11. Assessing the Quality of Green Finance Standards

© 2022 Chapter Authors, CC BY-NC 4.0 https://doi.org/10.11647/OBP.0328.11

Green finance is a rapidly growing mechanism for facilitating investment in sustainable transition. This chapter reviews the generic process in labelling green finance products governed by different green finance standards. The key differences in green finance standards are assessed, including governance, scope, and definition of green. Although the EU has been widely considered as the global leader in green finance, the recent inclusion of nuclear and natural gas in the sustainable finance category has generated controversy. This chapter also identifies current green finance standards whose added value is not clear. In other words, it is uncertain whether green finance is purely a statistical exercise or could bring additional sustainable benefits for the community.

Climate change is one of the greatest challenge humans face in this century. Mobilising investment and finance to address climate change is key for unlocking actions on climate change across countries. The estimated investment required to achieve the climate mitigation goal set up by the Paris Agreement range from US$1.6 trillion to US$3.8 trillion annually between 2016 and 2050, while the tracked annual flow of climate finance was US$579 billion on average, based on data in 2017 and 2018, as illustrated in Figure 11.1 (in the following text). Despite a significant growth in climate finance flow, the gap remains quite substantial. In response to the vast financing gap, the effectiveness of climate investment and finance must urgently be maximised.

Developing green finance, such as green bonds, green funds, or green loans, has given hope as a potential solution for bridging the funding gap for climate change. Since the first green bond was issued in 2007 by the European Investment Bank (EIB), the green finance market has been growing rapidly in both scale and market coverage. Green bonds remain the dominant asset in terms of the green finance market share. In 2021, green, social, sustainability, sustainability-linked and transition themed debt reached USD$1 trillion with growth spearheaded by green bond issuance. This represents a twenty-fold increase from 2015, and accounts for 10% of global debt markets.

In spite of the rapid growth of the green bond market, there are concerns of “greenwashing”. For example, Tariq Fancy, former chief investment officer of the largest asset management firm Blackrock, which has US$ 8.7 trillion assets under management (AUM), has suggested that “Wall Street is greenwashing the economic system and, in the process, creating a deadly distraction.”. In response to concerns, the US Securities and Exchange Commission (SEC) created a Climate and ESG Taskforce to “proactively identify ESG-related misconduct” in March 2021.

The EU has always led the development of green investment practices in the world. In May 2022, MEPs passed a text seeking to better regulate the green bond market, improve its supervision, reduce greenwashing, and add clarity when money goes to gas or nuclear energy. This chapter will review how green finance standards have been defined and applied, identify the current problems, and propose measures the EU could adopt in establishing a future-proof green finance standard system.

11.1 What Are Green Finance Standards?

The green finance standards system generally refers to a series of classification methods and measurement indexes that are established to identify, confirm and track green assets and green investment with the orientation of international, regional or national green development strategic goals. A variety of international and national green credits, green bonds, green stock indexes, green development funds, green insurance and other related financial products and services have been widely established, and various green finance standards systems with different connotations and extensions have been adopted. In general, a green finance standards system includes the following six elements:

- Sectoral Taxonomy/Classification;

- Identification and Standards;

- Proceeds Requirements;

- Incentives;

- Verification and Labelling; and

- Post Investment Monitoring

Currently, there are three major types of widely recognised green finance standards systems. The first type is a series of voluntary principles issued by financial institutions or organisations, including the Green Bond Principles (GBP), the Equator Principles (EPs) and the Climate Bonds Standard (CBS), the World Bank’s Green Bond Process Implementation Guidelines and the Asian Development Bank’s (ADB) Green Bond Framework. The European Commission is issuing its Green Bond Standard and ISO 14100 is developing its Guidance on Environmental Criteria to Support Green Finance. The second type is assessment systems introduced by financial services institutions, mainly developed by assessment and rating agencies, such as Moody’s Green Bond Assessment System and Standard & Poor’s Green Evaluation System. The third type is systems issued by the relevant regional or national departments, including the European UnionGreen Bond Standard that the EU is pushing for, and China’s Green Credit Guidelines, Green Bonds Issue Guidelines, Green Bonds Supporting Project Directory (2015 edition), and Green Industry Guidance Catalogue (2019 edition).

