9. Trends in Defence Spending in the European Union1

Alessandra Cepparulo2 and Paolo Pasimeni3

©2024 A. Cepparulo & P. Pasimeni, CC BY-NC 4.0 https://doi.org/10.11647/OBP.0434.10

After more than sixty years of peace, in 2022 Europe has faced a watershed moment in its security, which is leading to higher and more integrated defence spending in the European Union (EU). This article uses new sources of data to illustrate the evolution of defence spending in the EU and its composition. It also looks at the articulation of responsibilities for defence spending in a multi-level governance system, such as the EU. The institutional evolution of defence policy in the EU tries to build on a progressive convergence of foreign policy objectives and points towards some concentration of defence spending at the supra-national level. The key question for the future is to what extent this convergence will hold and to what extent it will be reflected in new provisions for defence in the common budget.

9.1 Introduction

Much of the economic literature relegates defence spending to the realm of strategic choices connected to security, threats, or arms races; in the post-Cold War years, the evolution of military spending has been shaped also by internal groups of interest. Additionally, defence spending, especially when considered in its various components, has implications for employment, investment, and the economic growth of a country. The empirical literature on the defence–growth nexus is not unanimous;4 little consensus exists on the relationship, as well as on its direction of causality and nature. Alptekin and Levine (2012) and Churchill and Yew (2018), in their meta-analysis of empirical studies found that positive economic impacts are more frequently reported in wealthy countries than in less developed ones. On a larger sample including developing countries, Yesilyurt and Yesilyurt (2019) find no significant effect, considering not only as dependent variable the share of military expenditure in GDP but also other functions of it (logarithms, differences, etc.). According to Santamaría et al. (2022), only about one in four articles, published between 1995 and 2019, support the existence of a positive relationship between military spending and growth, 16% support a negative relationship while nearly 38% are either heterogeneous or inconclusive. The findings are dependent on the time horizon and the methodology used. In particular, Dunne and Tian (2016), reviewing 168 studies, find that the horizon considered influences the results favouring a negative effect when using post-Cold War data.

According to the literature, favourable trends in investments and its components, such as equipment and R&T (research and technology) spending, can be deemed growth-enhancing. These economic implications deserve consideration in the current historical phase, when European countries are reassessing and increasing their defence spending, its quantity and composition, following years of steady decline.

