12. Options for a Permanent EU Sovereign Fund: Meeting the Climate-Investment Challenge and Promoting Macroeconomic Stability

© 2023 P. Heimberger & A. Lichtenberger, CC BY-NC 4.0 https://doi.org/10.11647/OBP.0386.12

This chapter argues that a new, permanent EU fiscal capacity can contribute to meeting the green-transition challenges and providing countercyclical macroeconomic stabilisation. While the Recovery and Resilience Fund (RRF) is not large enough to address the current challenges, its introduction was an essential step forward in providing an operational blueprint for a permanent EU investment fund. The reform of EU fiscal rules is set to provide insufficient scope for the additional public climate investment required to meet the climate targets. Furthermore, the EU sovereignty fund proposed by the European Commission in the form of the Strategic Technologies for Europe Platform (STEP) adds little new money, focuses on green-tech subsidies instead of public investment, and falls short of providing a realistic vision of meeting public investment

12.1 Introduction

The introduction of the Recovery and Resilience Facility (RRF) in the context of Next Generation EU during the COVID-19 pandemic is a major common fiscal policy tool, representing a temporary large-scale public-spending initiative financed by issuing EU bonds. The RRF contributes to macroeconomic stabilisation while addressing structural policy goals related to climate and digitisation by way of public investment and reforms (Alcidi and Gros 2020; Bankowski et al. 2021). However, the grants channelled to individual member countries based on the issuance of EU bonds will only be available up to the year 2026. Debate over whether the RRF should remain a one-off initiative is in full swing (Allemand et al. 2023). This chapter contributes by discussing selected options for designing a new, additional EU sovereign fund.

12.2 Arguments for a New, Additional, EU Sovereign Fund

This section discusses three main reasons in favour of a new, additional, EU sovereign fund. First, the reform of EU fiscal rules is set to provide national governments with insufficient space for public investment, in particular for climate and energy. Second, the RRF is too small to meet the climate goals and will only provide funds up to the year 2026. Third, the European Union lacks a permanent sovereign fund to promote macroeconomic stabilisation during downswings.

The current institutional architecture of the European Economic and Monetary Union makes public investment for several Member States more difficult, especially when fiscal consolidation pressures increase during and after crises. A central problem with regard to the euro area’s institutional architecture is that interest rate spreads worsen the financing conditions of some Member States to a greater extent (De Grauwe and Ji 2022). This may inhibit their investments in the aftermath of a crisis and, thereby, hinder these economies to a greater extent in reaching the EU climate and energy goals.

In the aftermath of the COVID-19 crisis and the energy crisis, fiscal consolidation pressures tend to put downward pressure on public investment, especially in countries with higher public-debt ratios and higher interest burdens. In the absence of political countermeasures at the European level, there is a risk that public investment will fall short of what is needed. Public investment can be cut more easily than other government spending components when the pressure to pursue fiscal consolidation increases (Jacques 2021). In an environment of higher long-term interest rates, undertaking public-investment projects becomes more difficult.

Overall, the EU fiscal rules exhibit a high degree of complexity (Blanchard et al. 2021). The rules have failed to prevent rising public-debt ratios, even as austerity programmes put downward pressure on public investment. Overall, the design of the EU fiscal rulebook prior to the COVID-19 pandemic, when the rules were suspended, contributed to procyclical fiscal policy; thus, fiscal policy tended to amplify economic developments rather than to counteract them (Heimberger and Kapeller 2017).

In principle, reform of EU fiscal rules could increase the scope for public investment at the national level (Dullien et al. 2022). However, with the reform of EU fiscal rules proposed by the European Commission, individual EU Member States would only be able to submit plans for investments and reforms if they are consistent with sustainable government finances in the medium term based on debt-sustainability analysis (Heimberger 2023). Governments can extend fiscal consolidation paths by up to three years if the Commission’s technical analysis suggests that these investments are compatible with debt sustainability, if, that is, they are focused on reducing public debt ratios in the long run (European Commission 2023a). The general idea is that only selected public investment projects should be subject to reduced fiscal-consolidation pressures. However, broad exemptions of (climate) public investments in deficit and debt calculations (for example, Truger 2016) are not included.