The industry category assessment of green finance standards is the first step in identifying green financial assets and industry categories, including primary and secondary catalogues. The green finance standard catalogue has a high degree of convergence, covering areas such as renewables, energy efficiency, pollution prevention and control, water management, clean and low-carbon transportation, and green and low-carbon buildings. There are two significant differences in the industry classification of green finance—China’s green finance standards generally do not include climate change adaptation. In contrast, international green finance standards include climate mitigation and adaptation-related fields. The question of whether coal, nuclear power and rail transit should be included in the green finance category is still controversial. International green standards generally explicitly exclude fossil fuels except for the use of CCUS technology. The Green Credit Guidelines issued by the China Banking Regulatory Commission (now the CBIRC) in 2012 also did not cover the coal sector. However, the Green Industry Guidance Catalogue released by NDRC in 2019 still includes clean coal use. Nonetheless, the categories related to coal use are removed in the 2021 Green Bond Guideline released jointly by NDRC and PBOC.

Compared to the simple filtering criteria of the fields in the international standards, some of China’s green finance standards are more targeted for technology application. For instance, the Green Industry Guidance Catalogue of the NDRC sets the scale or the technical threshold for the industry green finance project. These are, for example, minimum capacity for coal-fired thermal power units; the industry standard for energy-saving technological transformation projects; and clear, quantified indicators of the photoelectric conversion efficiency and the attenuation rate of polysilicon components (monocrystalline silicon components, high concentrated photovoltaic modules, membrane cells components) of photovoltaic power generation projects. Establishing industry thresholds complicates the certification process but avoids the outdated capacities of industries being identified as green assets.

There are different ways to identify green assets, including sector identification, sector plus threshold identification, negative list/exclusion identification and a scoring system. The scoring system can be further extended into two types, a qualitative evaluation system (according to expert opinions) and a quantitative evaluation system (according to quantitative data). The GBP, CBS and EU’s forthcoming classification schemes are identified by sector. For example, under these three principles, all wind power assets are simply classified as green assets. The operation cost of sector identification is low, but it is difficult to exclude the critical influencing factors beyond the green attribute, such as social influence and backward production capacity. The NDRC’s Green Industry Guidance Catalogue adopts thresholds of technology and scale, which are conducive to eliminating outdated production capacity and projects in which governments do not encourage investment. Moody’s and Standard & Poor’s, the world’s leading credit rating agencies, use a scoring system that includes disclosure and other factors, in addition to green attributes.

Capital requirements include requirements for the use and management of green capital raised, referred to as capital requirements, including the field or project invested in, the time of investment, reinvestment requirements, whether it can be used to repay corporate debt, and other factors. CBS requires companies to invest in green assets with raised capital within two years. Currently, most green finance standards require that all, or a certain percentage, of green funds, raised be invested in approved green assets. For corporate green bonds issued under the NDRC’s Green Industry Guidance Catalogue, raised capital can be used to repay the existing liabilities of the enterprise. If the enterprise involves both green and non-green assets, it is difficult to supervise the use of funds. Reinvestment of the capital obtained by enterprises through green finance is often not restricted by green finance standards.

The essential factor that distinguishes green finance from traditional finance is incentive policy, which directly affects the rate of return of green financial products and non-green financial products. Incentive policies include pre-issuance incentives, in-issuance incentives and post-issuance incentives, including public sector interest discounts and tax relief policies, low-interest loans from policy-based financial institutions, and grants from multilateral institutions. The implementation of incentive policies is conducive to encouraging enterprises to increase investment in green assets. However, due to the large scale of assets involved in green finance, the cost of screening and auditing needs to be urgently reduced, and the difficulty of fiscal subsidies (such as interest discounts on green bonds) is significant. At present, the support policies of governments for green finance have not had a substantial impact on the income of green financial products worldwide. However, Singapore has adopted a policy of subsidising the assessment fees for green bond issues.