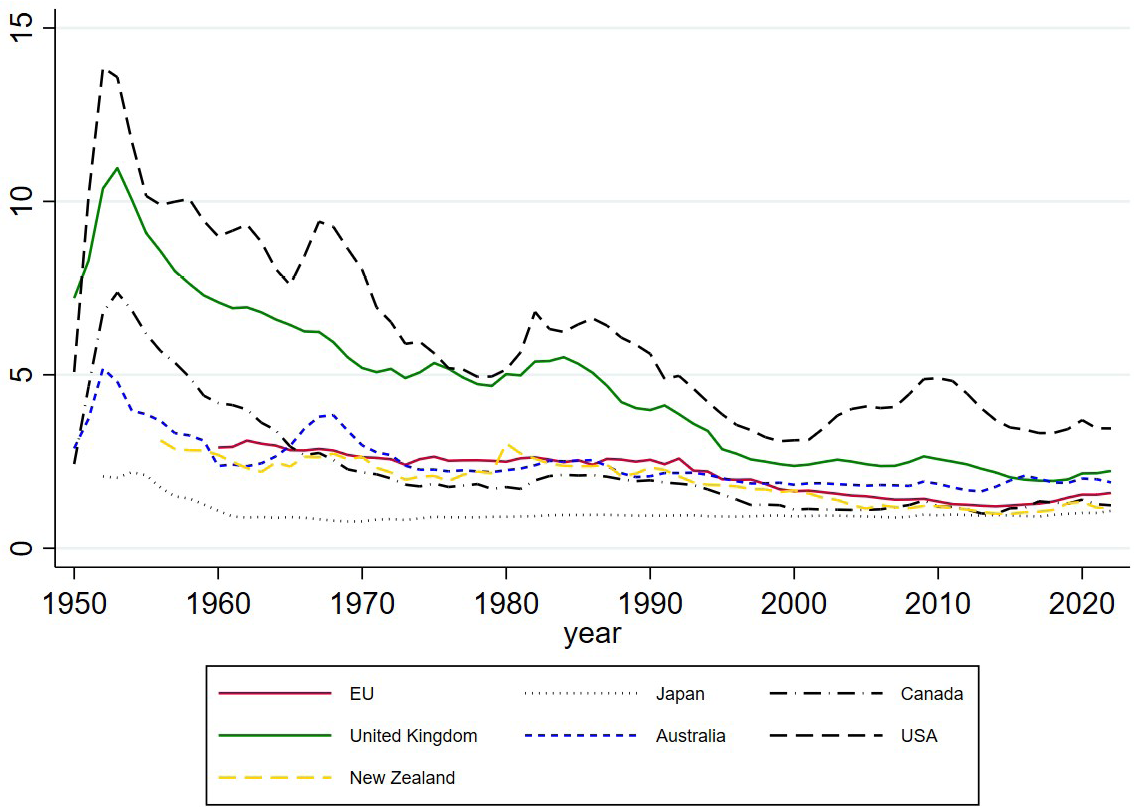

Several advanced countries have seen a significant decrease in defence spending over the past seventy years. In the United States (US), after the peaks connected to the Cold War period and the ‘war on terror’ in Iraq and Afghanistan, the share on military spending has decreased to about 4.5% GDP. In the European Union (EU) countries, as well as in New Zealand, and Japan, this decline has been less pronounced, also because the initial levels were considerably lower (Fig. 9.1). As a result of the Global Financial Crisis, a new downturn in military spending has taken place in the main advanced economies and, in particular, in certain EU countries (Bulgaria, Lithuania, Latvia, Greece, Slovakia, Slovenia, and Malta) where cuts have exceeded 20%.

Fig. 9.1 Defence spending (% of GDP): EU countries vs advanced economies. Source: SIPRI.

The invasion of Crimea by Russia and the NATO Readiness Action Plan, signed in 2014 to respond to instability and deteriorating security on the global front (NATO 2014), have reverted the trend. At that time, the US accounted for more than half of all transatlantic defence spending and NATO members agreed to reach a minimum spending of 2% of GDP in a decade. A further push in this direction, for the EU countries, came in 2017 when, as part of the Permanent Structured Cooperation (PESCO),5 they agreed to increase their defence budgets in real terms on a regular basis as one of their twenty common commitments. Finally, the invasion of Ukraine in 2022 has prompted a reappraisal of NATO and European countries’ defence spending with the view of bolstering their military strength.

The recent resurgence in defence spending raises multiple strategic, political and economic questions. The structure of the chapter is as follows. Section 2 discusses the economic, political, and institutional arguments about the attribution of defence spending responsibilities at different levels of government. Section 3 presents the institutional evolution of EU defence policy. Section 4 looks at the evolution and the composition of defence spending. The chapter ends with a conclusion.

9.2 Defence Spending in a Multi-Level Governance System

Given the nature of defence as a public good, a relevant question refers to the level of government best suited to finance it. The theory of fiscal federalism (Oates 1999, 2005) can inform this reflection. The traditional distinction of the key responsibilities of public finances highlights three main functions: allocation, redistribution, and macroeconomic stabilization (Musgrave, 1939). While the second and the third are usually performed more efficiently by the higher level of government (a federal or common budget), the function of allocation is often considered as one that is more effectively performed by lower levels of government, closer to citizens’ preferences.

There are, nevertheless, exceptions to this idea, notably related to the provision of public goods, a category to which defence belongs. Indeed, defence spending enjoys the non-rivalry and non-excludability features that characterize public goods. Hence, the only way to provide a sufficient level of defence is to entrust it to the highest level of government—be it central or federal—and fund it accordingly through its budget. However, an increasing number of activities related to defence policy—including policies related to common procurement, shared infrastructures, common arms export policies, and joint defence initiatives (Fuest and Pisani-Ferry 2019)—present non-rivalry and non-excludability features at the EU level, as they can ensure consistent and uniform security standards and equal protection and territorial integrity to all regions/states of the Union. Accordingly, to the extent that the Member States decide to transfer certain competences in the defence field to the EU level, this could be accompanied by and reflected in new provisions in the common budget.

A fundamental argument in favour of central EU spending on defence is to achieve economies of scale. Defence spending often requires significant upfront costs for acquiring and maintaining equipment, infrastructure, and technology. The recent report on the future of European competitiveness (Draghi 2024b: 166) argues that “complex next-generation defence systems in all strategic domains (air, land, space, maritime and cyber) will require massive research investment that exceeds the capacity of any Member State alone”. Considering the pace of technological innovation, EU Member States are unable individually to “finance, develop, produce and sustain the necessary defence capabilities and enabling infrastructure”. This may likely lead to inefficient and insufficient investment in defence, compared to other countries, thereby favouring technological dependence.