The reform of EU fiscal rules will not provide sufficient scope for the needed climate and energy investments of the public sector; hence, national governments will find it hard to meet the investment requirements. A prior assessment report of the European Commission is key in providing numbers on essential climate investment dimensions (European Commission 2021). Existing studies estimate the need for additional annual investment for the green transition in a range between 1.75% and 6% of EU economic output per year, where about half of the funding should be provided by the public sector (Stöllinger 2023; Wildauer et al. 2020; Pollin 2020). We focus on a lower bound estimate and assume an equal division of the costs between the public and the private sector. This entails a need for additional annual public investment for climate and energy of at least 1% of the EU GDP (Heimberger and Lichtenberger 2023).

A large part of climate investments will have to be financed through public borrowing. On the one hand, the urgency of the climate crisis creates immediate pressure to act, which would overwhelm a private sector left to its own devices; on the other hand, future generations will benefit substantially from these investments and the associated net public-wealth creation.

The RRF was a major step towards a stronger common European investment policy. To mitigate pandemic-related economic impacts, European decision-makers agreed on Next Generation EU (NGEU) in summer 2020. The largest part of NGEU consists of the RRF, which has a total size of €723bn at 2022 prices. Of this, €385bn are available in the form of repayable loans and €338bn are grants that the individual Member States do not have to repay directly.

The RRF represents a large-scale temporary EU-wide investment initiative through the issuance of EU bonds. The EU Commission raises funds on financial markets on behalf of all Member States, and countries hit harder by the COVID-19 pandemic are eligible to receive more funds than those less affected. Each Member State is obliged to spend at least 37% of its RRF funds on climate investments. However, to achieve the EU climate target by 2030 (which calls for a 55% reduction in CO2 emissions compared to 1990 levels), would require an expansion of public investment on the order of ten times the green-investment share of the RRF, equivalent to about €460bn per year (Cornago and Springford 2021).

While the RRF allows for important investments, the instrument will only be in place for the period from 2021 to 2026; from 2024 onward, grants will be gradually phased out (see Figure 12.1). As national governments undertake RRF investments at the same time, there are positive cross-border economic effects, which are stronger for high-export countries such as Germany and Austria than for many of those EU countries that receive more grants directly (Picek 2020; Pfeiffer et al. 2023). Therefore, an isolated focus on the allocation of subsidies to individual EU Member States falls short because it neglects these positive spillover effects of investments.

Fig. 12.1 RRF Grants for the Whole EU, 2021–2026.

Source: European Commission.

While the RRF represents an innovative European investment model, the instrument is still not nearly large enough to sufficiently address the investment requirements due to climate change and the energy crisis, especially since the grants only flow until 2026 and already diminish from 2024 onwards. In the absence of a successor sovereign fund, public-investment problems in Member States must, therefore, be expected to increase particularly after the year 2026.

When it comes to coping with existing investment requirements that go far beyond the RRF, a joint EU investment offensive is more promising than national initiatives. Individual initiatives are limited by pre-existing climate-change impacts, which are more prevalent in some EU countries than others, and by cross-border emissions that continue to occur (Arnold et al. 2022). In addition, coordinated investments also show stronger positive network effects in the area of new technologies. Coordinating investment efforts and securing their financing to achieve common goals is also more efficiently achieved at the EU level than at the nation-state level. A joint credit-financed effort with cost-sharing between generations also reduces pressure for tax increases in the present.

Tackling the climate and energy crisis is also relevant to ensure the political unity and, thus, the geopolitically strong position of the EU in the future. Other large economic blocs currently pursue aggressive industrial policies concerning green technologies to secure competitiveness and higher global market shares. In particular, the USA passed the Inflation Reduction Act (IRA) in August 2022. Through additional public spending via tax-credits and subsidies for energy-security and climate-change investment in the region of $370bn over the next 10 years, the IRA is not only supposed to help achieve reductions in greenhouse-gas emissions. It also intends to secure America’s supremacy as the largest energy producer in the long term (Tucker and Malhotra 2022). The USA strives for international technology leadership, and additional climate spending is seen as an instrument to ensure that geopolitical ambitions can be met. In this context, the establishment of a sizeable EU investment fund could enhance the ability of the community of EU Member States to undertake strategic investment projects in climate and energy to mobilise private investments and promote the competitiveness in industries that are key for the future. This would enable European companies to properly compete with their peers in countries, such as the USA, where sovereign governments promote aggressive industrial policy based on sizeable additional public spending.