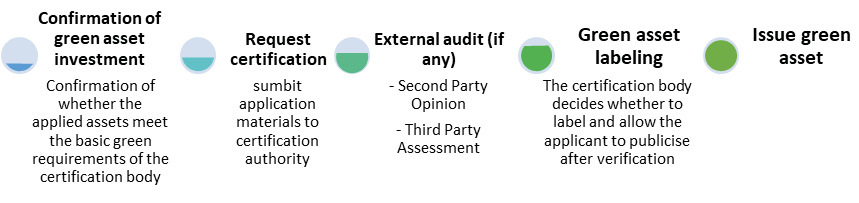

The certification of green financial products mainly refers to the evaluation and verification of the issuer’s internal processes, including screening of projects and assets, and tracking of projects, assets, internal processes, and expenditure of capital raised. The verification bodies adopt procedures to assess the readiness of the issuer and the compliance of the proposed bonds with the standards and employ general procedures (or lists) to assess the compliance of the proposed bonds with the pre-issuance requirements of the climate bond standard. Specifically, this includes the following steps: confirmation of green asset investment, certification application, second opinion or third-party review (if any), green asset labelling, and green asset issuance, as shown in Figure 11.1.

Fig. 11.1 The flow chart of the certification process of green financial products.

Confirmation of green asset investment refers to the preliminary review of whether the green financing application submitted (green credit, bonds, etc.) meets the definition and requirements of “green” classification for financial institutions. For the identified projects, the applicant must formally submit the certification application to the financial institution, including the project application and issuance qualification, capital use, monitoring and reporting methods. During this period, the financial institution may require the applicant to submit a second opinion or a third-party review. The largest second-party opinion service on green bonds is an assessment conducted by the Centre for International Climate and Environmental Research at the University of Oslo in Norway (CICERO), which has innovatively further subdivided approved green bonds into dark, medium and light green categories.

The second opinion is usually a general summary of a project carried out in the form of consultation; therefore, it is likely to lack credibility. Third-party review is a comprehensive assessment of the industry standard, capital use, capital management and monitoring and reporting of the product carried out by an independent institution hired by the issuer, according to the recognised green financial standards system. Whether it is a second opinion or a third-party verification, the existing market model is evaluated by the organisation hired by the issuer, and consequently, there will be potential conflicts of interest that are difficult to resolve.

The financial institution decides whether to label and issue the green asset after considering all of the application materials. In practice, the primary international assessment and certification standards are GBP and CBS, with China mainly adopting the Green Bond Supporting Project Catalogue released by the GFC.

Post-issuance monitoring is an essential but complicated part of the application of green finance standards. This is mainly due to the additional costs and strict monitoring system involved. Post-issueance monitoring will restrict the investment opportunities of financing institutions, which may reduce enterprises’ enthusiasm to issue green financial products. Post-issuance monitoring and tracking includes reporting the use of funds and proceeds, regularly disclosing the environmental and social impacts of the project, and post-release verification and assessment by third-party agencies. CBS strictly sets out the specific requirements and revocation of green bond issuance certification. The Equator Principles (EP4) requires that direct GHS emissions (Scope 1) and indirect GHGs from thermal or thermal use (Scope 2) must be publicly disclosed annually for projects with total annual CO2 emissions of more than 100,000 metric tons. The above standards, issued by mainstream international organisations, institutions and governments, are highly authoritative and influential. They provide a practical basis for developing green and climate financial products worldwide. However, there are certain differences in details, which reflect their different backgrounds and development demands.

11.2 What Are the Differences between Green Finance Standards?

Firstly, the definition of “green” differs. The definition of green varies from country to country due to the differences in stage, key concerns and operating institution of socio-economic development. The EU and institutions such as the CBI, the World Bank and the ADB have gradually focused on climate change mitigation and adaptation in recent years. On this basis, the Green Bond Principle also pays much attention to biodiversity conservation and other fields. China’s green finance standards had focused more on energy conservation, clean energy, pollution control, green infrastructure, clean transportation and ecological protection. A more noticeable difference is all parties’ attitude to the utilisation and upgrading of coal fossil energy. For example, the updating of old coal plants is generally judged as a “brown project” by international standards, which is not supported. However, in countries like India and China, the primary energy would rely on coal and clean coal or coal with carbon capture, utilisation and storage are usually considered as a green finance option.

Secondly, the scope and degree of refinement of the standards differ. From the perspective of range, the CBS, the GBP, the rating agency systems and the current green standards in China fail to include social benefits in the scope of screening and monitoring. The EP4, the World Bank and the ADB cover environmental, social and governance (ESG) indicators in their standards. The directory level and technical details of standards vary significantly. Both the Climate Bond Standard (CBS) and China’s Green Industry Guidance Catalogue subdivide the industry into three categories and specify the threshold of industry technology. GBP and the World Bank set the first-class directory, and the standard is relatively broad, with a lack of operability. The EP4 are mostly descriptive in principle and impose conceptual requirements on environmental risks. Other criteria should refer to the ADB’s basic theoretical specifications. China’s Green Bond Supporting Project Catalogue (2021 edition) and the Green Industry Guidance Catalogue (2021 edition) both stipulate specific projects and quantitative standards for loan use and separately explain the standards, which are of great guiding significance for the selection and evaluation of actual projects.

