9. The Investment Needs for REPowerEU

© 2022 Chapter Authors, CC BY-NC 4.0 https://doi.org/10.11647/OBP.0328.09

Introduction

On 18 May 2022, the European Commission presented REPowerEU (European Commission, 2022a, b), the concrete EU plan to reduce dependency on Russian fossil fuels. This plan details how to achieve the objectives laid out by the Commission in March (European Commission 2022c) that were endorsed by the heads of state and governments at Versailles (European Council, 2022).

The plan provides a clear identification of the required investment needs (including infrastructure bottlenecks) and policy actions on both the demand and supply sides. Reducing dependence on Russian fossil fuels will on the one hand require a faster reduction of our dependence on fossil fuels more broadly, and, on the other hand, a diversification of gas supplies. Both of these actions will require investments to boost energy efficiency gains, increase the share of renewables, address infrastructure bottlenecks, increase LNG imports and pipeline imports from non-Russian suppliers, and increase the levels of renewable hydrogen and bio-methane. In the immediate term, this requires a diversification of supply sources and a reduction in demand. In the longer term, this will call for the deployment of alternative sources of energy.

This article provides an estimate of the investment needs and additional costs of reducing our fossil fuel dependence on Russia to zero by 2027, with a specific focus on the use of natural gas. This analysis was instrumental in preparing the REPowerEU plan as presented by the Commission on the 18 May 2022. The decoupling of the EU and fossil fuel imports from Russia has already started and will pass through different stages, affecting both the demand and supply sides. Taking into account the above elements, this analysis indicates that reducing our dependence to zero (310 billion cubic metres, or bcm) would require €300bn1 cumulatively from now until 2030, in addition to the Fit for 55 proposals.2 By the end of 2027, this transition corresponds to approximately €210bn of investments (and 235 bcm). These REPowerEU investments correspond to about 5% of the total Fit for 55 investments until 2030, and are in addition to them. The Commission analysis estimates that with the Fit for 55 and REPowerEU measures combined, the EU can save €80bn on gas import expenditures, €12bn on oil import expenditures and €1.7bn on coal import expenditures per year.

Full implementation of our Fit for 55 proposals would lower our gas consumption by 30%, which is equivalent to 116 billion cubic meters (bcm), by 2030. Along with additional gas diversification and accelerated gas decarbonisation, frontloaded energy savings and electrification have the potential to jointly deliver at least the equivalent of the 155 bcm imports of Russian gas by 2027.

The REPowerEU plan proposed higher targets for renewables (-45%) and energy efficiency (-13%, final energy consumption) by 2030, thereby strengthening the Fit–for-55 package. This article explores how these higher renewables and energy efficiency levels contribute to the REPowerEU objectives.

Achieving the objectives of REPowerEU relies notably on scaling up renewable hydrogen and bio-methane and will make a crucial contribution to efforts to reduce EU dependence on Russian gas.3

The scaling up of the deployment of renewable hydrogen will reduce our dependence on natural gas, coal and oil imports from Russia, and will help to accelerate the EU energy transition. For this reason, the REPowerEU report of 8 March mentioned the Hydrogen Accelerator in relation to the ambition to use 20 million tons of renewable hydrogen in 2030 in the EU.

The proposed measures would not only facilitate an increase in the production of biogas, but would also boost its subsequent conversion into bio-methane, respecting strict environmental criteria agreed in the REDII. Recognising existing barriers to entry, the actions also target the facilitation of biomethane integration into the EU internal gas market. Further co-ordination of support for biogas and bio-methane at the EU, national and regional levels is needed if we collectively want to achieve the 35 bcm target. Challenges include improving infrastructure deployment, improving access to finance, and supporting research, development and innovation.

9.1 Drivers of Natural Gas Demand Reduction in REPowerEU

The March REPowerEU Communication states that the full implementation of the Fit for 55 proposals would lower our gas consumption by 30%, which is equivalent to 116 bcm, by 2030. The higher long-term gas and oil price paths will reduce natural gas demand further by about 40 bcm before 2030, whereas the implementation of the REPowerEU measures will complete the process with an additional almost 100 bcm reduction by 2030.