Furthermore, joint European decisions and initiatives require a distribution of economic burdens. Populations in EU countries are affected to different degrees by the consequences of the energy and climate crisis (Lenaerts et al. 2022). This makes policy implementations through coordination of nation-state initiatives increasingly difficult and requires joint EU solutions based on solidarity (Redeker and Jaeger 2022).

The European Economic and Monetary Union still lacks a permanent centralised fiscal capacity that contributes to cushioning macroeconomic shocks. When external shocks hit, such a facility would provide funding when national fiscal policies cannot respond adequately. Common monetary policy and domestic fiscal policy may be insufficient in responding to large common shocks; asymmetric impacts of a shock on different member countries may be impossible to address with domestic measures only (Misch and Rey 2022). As the next section will discuss, a European investment fund could provide stable funding for investments to avoid cuts during recessions, while a rainy-day fund could provide countercyclical funds, for example, via an unemployment re-insurance scheme.

12.3 Options for a New European Sovereign Fund

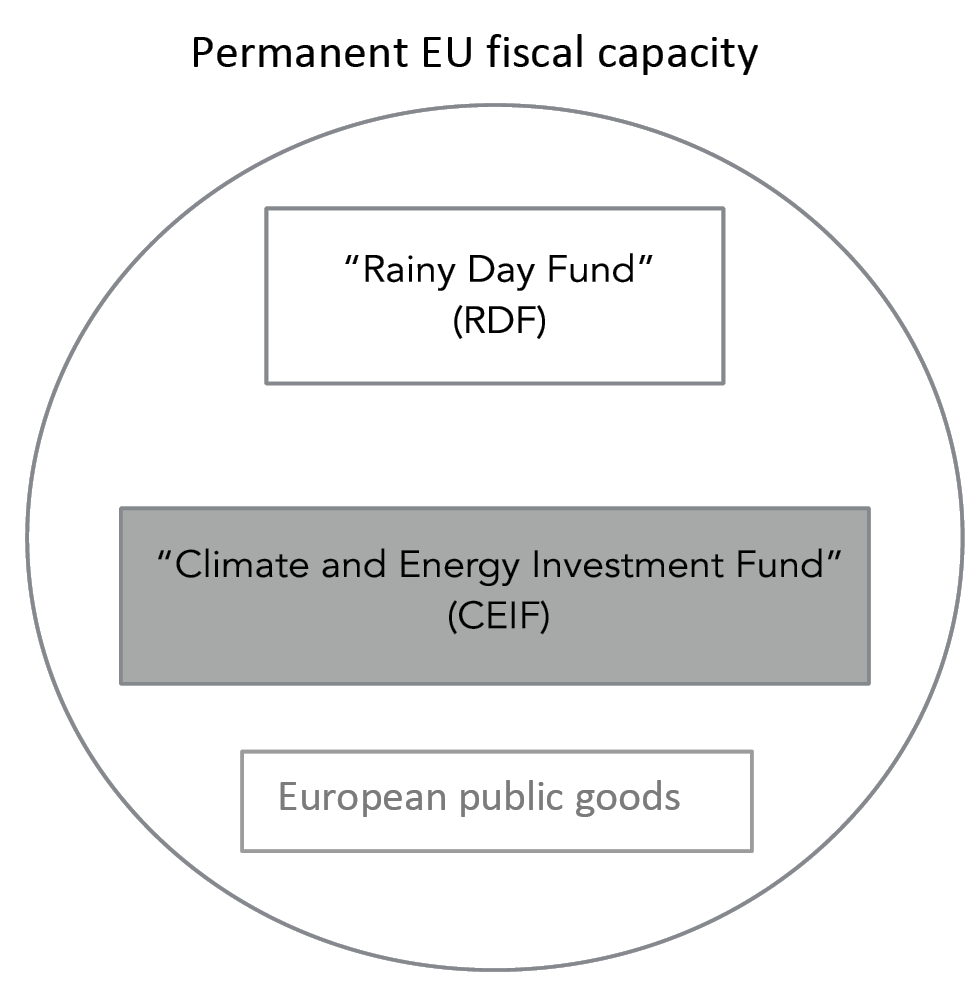

This section discusses three options for a new, additional, sovereign fund. First, a new, permanent investment fund based on the RRF model could provide funds so that individual member countries can make additional investments, in particular, related to climate and energy. Second, a new sovereign fund could focus on providing European public goods to emphasise the Pan-European dimension of investments. Third, a European ‘rainy-day fund’ could be introduced, which would finance expenditures during economic downturns in particularly affected countries by funds accumulated during boom periods. These options could be implemented individually or in combination.