Thirdly, nature and implementation effectiveness differ. International standards are mostly voluntary in terms of adoption and compliance, and not mandatory. The green project or financial institution can obtain the labelling or certification after the voluntary application and verification by the standard-setting institution or third party. Moreover, after issuance, the reporting and disclosure requirements are relatively loose, and the role of the government is unclear. China’s green finance standards are issued by the government regulatory departments, which have executive force for the involved industries and participants. Besides, relevant departments are also responsible for examining, approving and supervising green investment and financing activities, thereby tangibly standardising and promoting the orderly development of green finance.

We note that with the increase of cross-border finance and international environmental cooperation, global green finance standards are gradually converging. Meanwhile, as global awareness of the environment and climate change issues deepens, more and more governments and organisations are realising that the current traditional green finance system is unable to effectively support the strong financial and institutional needs for countries to achieve their NDCs in the Paris Agreement and the UN 2030 Sustainable Development Goals (SDGs). In the discussion and practice of green finance, due to the particularity of its nature, purpose and methodology, the concept and development demands of “climate finance” have become increasingly prominent, and climate effect is often the most crucial consideration of the international green finance system.

11.3 Nuclear and Natural Gas as Green Investments?

In Feb 2022, the EU’s executive proposed to extend green finance criteria (EU Sustainable Finance Taxonomy) to natural gas-fired power and nuclear energy despite objections from NGOs, investors, a few member states, and members of its own expert group. Under the act approved by commissioners, private investment in natural gas-fired power generation will be classified as “transitional” if the plants use an increasing share of cleaner fuels like biogas or hydrogen.

The inclusion of gas-fired power, which emits mostly NOx and CO2 as well as methane via the natural gas supply chain, has drawn abundant criticisms. The decision was fiercely contested by EU member states. While Germany and some of Central and Eastern Europe had supported the inclusion of gas, nations like Sweden, the Netherlands, Denmark, Luxembourg and Austria had opposed it and called for parliament to reject the proposal or risk its being challenged in court.

The inclusion of nuclear power in the sustainable taxonomy also drew criticism from Germany, Spain and Belgium, countries which had committed to phasing out nuclear power after the 2011 Fukushima nuclear disaster. In fact, a new, large-scale nuclear power plant is too expensive to construct in Europe in the last decade. However, France is supporting the inclusion of nuclear power in the taxonomy, and generates 69% of its total power from nuclear.

The green taxonomy will provide a strong signal for private investment decisions in the EU and potentially create a template for other jurisdictions. Most countries have been cautious about including fossil fuel and nuclear power in a green or sustainable taxonomy. For example, China removed clean coal and natural gas from its green taxonomy in 2021. Even though coal and gas will have strong roles to play in China over the next decade, the taxonomy needs to be strategic about facilitating finance for long-term green growth.

11.4 Does Green Finance Product Deserve Public Financial Incentive?

The 2019 EU Green Bond Standard proposal encourages member states and financial institutions to link the standard directly with the future standards of the financial industry. Central banks will step up their participation to enhance the market’s acceptance and recognition of green finance. At the same time, it is advised that all member states implement preferential tax policies, including adopting an “accelerated depreciation method” for green assets and investment and improving the competitiveness of green assets. Similarly in China, the city of Huzhou in Zhejiang Province has taken the lead in formulating local standards for green finance. It is building a green finance reform and innovation pilot zone, promoting financial institutions to carry out green rating, labelling and information disclosure, as well as promoting the greening of the construction industry and the marketisation of environmental rights and interests, thereby comprehensively supporting the development of green finance.