Together with additional gas diversification and renewable gases, frontloaded energy savings and electrification have the potential to jointly deliver at least the equivalent of the 155 bcm imports of Russian gas by 2027.

While there is currently an ongoing shift from gas to coal and oil, under the Fit for 55 proposal, demand for oil and coal is projected to decrease by 28% and 50% respectively between 2019 and 2030. Under REPowerEU, demand for coal is expected to decrease by 36% (by 2030 vs 2020). The demand for oil will be comparable in 2030 to the Fit for 55 projections (since the focus of this analysis is on gas). The reduction in the demand for coal suggests that we will fully replace Russian coal imports by 2027.

Three main drivers will change the energy system beyond the Fit for 55 proposals:

- The decoupling from Russian gas imports, leading to the need for alternative suppliers and entry points into the EU, alternative intra-EU pipeline routes and other infrastructure. Regarding natural gas, additional imports from alternative sources can reach Europe either by pipeline or in the form of LNG. In the short term, i.e. by using only existing infrastructure, an additional 10 bcm can be imported by pipeline and a further 50 bcm using existing LNG infrastructure.

- The REPowerEU plan further increases the ambition level beyond the Fit for 55 Package for gas alternatives (bio-methane, renewable hydrogen), deployment of renewables, and structural demand measures such as energy efficiency;

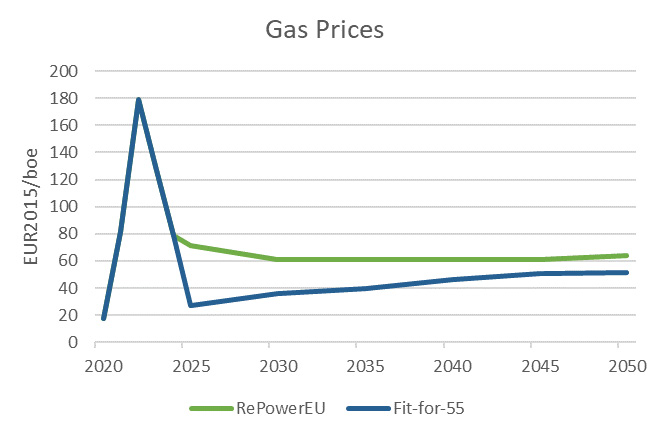

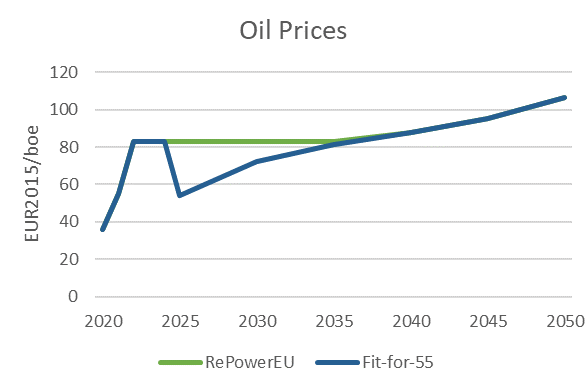

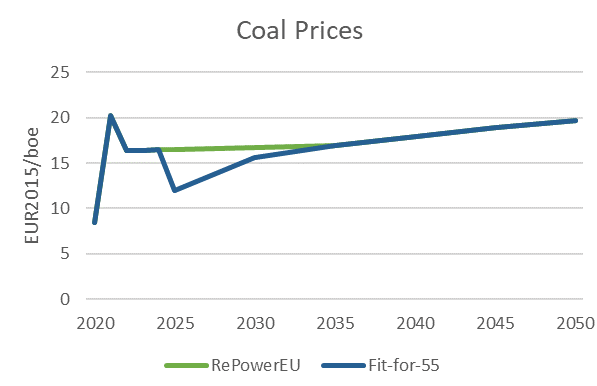

- Prices are expected to be persistently higher than the reference (but lower than the peak prices observed in 2021 and 2022). Experts expect that current events will temporarily fragment oil and coal markets resulting in higher prices, while these markets will rebalance in the medium term. The fuel price trajectories used in the REPowerEU and Fit for 55 scenarios are provided in Figure 9.1 in Annex A.