12.3.1 A Permanent EU Investment Fund for Climate and Energy

RRF funds are disbursed gradually on the basis of evidence of investments and reforms implemented. In addition to meeting agreed milestones, investments and reforms must be consistent with long-term structural goals (such as climate neutrality). While using RRF money for additional investments can have a substantial stabilising effect on the economy (Picek 2020), the programme’s main purpose is to provide steady funding for investments and reforms over the period 2021–2026. The instrument is set up in a way that funds can flow regardless of swings in the business cycle.

A new, permanent EU Climate and Energy Investment Fund (CEIF), built on experience of the RRF, could support public investments that are tied to targets for achieving climate and energy goals (Heimberger and Lichtenberger 2023). The size of such a fund should allow for public investment of at least 1% of EU economic output annually to meet increased investment requirements even during periods of political and economic stress. An EU CEIF would help avoid procyclical cuts in public investment in the context of economic downswings, but it would not trigger transfers in reaction to negative shocks as in the case of a rainy-day fund.

An EU investment fund with green conditions would help achieve climate and energy targets. As funding criteria, the EU climate coefficient method, which already exists for green investments of the RRF funds, could be adapted (European Commission 2021). According to assumed contributions to the green transition, this method assigns weighting coefficients with regard to the eligibility of project expenditures. In the current situation, expenditures for projects to improve the energy efficiency of residential buildings or to expand solar-energy parks are weighted with a climate coefficient of 100%, while large companies’ energy-efficiency projects only receive a climate coefficient of 40% and their digitisation initiatives attract 0%. Applying an adapted method could allow for a consistent pursuit of climate and energy goals that is also not threatened by deteriorations in the budget outlook. While loans taken out by individual countries have a direct impact on the national public debt ratio, grants financed via EU bonds would not pass through to the public debt ratio. This would make it easier for EU Member States to comply with reformed EU fiscal rules, which could then be enforced more strictly even after their prospective reform (European Commission 2023a). A permanent EU CEIF would also have the advantage that national green investments accepted by the European Commission and European Council could draw on a common taxonomy to determine which investments should be classified as ‘green’.

In financing the permanent EU investment fund for climate and energy, the RRF could serve as a model. The European Commission would issue bonds on behalf of the EU to raise the investment funds in financial markets. Member states would not be individually liable for the EU bonds issued; the liability would remain with the EU, which would act in the financial markets backed by the guarantees of future contributions to the EU budget by EU Member States. The agreement on Next Generation EU provides for the establishment of new EU own resources that generate a revenue stream from which EU bonds can be serviced over a long period of time. A key advantage of repeating this financing method for the permanent EU investment fund would be that individual EU Member States’ contributions to the EU budget would not need to be increased. Options for new EU own resources—such as Emission Trading System (ETS)-based resources, Carbon Border Adjustment Mechanism (CBAM)-based resources, and taxation reforms for financial goods, corporations, aviation, top earners, and wealth owners—have been discussed by Schratzenstaller et al. (2022). Some researchers also argue that an EU-wide wealth tax to finance green investments could result in tax revenue in the dimension of the annual investment gap, namely 1.5% of EU GDP annually, with other models generating between 3% and even 11% in additional tax revenue (Kapeller et al. 2023). Another option is not to service the EU bonds (entirely) with EU own resources but to allow the build-up of an EU debt stock.

A recent report published by the ECB (Abraham et al. 2023) that seriously engaged with public-investment needs for climate and energy also concluded that an ‘EU Climate and Energy Security Fund providing €500bn by 2030 would be an effective and efficient option for addressing these climate and energy-related public investment needs’ (Abraham et al. 2023: 4).