It is noteworthy that the ability to generate additional green benefits should be the basis for policy support from governments and multilateral institutions. If a green investment and financing project is successfully carried out without being labelled as green (i.e., without additionality), the preferential policies provided by the government and multilateral institutions are likely to lead to wastage of resources and to squeeze the commercial investment and financing. It is a great pity that many green finance standard-setting organisations are aware of this problem (e.g., section 2.1 of the EU Green Bond), but do not encourage green bond issuers to disclose the additionality, which may mislead climate-friendly investors and policymakers. The authors reviewed the policy and marketing documents of the following green finance standards and found that none of them actually assessed and disclosed additionality (Table 11.1).

We reviewed seven major green bond standards in the world launched by International Capital Market Association (ICMA), Climate Bond Initiative (CBI), EU Technical Expert Group on Sustainable Finance (TEG), People’s Bank of China (PBOC), National Development and Reform Commission of China (NDRC), Moody, S&P, and Fitch. Only ICMA, CBI, and EU have been reported to discuss the additionality issue explicitly (as illustrated in Table 11.1 beneath). ICMA, in their working group research in 2018/2019, suggested “additionality in sustainable finance” as a discussion topic for consideration, while the EU Green Bond Standard report acknowledged the missing additionality issue in the current green bond market but argued there were other benefits in classifying bonds as green bonds, such as improving information transparency in green asset refinancing and developing policy debates in green finance. The discussion on additionality by CBI is rather vague and an “additionality assessment” is not needed for green bond certification in their frequently asked questions page on the carbon market. As shown in Table 11.1, none of these eight existing green bond standards have assessed or disclosed additionality issues.

Table 11.1 Review of whether “Additionality” is Discussed, Assessed and Disclosed in Major Green Bond Related Standards.