9.2. Investment Needs

Reduction of Gas Demand and Investments by Technology

Achieving the objectives of the REPowerEU communication to reduce the dependence of Russian fossil fuels will require significant investments to:

- Reduce our dependence on fossil fuels faster at the levels of homes, buildings, transport, industry and the power system by boosting energy efficiency gains, increasing the share of renewables and addressing infrastructure bottlenecks.

- Diversify gas supplies, via higher LNG imports and pipeline imports from non-Russian suppliers, and higher levels of bio-methane (domestically produced) and renewable hydrogen (domestically produced and imported).

Full implementation of our Fit for 55 proposals would lower our gas consumption by 30%, which is equivalent to 116 bcm, by 2030. Along with additional gas diversification and more renewable gases, frontloaded energy savings and electrification have the potential to jointly deliver at least the equivalent of the 155 bcm imports of Russian gas by 2027.

For the purpose of this analysis, fossil fuels considered are coal, oil and refined petroleum products (e.g. diesel) and, in particular, natural gas.

The analysis considered three dimensions for the menu of options:

- How fast can these measures be deployed?

- How cost-efficient are these measures (contribution to reducing the dependency, number of bcm saved in the case of gas)?

- How green? The measures should not lead to stranded assets and should be future-proof, as far as possible.

Several policy actions can be considered both from the supply and demand sides:

- In the short term

- Diversification of gas pipeline routes (including higher load factor of existing pipelines)

- Limited additional LNG under current infrastructure or floating storage regasification units (e.g. import terminals and pipeline network)

- Demand-side behavioural measures

- Energy efficiency investments (including heat pumps)

- Industry gas prioritisation (emergency measure)

- As a response to high prices, users switch to other fuels. With existing capacities, this can be achieved with relatively little additional investments (e.g., when coal and nuclear power plants increase operating hours)

- In the medium term:

- Further energy efficiency investments and innovation (including heat pumps, retrofitting and energy-efficient industrial processes)

- Development of bio-methane production and infrastructure

- Additional photovoltaic (PV), on-shore and off-shore wind deployment and energy system integration

- Additional investment in the power grid and storage

- Limited new LNG and gas pipeline infrastructure and adapting the existing gas networks to bio-methane and renewable hydrogen

- In the longer term

- Development of renewable hydrogen production and hydrogen infrastructure

The analysis looks at the investments needed to build a structurally new energy system that is independent from Russia as a fossil fuel producer. Taking into account the above elements, the up-front additional investment needs, complementing the Fit for 55 package, to reduce the dependence to zero would amount to €300bn from now until 2030 (or, approximately €210bn by the end of 2027).

Table 9.1 below focuses on a gradual decoupling from Russian gas and assesses the options for additional gas demand reduction and associated investment needs compared to the Fit for 55 scenario. It is based on comparing results of modelling scenarios of REPowerEU and implementation of the Fit for 55 package6 using the PRIMES model.7 The modelling implements the REPowerEU drivers as described in Section 2. More particularly, the investments listed in the table below notably cover the implementation of all the measures in the REPowerEU Communication and the specific needs for gradual gas decoupling from Russia by 2027, new LNG infrastructure and gas pipeline corridors, and production, transmission and demand sides of the transition outlined in the REPowerEU Communication including energy efficiency, renewables, heat pumps, renewable hydrogen including electrolysers, biomethane. Those investments do not cover the impacts of sanctions, oil savings, oil production or demand measures, curtailment of oil, natural gas or coal, nor investments in existing infrastructures related to the diversification of gas supply. As the focus of the analysis is on gas, Table 9.1 does not include transport, and investments in transport are similar in the REPowerEU and Fit for 55 projections.

