Luxemburg.

ILO Global Report on Youth & COVID-19 (2020) Impacts on Jobs, Education, Rights and Mental Well-being.

Lifelong Learning Platform (2021) Europe’s Share of GDP for Education and Training Has Never Been This Low: A Comparative Analysis, 23rd March 2020.

Luna-Martinez, J. and L. Vicente (2012) “Global Survey of Development Banks”, World Bank Policy Research Working Paper 5969, http://documents.worldbank.org/curated/en/313731468154461012/pdf/WPS5969.pdf.

Marjorie, B., E. Tiven, R. Fuchs and A. MacQuarrie, Evaluating Global Digital Education: A Student Outcomes Framework, OECD.

Muraille, M. (2020) From Emergency Remote Learning to a New Digital Education Plan: An EU Attempt to Mainstream Equality into Education”, European Policy brief No 66.

Mazzucato, M. and C. Penna (2016) “Beyond Market Failures: The Market Creating and Shaping Roles of State Investment Banks”, Journal of Economic Policy Reform 19(4): 305–26, https://doi.org/10.1080/17487870.2016.1216416.

Nugroho, D., C. Pasquini, N. Reuge and D. Amaro (2020) COVID-19: How Are Countries Preparing to Mitigate the Learning Loss as Schools Reopen? Trends and Emerging Good Practices to Support the Most Vulnerable Children, an Innocento Research Brief, UNICEF.

OECD (1998) Human Capital Investment: An International Comparison, OECD Publishing, Paris.

Prodi, R. and E. Reviglio (2019) A New Fund for Europe. The Creation of a New European Social Bond Would Help EU Member States Meet their Infrastructure Needs, OMFIF Bulletin.

Resnick, M. (2020), Rethinking Learning in the Digital Age, Cambridge, Mass.: MIT Press.

Reviglio, E. “Exacerbating Public Debt”, in OMFIF Global Public Investor, ed. by Danae Kyriakopoulou (London: OMFIF Ltd), pp. 132–33.

Schmid, G. (2015) “Sharing Risks of Labour Market Transitions: Towards a System of Employment Insurance”, British Journal of Industrial Relations 53(1): 70–93, https://doi.org/10.1111/bjir.12041.

The Economist (2021) How Covid 19 Is Inspiring Education Reform.

The Economist (2021) Closing the World’s Schools Caused Children Great Harm.

The World Bank Group (2020) The Human Capital Index 2020 Update. Washington DC.

1 See Moody (2017) Default and Recovery Rates for Project Finance Bank Loans, 1983–2015, Default Research, Moody’s Investors Service, 6 March 2017; Moody (2017) Addendum: Infrastructure Default and Recovery Rates, 1983–2015, Default Research, Moody’s Investors Service, 27 April 2017; and Moody (2016) Infrastructure Default and Recovery Rates, 1983–2015, Default Research, Moody’s Investors Service, 18 July 2016.

2 There exist two main types of low-carbon indices: “pure-play” indices, including stakes of green (and social) companies, and “decarbonised” indices (or “green beta indices”), constructed by excluding the largest GHG emitters from a benchmark index.