Establishing a permanent common fiscal capacity at the EU level could be an effective, low-cost and politically feasible initiative. Collectively providing funds through an EU investment fund along the lines of the RRF would be a more attractive investment option for many EU countries than if they had to borrow individually on their own (Cornago and Springford 2021). An EU CEIF would make it easier for governments to undertake additional green investments beyond existing public investment quotas while complying with EU fiscal rules. A reasoning similar to the multi-factor disbursement decision rule applied to the RRF could also be used in the case of the CEIF. Any concrete funds-allocation rule would have to pass a political negotiation process. However, for illustration purposes, we show what such a stylised funds allocation could look like. A satisfactory and sufficient criterion should at least bear in mind each Member State’s needs for mitigation in the light of their respective financial abilities to cope with financing such a transition. Even though a lot more details could be considered, we here restrict ourselves to: (i) using the greenhouse-gas (GHG) emissions per capita for the variable that describes the need for change, since economies with very high GHG footprints require more structural change, (ii) accounting for the size of the country by including the current population count, and (iii) using the inverse of GDP per capita as a weight term that captures the degree to which financial support is needed. This implies that the share of the CEIF that should be attributed to each Member State i should be proportional to

CEIFi =  popi (

popi ( )–1= GHGi ()–1.

)–1= GHGi ()–1.

Figure 12.2 presents the results of such a distribution rule. The upper panel (A) shows the distribution of CEIF funds in absolute terms, which can be thought of as the share of the total annual investment funding volume of CEIF. If the CEIF allowed for investment of 1% of EU economic output per year (€146.5bn), large industrial countries like Poland (19.2% of the total investment funds), Germany (14.5%), Italy (9.6%), or Spain (8.4%) would receive the largest absolute grant amounts according to our allocation criteria. The lower panel (B) shows the amount of grants received by each country in relation to their own economic output. It can be seen that specifically Eastern Member States would receive relatively higher grants in comparison to their GDP, for example, Bulgaria (10.4%), Poland (4.9%), Romania (4.4%), and Latvia (3.4%), followed by Southern and Northern European countries.

The experience of debt-based financing at the EU level through the RRF can also be used to expand the thinking about financing options for an EU fiscal capacity. The introduction of a common European debt agency could circumvent the debt difficulties of individual countries, provide more funding space at lower funding costs, help to stabilise government-bond markets, and offer advantages in the issuance of assets considered particularly safe and liquid that, as such, would be in high demand (Saraceno et al. 2022). Institutional investors such as insurance companies and pension funds, show great demand for safe assets, the supply of which would be expanded by the increased and planned issuance of EU bonds over a longer period of time, thus contributing to the stability of financial markets (Alogoskoufis et al. 2020).

Fig. 12.2 Distribution of CEIF Funds in Absolute and in Relative Terms.

Note: Upper Panel (A) shows the percentage share of the CEIF that each EU Member State would receive based on absolute GHG emissions and the inverse of GDP per capita as disbursement criteria. Lower panel (B) shows the amount of the disbursement in relative terms based on the respective GDP (data based on 2021 values)

Source: Production-based GHG emissions in CO2 equivalents and population observations for 2021 adopted from Our World in Data; GDP at 2021 market prices and in € adopted from Eurostat.

12.3.2 European Public Goods: Focusing on the Pan-European Dimension

The boost from RRF funds is primarily attributed to national investment and reform projects, although the financing is based on issuing EU bonds. The option to implement a new long-term investment fund for climate and energy would also work by channelling funds to promote investment at the national level.

However, a new sovereign fund could also focus explicitly on genuinely European projects in the field of energy- and transport-system transformation to create common EU added value. EU public goods would benefit EU citizens across borders. For example, the improvement of transport and energy infrastructures is consistent with the shared necessity to decarbonize. Using the financing from an EU sovereign fund for European projects could contribute to overcoming the net-position thinking in EU Member States with regard to contributions to and transfers received from EU budgets (Bachtrögler-Unger et al. 2020).

Creel et al. (2020) propose investments in a European high-speed train system that could reduce CO2 emissions in the transport sector in the long term. In addition, in the area of energy and decarbonisation, they discuss the realisation of an integrated electricity grid for the transmission of 100% renewable energy and support for complementary battery and green-hydrogen projects. While a focus on Pan-European low-carbon transport and energy systems seems obvious in the context of pursuing ambitious climate and energy goals, other European projects could also be facilitated by an EU sovereign fund, such as security projects that enhance European autonomy in the context of the geopolitical struggle of the EU with China, Russia, and the USA.

12.3.3 A Rainy-Day Fund for Macroeconomic Stabilisation

The investment fund components discussed so far do not primarily focus on countercyclical stabilisation. Investments for climate and energy can be expected to have short-run and long-run impacts on the economy via fiscal multipliers (Fournier 2016). Furthermore, adaption investments for climate and energy are key to lessening future economic damage from climate change, thereby easing the pressure on national budgets in the long-run and making inaction economically unjustifiable (Zenios 2022; Steininger 2022). However, designing an investment fund with an emphasis on meeting long-run structural goals will not provide special countercyclical stabilisation properties during economic downswings.