Table 9.1 Potential measures and investments to reduce dependence on Russian gas via technology, in addition to the Fit for 55 package.

|

Timing |

Measure |

bcm (in 2030) |

€ bn invest-ments (2022-2030) |

Justification/ explanation of the bcm figure |

Eligibility under EU financial programmes |

|

Ff55 savings by 2030 |

Total of all Fit for 55 measures |

116 |

Fit for 55 modelling estimates 30% natural gas savings |

- |

|

|

Short-term prepared-ness |

Diversification (additional LNG using existing infrastructure) |

50 |

REPowerEU Communication COM(2022) 108 final |

- |

|

|

Diversification of pipeline imports using existing infrastructure |

10 |

- |

In 2030, long term contracts account for about 110 bcm (of which about 55 bcm are take-or-pay contracts) |

- |

|

|

Delayed phase-out and more operating hours for coal |

24 |

2 |

Using existing capacity. The investment refers to CAPEX. The fuel cost (coal) is not included (OPEX). The total expenditure of the switch from gas to coal is the sum of CAPEX and OPEX. |

- |

|

|

Abandoned phase-out nuclear plants |

7 |

-8 |

Recent political decisions in BE and FR |

- |

|

|

Fuel switch in the residential and service sectors |

9 |

Fuel switch driven by price changes |

|||

|

EU Save: Demand measures (behaviour) |

(10) |

- |

Measure 9 of the IEA plan on gas in the EU (gas saving counted under energy efficiency) |

- |

|

|

EU Save: Industry curtailment |

- |

- |

Emergency measure |

- |

|

|

Mid-term (until 2027) |

New LNG infrastructure and pipeline corridors |

- |

10 |

These infrastructure and pipelines facilitate the full effect of the diversification. Compared to average EU LNG imports of 7 bcm/month (in 2019–2021), the EU system could absorb an additional 3.8 bcm/month (45.6 bcm/year) of LNG if bottlenecks are removed. oe However, there are currently only 8 to 10 available Floating Storage Regassification Units LNG terminals in the world.9 |

Modernisation Fund,10 RRF,11 CEF,12 ERDF and CF, for projects on the 5th PCI list |

|

Additional investments in the power grid and storage |

- |

39 |

The storage is about 10bn. |

CEF, InvestEU,13 HE,14 ERDF,15 CF,16 JTF,17 RRF, ETF Funds18 |

|

|

Biomass in power generation |

1 |

2 |

In line with the sustainability criteria of the Renewable Energy Directive. |

HE, InvestEU, LIFE, ERDF, CF, JTF, RRF, ETS Funds, RES EU FM, EAFRD19 |

|

|

Energy Efficiency and Heat Pumps |

37 |

56 |

Including energy efficiency in buildings; Lower final electricity demand; |

HE,20 InvestEU, LIFE, ERDF, CF, JTF, RRF, ETS Funds |

|

|

PV |

- |

See Hydrogen |

In this scenario, all additional PV and wind power is used to produce the additional hydrogen. Alternatively, direct use of PV electricity to replace natural gas requires approximately €1.6bn of investment per bcm saved. |

HE, InvestEU, CEF,21 LIFE, ERDF, CF, JTF, RRF, ETS Funds, RES EU FM22 |

|

|

Onshore wind; Offshore wind |

- |

See Hydrogen |

Due to the long lead times and higher costs, in the short term, there is little additional deployment of offshore wind power. In this scenario, all additional PV and wind power is used to produce the additional hydrogen. Alternatively, direct use of wind electricity to replace natural gas requires approximately €1.6bn of investment per bcm saved. |