|

Discussed |

Assessed |

Disclosed |

|

|

ICAM Green Bond Principle |

Yes |

No |

No |

|

CBI”s Climate Bonds Standard |

Yes |

No |

No |

|

Proposal for EU Green Bond Standard, EU-GBS |

Yes |

No |

No |

|

PBOC Green Bond Guidance, China |

No |

No |

No |

|

NDRC Green Bond Guidance, China |

No |

No |

No |

|

Moody Green Bond Assessment |

No |

No |

No |

|

S&P Green Evaluations |

No |

No |

No |

|

Fitch Green Bond Rating |

No |

No |

No |

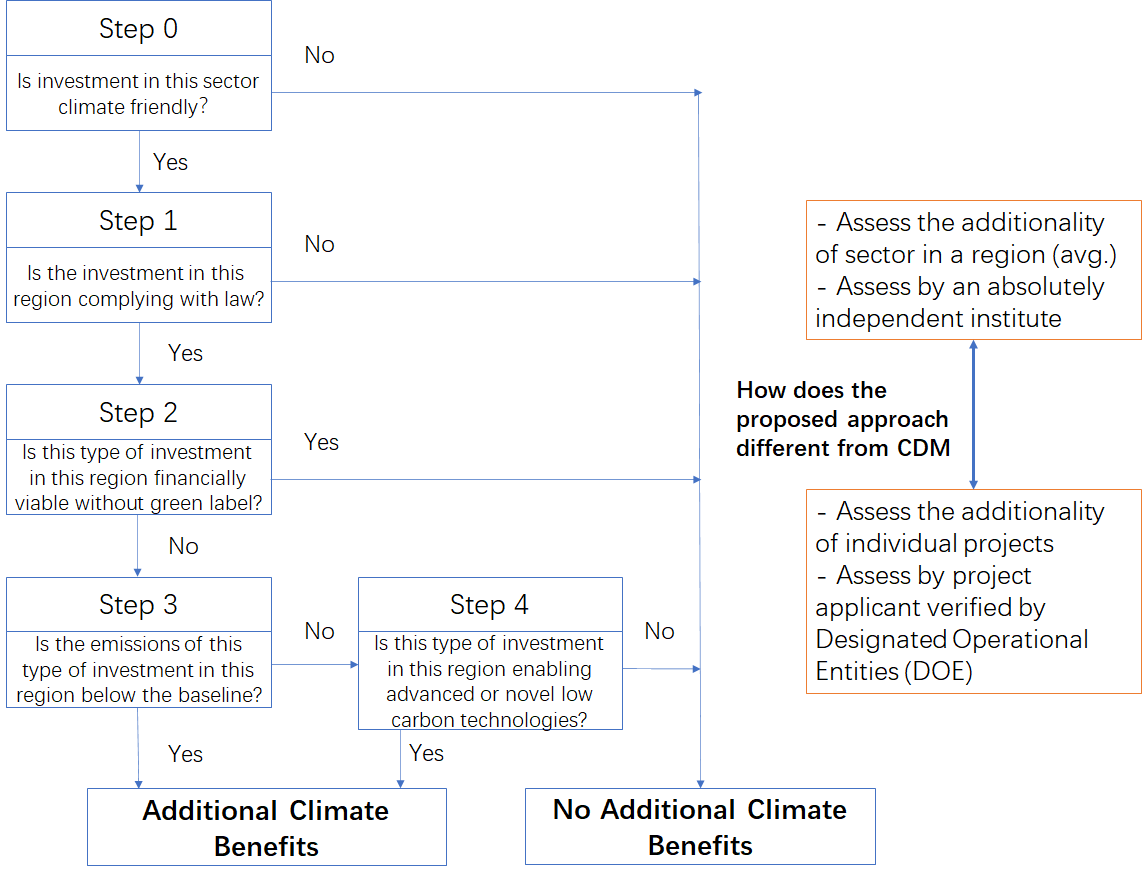

A future-proof green finance standard should provide more accurate disclosure requirement, i.e. investors of green bonds should notice that green bond investment does not create additional climate benefits and that the emission reduction of green assets is not attributed to such investment. Additional assessments of green finance should be introduced. We recommend a process illustrated in Figure 11.2 in the following text. Policymakers should meet the urgent need to create an investment environment that facilitates additional green assets, rather than simply making green statistics the baseline case. To generate additionality for a green asset, at least one of the following four investment environment scenarios needs to be created, in addition to a green additionality and financial additionality assessment.

1. Willingness of the issuers to accept a lower rate of return, i.e. environment- or climate-friendly firms would accept a lower required rate of return if the underlying project is certified with additionality. The condition may be possible if the additionality certificate generates significant reputational benefits to the issuer.

2. Climate-friendly concessional investors (either equity or debt investors) are willing to accept a lower required rate of return if the underlying project is certified with additionality. The climate finance commitments by MDBs shown in Figure 11.1 are likely meeting this condition. There are other climate-friendly family foundations or charities which may meet the condition as well.

3. Return increased: the return of the underlying project certified with additionality is increased to above the threshold level through either policy support or higher market price driven by additionality certification of the underlying asset.

4. Risk mitigation: the required rate of return (e.g. required IRR or discount rate) of the underlying project is decreased to below the project rate of return (e.g., IRR) through risk mitigation by additionality certification of the underlying asset.

Fig. 11.2 Proposed Approach for Assessing Climate Mitigation Additionality.

To maximise the efficiency of utilising climate funding and green finance, we make the following four recommendations:

- We recommend classifying new green finance products into two categories. Products without verified additionality could be defined as “green statistics financial products” and products with additionality could be defined as ‘green impact financial products’.

- We recommend that all existing green finance products, if possible, disclose whether additionality is assessed and, if assessed, disclose whether additionality is verified. This disclosure would avoid limited public resources and climate-friendly concessional investors mistakenly investing in projects without generating additional green or climate benefits.

- For potential green-impact financial products, further research is needed to understand how to maximise the effectiveness of grants, public finance, and concessional finance, to avoid generating significant windfall profit for projects with additionality.

- We recommend that green finance standards be updated with mandatory additionality disclosure. For standards currently at the development stage, such as the European Green Bond Standard, these should be more rigorous and transparent, and the additionality issue should be taken into account in the standard development process.

References

ADB (2015) Green Bond Framework. Manila: Asian Development Bank, https://www.adb.org/sites/default/files/adb-green-bonds-framework.pdf.

Buchner, B., A. Clarke, A. Falconer, R. Macquarie, C. Meattle, R. Tolentino, and C. Wetherbee (2019) Global Landscape of Climate Finance 2019. London: Climate Policy Initiative, https://climatepolicyinitiative.org/wp-content/uploads/2019/11/2019-Global-Landscape-of-Climate-Finance.pdf.

CBRC (now CBIRC) (2012) CBRC’s Notice on the Issuance of Green Credit Guidelines (CBRC (2012) No.4). https://www.cbirc.gov.cn/en/view/pages/ItemDetail.html?docId=68035&ite.