For countercyclical purposes, a European ‘Rainy-Day Fund’ (RDF) could be introduced, which would finance expenditures during economic downturns in particularly affected countries by funds accumulated during boom periods (Lenarcic and Korhonen 2018; see Figure 12.3). A rainy-day fund would promote countercyclical macroeconomic stabilisation in future crises. For example, the IMF discusses a concept for the euro area wherein euro-area countries pay 0.35% of their economic output annually into a rainy-day fund to build up assets in good economic times that would be used to stabilise the region in the event of crises. The concept also includes mechanisms to avoid permanent fiscal transfers (Arnold et al. 2018). Rainy-day fund proposals include transfers triggered after negative shocks to economic activity (Furceri and Zdzienicka 2015), an investment-stabilization function that supports public investment especially during economic downturns (European Commission 2018), and unemployment re-insurance schemes (Dolls 2020).

Fig. 12.3 Components of a Permanent EU Fiscal Capacity.

Source: Author’s elaboration.

12.4 An EU Sovereignty Fund?

Prompted by USA green industrial-policy initiatives like the IRA, the EU is developing a policy response. On 20 June 2023, the European Commission announced the proposal of the ‘Strategic Technologies for Europe Platform (STEP)’ which shall take over the function of an EU sovereignty fund. The STEP is supposed to support the development of technologies in the field of digitalisation, decarbonisation, and biotech. Hence, its focus is on matching green-tech subsidies from the USA and China. Money flows will mostly be based on reshuffling existing funds. Instead of an injection of new cash, the policy draft reroutes money flows from existing budget positions with a €10bn top-up of Member States. Assuming multipliers between 1.3 and 10, the EC expects to mobilise a total volume of €160bn with €10bn of fresh money plus €50bn of redirected funds (see Table 12.1).

Table 12.1 EC Proposal for STEP

|

Program |

Fresh Money |

Adjustments |

Multiplier |

Headline number |

|

InvestEU |

3 |

7.5 (guaranteed) |

10 |

75 |

|

Horizon (EIC) |

0.5 |

2.13 (complemented) |

~ 5 |

13 |

|

Innovation Fund |

5 |

4* |

20 |

|

|

European Defense Fund |

1.5 |

1.33* |

2 |

|

|

Subtotal |

10 |

110 |

||

|

Cohesion fund reprioritizing** |

14 |

|||

|

Just Transition Fund** |

6 |

6 |

||

|

RRF Resources for InvestEU products |

30 |

|||

|

Subtotal |

50 |

|||

|

Total |

160 |

Note: * = Inferred; ** = Every 5% of programming towards STEP priorities leads to €18.9bn of [cohesion] resources made available, in addition to €6bn to be paid out from the Just Transition Fund

Source: Data from European Commission 2023b.

Besides assuming high multipliers and hardly adding any fresh money, the EU proposal of addressing a plethora of spending targets with €60bn, that is about 0.35% of current EU GDP, appears small. As outlined earlier, just to meet the EU climate goals an addition of at least 1% of EU GDP on an annual basis is considered necessary. Even assuming a crowding-in factor of 100% for all programmes, the total STEP spending volume would only amount to 0.7% of GDP.

12.5 Conclusions

This chapter has discussed selected options for a new, additional EU sovereign fund. A rainy-day fund for macroeconomic stabilisation in times of crisis could be combined with a long-term investment fund for climate and energy that provides public goods at the European and/or national level. However, the three options discussed in this chapter could also be implemented individually. A decision rule on the disbursement of funds could be based on multi-factor criteria as it was the case for the RRF. Similarly, the servicing of the debt for such a permanent sovereign fund could be ensured via new own EU resources or via allowing the build-up of an EU debt stock.

The debate on whether the EU needs a new, additional sovereign fund continues. The European Commission has tabled proposals for a European sovereignty fund. In their final proposal they reconcile their visions of a sovereign fund with the STEP. This programme, unfortunately, mostly reshuffles existing budgets and hardly adds new money; it does not even amount to half a percent of EU GPD in total. To keep alive at least the possibility of meeting the climate goals, European policymakers would need to do more.