HE, InvestEU, CEF23 LIFE, ERDF, CF, JTF, RRF, ETS Funds, RES EU FM |

|

|

Sustainable bio-methane |

17 |

37 |

Increased use in households, industry and agriculture. The total (with Fit for 55) adds up to 35 bcm in 2030. |

||

|

Reduced use in industry |

12 |

41 |

Including electrification, energy efficiency, and fuel substitution (including hydrogen); Excluding the cost of production of hydrogen and biogas/bio-methane; Excluding refineries. |

HE, ETS Funds, InvestEU, ERDF, CF, RRF |

|

|

Long-term needs (by 2027 & beyond) |

Renewable hydrogen |

27 |

113 |

About 6.6 Mt is produced domestically and included in the Fit for 55 scenario. REPowerEU increases the domestic production by 3.4 Mt while 6 Mt of renewable hydrogen and approximately 4 Mt of ammonia are imported. Out of the approximately additional 10 Mt hydrogen, 8 Mt replace 27 bcm of gas, whereas the remaining 2 Mt replace oil (4 Mt) and coal (1.4 Mt of which 156 kt are from Russia29). Out of €113bn, €27bn corresponds to the direct production and distribution of hydrogen. €37bn covers the related investment for PV and €49bn is for related investment in wind electricity capacity. |

CEF, InvestEU, HE, ETS Funds, RRF, ERDF, CF, JTF30 |

|

Total |

310 |

300 |

Note: bcm figures in brackets are provided for information but not included in the total.

Infrastructure

The measures proposed for decoupling the energy supply from Russia constitute a significant change to the energy system in terms of quantities, prices, and directions of energy flows. As a result, the infrastructure needs for electricity, hydrogen and natural gas should also adapt. These infrastructure investments should solve the future needs in a coordinated manner, avoiding creating stranded assets as far as possible, and facilitating the long-term transition to a carbon-neutral economy.

Diversification of suppliers is essential for eliminating natural gas imports from Russia. In particular, it will be necessary to import sufficient additional natural gas from other pipeline suppliers and LNG ports. These new import routes and new intra-EU gas flows will require about €10bn of investment (e.g. LNG terminals, pipelines, reverse flows) by 2030, in order to guarantee a sufficient supply and a fluid distribution of natural gas across all member states.

Simultaneously, REPowerEU proposes an ambitious level of renewable hydrogen deployment, which also requires an acceleration of the development of renewable hydrogen infrastructure. These gas and hydrogen infrastructure investments should make use of synergies in order to be future-proof investments. Hydrogen networks should enable a pan-European integration of hydrogen supply and demand. This is closely related to the deployment of renewable energy (reaching a 45% share with REPowerEU), the location of electrolysers producing renewable hydrogen, and the form in which hydrogen is to be transported or imported (e.g. including ammonia).

The further increase and integration of renewable energy requires an efficient and adapted electricity network. REPowerEU increases and frontloads the renewable capacities compared to the Fit for 55 package, and the electricity network should adapt accordingly, including both offshore and onshore grids. By 2030, €39bn of additional investments in the power grid will be needed (including transmission, distribution and storage plants), compared to the Fit for 55 scenario, in line with the higher deployment of renewables.

9.3 Why Should the Potential for Natural Gas Reduction Be Higher than 155 bcm?

The combined effect of the Fit for 55 proposals—the measures announced in the March Communication, a higher price trajectory for natural gas, and the LNG and pipeline diversification—all have the potential to lead to a cumulative demand reduction of 310 bcm of natural gas by 2030 compared to 2020 (Table 9.1 Potential measures and investments to reduce dependence on Russian gas via technology, in addition to the Fit for 55 package.). By 2027, this will correspond to 235 bcm (including 60 bcm of diversification measures).31 REPowerEU aims to improve energy security in the EU, while respecting cost-efficiency and the decarbonisation pathway. Therefore, it is in the interest of the EU to have a broad range of options to allow for sufficient flexibility and to prepare for other unforeseen events. The objective should go beyond 155 bcm, which is the quantity of Russian natural gas imports in 2021.