China Financial News (2018) Huzhou Released the First National Green Finance Local Standards (湖州发布全国首批绿色金融地方标准). Tonghuashun Finance, http://field.10jqka.com.cn/20180904/c606935597.shtml.

CICERO (2020) Shades of Green. https://www.cicero.green/our-approach.

Climate Bonds Initiative (2019) Climate Bonds Standard Version 3.0. CBI, https://www.climatebonds.net/files/files/climate-bonds-standard-v3-20191210.pdf.

Climate Bonds Standard (2019) https://www.climatebonds.net/standard/faqs.

de Coninck, H., A. Revi, M. Babiker, P. Bertoldi, M. Buckeridge, A. Cartwright, W. Dong, J. Ford, S. Fuss, J.-C. Hourcade, D. Ley, R. Mechler, P. Newman, A. Revokatova, S. Schultz, L. Steg, and T. Sugiyama (2018) “Strengthening and Implementing the Global Response”, in Global Warming of 1.5°C. An IPCC Special Report on the Impacts of Global Warming of 1.5°C above Pre-industrial Levels and Related Global Greenhouse Gas Emission Pathways, in the Context of Strengthening the Global Response to the Threat of Climate Change, Sustainable Development, and Efforts to Eradicate Poverty, ed. by V. Masson Delmotte, P. Zhai, H.-O. Pörtner, et al., IPCC, pp. 313–444, https://www.ipcc.ch/site/assets/uploads/sites/2/2019/06/SR15_Full_Report_High_Res.pdf.

Equator Principles (2020) The Equator Principles (EP4): A Financial Industry Benchmark for Determining, Assessing and Managing Environmental and Social Risk in Projects. Equator Principles, https://equator-principles.com/wp-content/uploads/2020/01/The-Equator-Principles-July-2020.pdf.

EU Technical Expert Group on Sustainable Finance (2019) Report on EU Green Bond Standard. EU, https://ec.europa.eu/info/publications/sustainable-finance-teg-green-bond-standard_en.

Fu, Y., Y. Wu and Y. Shi (2019) (2018) Practice Analysis of China’s Green Bond Appraisal and Certification (2018中国绿色债券评估认证实践分析), IIGF, http://www.tanjiaoyi.com/article-28329-1.html.

ICMA (2018) 2018/2019 Working Group Research. https://www.icmagroup.org/assets/documents/Regulatory/Green-Bonds/WG-Research-ToR-_-2018-2019-251018.pdf.

IRS (2019) How to Depreciate Property (Publication 946). https://www.irs.gov/publications/p946.

ISO (2021) Green and Sustainable Finance. Geneva: International Organization for Standardization, https://www.iso.org/files/live/sites/isoorg/files/store/en/PUB100458.pdf.

Jia, F., J. He, J. Yang et al. (2019) 2019 Climate Investment and Finance Case Study (2019气候投融资典型案例研究报告). Beijing: Publicity and Education Centre of the Ministry of Ecology and Environment.

Jiang, N. (2019) “Huzhou, Zhejiang Province, Has Embarked on a New Journey of Green Finance Reform and Innovation Pilot Zone Construction” (浙江省湖州市全面开启绿色金融改革创新试验区建设新征程), China Financial Information Network, http://greenfinance.xinhua08.com/a/20190308/1802593.shtml.

Moody’s Investors Service (2016) Green Bond Assessment (GBA). Moody’s, https://www.amwa.net/sites/default/files/GBA%20Methodology-final-30march2016.pdf.

NDRC (2015) Notice on the Issuance of Guidelines on the Issuance of Green Bonds (NDRC (2015) No. 3504). https://www.ndrc.gov.cn/xxgk/zcfb/tz/201601/t20160108_963561.html?code=&state=123.

Refinitiv (2022) “Sustainable Finance Continues Surge in 2021”, Refinitiv.com, 2 February, https://www.refinitiv.com/perspectives/market-insights/sustainable-finance-continues-surge-in-2021/.

S&P Global Ratings (2018) Green Evaluation: Time to Turn over a New Leaf?, S&P Global Ratings, https://www.spratings.com/documents/20184/1481001/Green+Evaluation/bbcd37ba-7b4f-4bf9-a980-d04aceeffa6b.

The World Bank (2017) Green Bond Process Implementation Guidelines, The World Bank, http://pubdocs.worldbank.org/en/217301525116707964/Green-Bond-Implementation-Guidelines.pdf.