References

Abraham, L., M. O’Connell, and I. Oleaga (2023). ‘The Legal and Institutional Feasibility of an EU Climate and Energy Security Fund’. ECB Occasional Paper, 313, https://doi.org/10.2139/ssrn.4403664

Alcidi, C., and D. Gros (2020). ‘Next Generation EU: A Large Common Response to the COVID-19 Crisis’, Intereconomics, 55(4): 202–03, https://doi.org/10.1007/s10272-020-0900-6

Allemand, F., J. Creel, F. Saraceno, S. Levasseur, and N. Leron (2023). ‘Making Next Generation EU a Permanent Tool. FEPS

Alogoskoufis, S., M. Giuzio, T. Kostka, A. Levels, L. Vivar, and M. Wedow (2020). ‘How Could a Common Safe Asset Contribute to Financial Stability and Financial Integration in the Banking Union?’ Financial Integration and Structure in the Euro Area, ECB-Publication, March

Arnold, N. G., B. Barkbu, H. E. Ture, H. Wang, and J. Yao (2018). ‘A Central Fiscal Stabilization Capacity for the Euro Area’. IMF Staff Discussion Note, 18/03, https://doi.org/10.5089/9781484348178.006

Arnold, N., R. Balakrishnan, B. Barkbu, H. Davoodi, A. Lagerborg, W. Lam, P. Medas, J. Otten, L. Rabier, C. Roehler, A. Shahmoradi, M. Spector, S. Weber, J. Zettelmeyer (2022). ‘Reforming the EU Fiscal Framework: Strengthening the Fiscal Rules and Institutions’. IMF Departmental Papers, 2022/014, https://doi.org/10.5089/9798400209888.087

Bachtrögler-Unger, J., M. Holzner, V. Kubekova, M. Schratzenstaller (2020). ‘Overcoming Net Position Thinking in EU Member States’, ÖGFE Policy Brief, July

Bankowsi, K., M. Ferdinandusse, S. Hauptmeier, P. Jacquinot, V. Valenta (2021). ‘The Macroeconomic Impact of the Next Generation EU Instrument on the Euro Area’, ECB Occasional Paper, 2021/255, https://doi.org/10.2139/ssrn.3797126

Cornago, E. and J. Springford (2021). ‘Why the EU’s Recovery Fund should be Permanent’. Policy Brief, July 14, Centre for European Reform (CER), https://www.cer.eu/publications/archive/policy-brief/2021/why-eus-recovery-fund

Creel, J., M. Holzner, F. Saraceno, A. Watt, J. Wittwer (2020). ‘How to Spend It: A Proposal for a European COVID-19 Recovery Programme’. WIIW Policy Report, 38

De Grauwe, P. And Y. Ji (2022). ‘The Fragility of the Eurozone: Has it Disappeared?’, Journal of International Money and Finance, 120, 102546, https://doi.org/10.1016/j.jimonfin.2021.102546

Dolls, M. (2020). ‘An Unemployment Re-Insurance Scheme for the Eurozone? Stabilizing and Redistributive Effects’. CESifo Working Paper, 8219, https://doi.org/10.2139/ssrn.3576297

Dullien, S., R. Repasi, C. Paety, A. Watt, S. Watzka (2022). ‘Between High Ambition and Pragmatism: Proposals for a Reform of Fiscal Rules without Treaty Change’, IMK Study, 77

European Commission (2018). ‘Proposal for a Regulation of the European Parliament and of the Council on the Establishment of a European Investment Stabilization Function’, COM(2018) 387 final

—— (2021). ‘Next Generation EU: Green Bond Framework’. Commission Staff Working Document, https://ec.europa.eu/info/strategy/eu-budget/eu-borrower-investor-relations/legal-texts_en#nextgenerationeu-green-bond-framework

—— (2023a). ‘Proposal for a Regulation of the European Parliament and of the Council on the Effective Coordination of Economic Policies and Multilateral Budgetary Surveillance and Repealing Council Regulation’, 1466/97, COM(2023) 240 final

—— (2023b). ‘EU Budget’. Press release, 20 June, https://ec.europa.eu/commission/presscorner/detail/en/ip_23_3364

Fournier, J. (2016). ‘The Positive Effect of Public Investment on Potential Growth’, OECD Economics Department Working Papers, 1347, OECD Publishing, Paris, https://doi.org/10.1787/15e400d4-en