- In previous years, the Russian imports have been significantly higher (e.g. 195 bcm in 201932). Further, domestic natural gas production continues to decrease by several bcm every year in the EU and its surroundings. Not all reductions in natural gas consumption will directly translate to fewer imports from Russia (e.g. in the Western part of the EU).

- Another uncertainty is the price trajectories of natural gas and the other fossil fuels. Higher gas prices than usual, as shown in the price trajectory (see Annex), will drive about 40 bcm out of the EU energy system by 2030 (e.g. by switching to coal). While lower gas prices are beneficial for the EU economy, the price signal to use less gas will evaporate, possibly compromising the decoupling from Russia, and putting the energy security of the EU at risk in the longer term.

- The REPowerEU measures and the Fit for 55 proposals rely heavily on a quick and ambitious deployment of fossil-free technologies. Various bottlenecks may delay this deployment, such as the dependence on rare-earth elements, supply chain constraints, skilled labour shortages, higher than average price inflation, financing, and the development of new production capacities and transport infrastructures (e.g. for renewable hydrogen).

Finally, the greater potential for gas reduction may allow the EU member states to roll back the temporary measures before 2027, including (i) measures to reduce the temperature in buildings by one degree (10 bcm), (ii) more operating hours and a delayed phase-out of coal power plants (24 bcm), and (iii) a delayed phase-out of nuclear plants (7 bcm).

9.4 Conclusion

The REPowerEU communication presents an ambitious but credible plan to reduce the EU’s dependence on Russian fossil fuels, identifying critical actions and specific investment needs.

Its implementation will depend on the ambition and ability to coordinate of member states in a very unstable context. In this sense, the EU would have to be ready to further develop its solidarity arrangements in case of supply disruptions and to coordinate demand reduction measures, complementing the current diversification efforts (particularly in the context of the EU energy platform). It would be advisable to strengthen solidarity requirements and tools so as to be better prepared in case emergencies arise.

With REPowerEU, the EU’s gas consumption will reduce at a faster pace, limiting the role of gas as a transitional fuel in the energy transition. REPowerEU solidly builds on the full implementation of the Fit for 55 package and proposes higher ambitions for renewables and energy efficiency. REPowerEU, combined with the Fit for 55 package, has the potential to reduce the EU’s natural gas use by up to 310 bcm by 2030.

Moving away from Russian fossil fuels will also require targeted investments for security of supply in gas and (very limited) oil infrastructure alongside large-scale investments in the electricity grid and an EU-wide hydrogen backbone. These investments are estimated to amount to €210bn by 2027 and require initiatives related to demand and supply, involving industry, buildings, infrastructure and the energy sector.

References

European Commission (2022a) REPower Plan, COM/2022/230 final, https://eur-lex.europa.eu/resource.html?uri=cellar:fc930f14-d7ae-11ec-a95f-01aa75ed71a1.0001.02/DOC_1&format=PDF.

European Commission (2022b) Commission Staff Working Document Implementing the REPower EU Action Plan: Investment Needs, Hydrogen Accelerator and Achieving the Bio-Methane Targets, SWD/2022/230 final, https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52022SC0230&from=EN.

European Commission (2022c) Joint European Action for More Affordable, Secure and Sustainable Energy, COM/2022/108 final, https://energy.ec.europa.eu/system/files/2022-03/Communication_Security_of_supply_and_affordable_energy_prices.pdf.

European Council (2022) Informal meetIng of the Heads of States or Government. The Versailles Declaration, 10 and 11 March 2022, https://www.consilium.europa.eu/en/press/press-releases/2022/03/11/the-versailles-declaration-10-11-03-2022.

Annex on Price Trajectories between 2020 and 2050 for Gas, Oil and Coal

Figure 9.1 shows the price trajectories between 2020 and 2050 for gas, oil and coal. Oil and coal prices are based on historical data for 2020–2021, combined with estimates of prices in 2022 and complemented by a linear interpolation to the long-term trajectory assumed in the EU Reference Scenario 2020 for the following years. The same approach is followed for gas prices, except that these are expected to remain higher than in the Fit for 55 scenario in the long run.