Furceri, D. and A. Zdzienicka (2015). ‘The Euro Area Crisis: Need for a Supranational Fiscal Risk Sharing Mechanism?’. Open Economies Review, 26(4): 683–710, https://doi.org/10.1007/s11079-015-9347-y

Heimberger, P. and J. Kapeller (2017). ‘The Performativity of Potential Output: Pro-cyclicality and Path Dependency in Coordinating European Fiscal Policies’. Review of International Political Economy, 24(5), 904–28, https://doi.org/10.1080/09692290.2017.1363797

Heimberger, P. (2023). ‘Debt Sustainability Analysis as an Anchor in EU Fiscal Rules: An Assessment of the European Commission’s Reform Orientations’, In-Depth Analysis Requested by the ECON Committee of the European Parliament, March

—— and A Lichtenberger (2023). ‘RRF 2.0: A Permanent EU Investment Fund in the Context of the Energy Crisis, Climate Change and EU Fiscal Rules, WIIW Policy Notes and Reports, 63

Jacques, O. (2021). ‘Austerity and the Path of Least Resistance: How Fiscal Consolidations Crowd out Long-Term Investments’. Journal of European Public Policy, 28(4): 551–70, https://doi.org/10.1080/13501763.2020.1737957

Kapeller, J., S. Leitch, and R. Wildauer (2023). ‘Can a European Wealth Tax Close the Green Investment Gap?’. Ecological Economics, 209, 107849, https://doi.org/10.1016/j.ecolecon.2023.107849

Lenaerts, K., S. Tagliapietra, and G. Wolff (2022). ‘How Can the European Union Adapt to Climate Change while Avoiding a New Fault Line?’. Bruegel Policy Contribution, 11/2022, https://doi.org/10.1007/s10272-022-1071-4

Lenarcic, A. and K. Korhonen (2018). ‘A Case for a European Rainy Day Fund’. ESM Discussion Paper Series, 5, European Stability Mechanism (ESM)

Misch, F. and M. Rey (2022). ‘The Case for a Loan-Based Euro Area Stability Fund’. ESM Discussion Paper Series, 20

Picek, O. (2020). ‘Spillover Effects from Next Generation EU’. Intereconomics, 55: 325–31, https://doi.org/10.1007/s10272-020-0923-z

Pfeiffer, P., J. Vargaand, and J. in ’t Veld (2023). ‘Quantifying Spillovers of Coordinated Investment Stimulus in the EU’. Macroeconics Dynamics, 27(7): 1843–865, https://doi.org/10.1017/s1365100522000487

Redeker, N. and P. Jäger (2022). ‘New Needs, New Prices, Same Money: Why the EU Must Raise its Game to Combat the War’s Economic Fallout. Jacques Delors Centre Policy Brief, June

Saraceno, F., L. Gobbi, E. Belloni, C. A. Favero, and M. Amato (2022). ‘Creating a Safe Asset without Debt Mutualisation: The Opportunity of a European Debt Agency’. VoxEU, 22 April, https://cepr.org/voxeu/columns/creating-safe-asset-without-debt-mutualisation-opportunity-european-debt-agency

Schratzenstaller, M., D. Nerudova, V. Solilova, M. Holzner, P. Heimberger, N. Korpar, A. Maucorps, and B. Moshammer (2022). ‘New EU Own Resources: Possibilities and Limitations of Steering Effects and Sectoral Policy Co-Benefits’. Study Requested by the BUDG Committee of the European Parliament, March

Steininger, K. W. (2022). ‘Foreseeability of Economic Damages Related to Inadequate Climate Mitigation and Adaptation’, in Climate Change, Responsibility and Liability, June, pp. 93–102, https://doi.org/10.5771/9783748930990-93

Truger, A. (2016). ‘Implementing the Golden Rule for Public Investment in Europe: Safeguarding Public Investment and Supporting the Recovery’. Materialien zu Wirtschaft und Gesellschaft, 138

Tucker, T., and S. Malhotra (2022). ‘The Unprecedented Green Industrial Policy Wins in the Inflation Reduction Act’, Roosevelt Institute, 5 August, https://rooseveltinstitute.org/2022/08/05/unprecedented-green-industrial-policy-wins-in-the-inflation-reduction-act/

Zenios, S. (2022). ‘The Risks from Climate Change to Sovereign Debt’, Climatic Change, 172, 30, https://doi.org/10.1007/s10584-022-03373-4