Fig. 9.1 Fuel price trajectories used for REPowerEU and Fit for 55 analysis.

1 All monetary values are in EUR 2022 with HICP index (March 2022) being 115.88 (compared to 2015).

2 The additional investments beyond the Fit for 55 proposals reflect both the impact of the REPowerEU measures and that of the higher (see Annex 1) fossil fuel price context. The analysis excludes:

- Transport

- The possibility to increase intra-EU sources of fossil fuels (e.g Groningen in the Netherlands)

- The investments and infrastructure needed outside of the EU (e.g. LNG terminals or tankers outside the EU removing bottlenecks to increase supply from Third Countries).

3 The European Commission (2022b) explores how the development of hydrogen can be accelerated and the bio-methane targets achieved. In particular, the Staff Working Document develops the Hydrogen Accelerator by identifying activities to support the implementation of these accelerated ambitions. It describes in which priority sectors the increased amount of renewable hydrogen can be used and what measures would enable this uptake, identifies possible activities and support for the rapid development of the required hydrogen infrastructure, including pipelines, storages and terminal facilities, and sets out how the EU could step up its international engagement and coordinate its actions to facilitate the import of 10 million tons of renewable hydrogen, while ensuring respect for the EU’s international trade obligations. Further, the Staff Working Document presents a number of possible actions to boost biomethane production to 35 bcm by 2030. The actions cover four key areas and could unlock the full biogas and bio-methane potential that exists across all EU member states.

4 Using the definition in RED III.

5 Including the use of e-fuels derived from hydrogen.

6 The additional investments beyond the Fit for 55 proposals reflect both the impact of the REPowerEU measures and that of the higher fossil fuels prices.

8 Investments for nuclear long-term operation are included in investments for other power technologies and infrastructure.

9 As an example, the Wilhelmshaven LNG Import Terminal, scheduled to enter service by 2023, once completed could deal with 10 bcm of additional gas per year. The cost of the project is around €672m.

10 Natural gas transmission (and distribution as well as gas-fired energy generation) are capped at a maximum of 30% of the overall Modernisation Fund allocation.

11 Recovery and Resilience Facility.

12 Connecting Europe Facility.

13 InvestEU Programme.

14 Horizon Europe.

15 European Regional Development Fund.

16 Cohesion Fund.

17 Just Transition Fund.

18 Refers to two funds established under the ETS Directive: the Innovation Fund and the Modernisation Fund. The Modernisation Fund is available to ten MS: Bulgaria, Croatia, Czech Republic, Estonia, Hungary, Latvia, Lithuania, Poland, Romania, and Slovakia.

19 European Agricultural Fund for Rural Development.

20 Horizon Europe.

21 Here, eligibility would be possible under the CEF-Energy cross-border RES envelope.

22 RES EU financing mechanism.

23 Here, eligibility would be possible under CEF-Energy cross-border RES envelope.

24 European Regional Development Fund.

25 Cohesion Fund.

26 Just Transition Fund.

27 Connecting Europe Facility.

28 Refers to two funds established under the ETS Directive: the Innovation Fund and the Modernisation Fund. The Modernisation Fund is available to ten MS: Bulgaria, Croatia, Czech Republic, Estonia, Hungary, Latvia, Lithuania, Poland, Romania, and Slovakia.

29 In 2020, 12% of coking coal consumed in the EU was imported from Russia.

30 Concerning the ERDF, Cohesion Fund, and JTF, the eligibility refers to RES hydrogen as “promoting renewable energy in accordance with Directive (EU) 2018/2001” according to Regulation (EU) 2021/1058 on the ERDF/CF.

31 The 60 bcm of diversification measures can be achieved entirely by 2027; the remainder is multiplied by 70% (to bring 2030 figures to 2027). Arithmetically, 235 = 60 + 70% * (310–60).

32 Total of 178 bcm of pipeline and 17 bcm LNG (ENTSOG).