The central budget can pool resources, negotiate better contracts, and streamline procurement processes, leading to cost savings and efficiency gains. This approach is especially beneficial for smaller states that may not have the necessary resources to independently build and maintain robust defence capabilities. Fragmentation and duplication in spending are a source of inefficiency, dampening the positive effects of synergies and scale: in the EU, just 18% of all defence investments are undertaken collaboratively, according to the “Coordinated Annual Review on Defence” report (EDA 2022). In the case of R&T spending the percentage of collaboration is reduced by half. According to the European Commission (2022b), EU Member States frequently act in isolation rather than coordinating their military efforts, with the cost of this lack of collaboration ranging from €25 billion to €100 billion per year.

A further argument refers to defence externalities and spill-over effects. By centralizing defence spending, the EU could better account for interdependencies and externalities, ensuring a coordinated response. Moreover, investment in defence infrastructure, research and development (R&D), and defence-related industries can have spill-over effects on the economy, in the form of technology advancement and innovation. Mowery (2010) and Mazzucato (2013), based on the US experience, show how military R&D has been a crucial driver of technological innovation, with substantial spillover effects on the rest of the economy. However, Mowery (2010) notices how the extent and efficiency of these spillovers depend on factors such as openness, collaboration, and sustained investment. These benefits may extend beyond regional or national boundaries. These arguments are relevant from an economic point of view, in particular, because efficiency considerations seem to matter greatly when analysing the nexus with economic growth (Angelopoulos et al. 2008).

Finally, common defence spending can also be, in principle, a tool to better promote common strategic and foreign policy objectives. Centralizing defence expenditure would enable the EU to allocate resources strategically, respond to emerging threats, and project national power effectively on the international stage. These theoretical arguments support the assignment of some tasks of defence policy at the EU supranational layer. The current geopolitical situation would also suggest some form of pooled sovereignty, or at least enhanced European cooperation (Fuest and Pisani-Ferry 2019).

The EU, however, is not a federation, like other complete federal states; it is instead a union of sovereign countries in which political and budgetary responsibilities are delegated (with many limitations) by the national to the supranational level. The EU has evolved into “an environment of increased interconnectedness, but also heightened vulnerability, with rampant externalities and spillovers” (Buti and Papaconstantinou 2022: 1); for this reason, it is entrusted with some shared responsibilities across different policy areas and provides some public goods whose benefits are enjoyed at the EU level and that are also known as European Public Goods (EPG).

Due to the extent of the common military funding needs, the EU budget allocation alone is insufficient; both public and private resources are required. Public procurement can play an important role in reducing the defence market’s fragmentation, which is estimated to cost over €100 billion a year (Letta 2024). There have been discussions about the possible emission of defence Eurobonds or specialized credit lines for national defence spending, utilizing the European Stability Mechanism (ESM). The European Council (March 2024) agreed that the European Investment Bank could support the defence industry, while “core defence activities” remain excluded from the support. Such exclusion, as observed by the Draghi report (2024b) is also applied by other public and private banks limiting the possibility of the defence sector to fully benefit from EU financial instruments and private financing.

For the moment, in general, collaboration in defence spending is promoted only when it aligns with national goals or benefits the national industry, and this points to another fundamental criterion that has to be assessed when thinking of shifting decision and budgetary powers to the supranational level. Defence has typically been at the core of national interest because it has the ultimate task to provide security, it is an expression of sovereignty, and contributes to shaping a country’s role in the international community. To the extent that these objectives are shared among countries, these functions can be centralized, but the process is likely to be slow and delicate.

9.3 Institutional Developments in the EU Defence Policy

According to the current legal framework, defence policy is an intergovernmental competence, since the establishment of the EU Common Security and Defence Policy (CSDP) in 1999. The CSDP aims to provide the EU with the capability to effectively respond to international crises, contribute to international peace, and strengthen global security; it integrates both civilian and military tools.

In line with the Treaty limitations (TEU, Art. 41(2)), the EU budget can only cover the operating expenditure for civilian CSDP missions that contribute to maintaining regional and global security and stability, whereas the operations that have military or defence implications or the purchase of military equipment for third countries cannot be borne by the EU budget. The big legal question today refers to the nature of these “operations” that cannot be financed by the EU budget, and in particular whether Article 41(2) refers only to own operations of the Union or also to operations conducted by other entities (such as, for instance, Ukraine).

Since 2014, a growing perception of a threat following Russia’s annexation of Crimea and the war in eastern Ukraine has prompted European defence cooperation. The EU global strategy addressed five priorities: (1) the EU’s own security; (2) enhancing the resilience of the neighbourhood; (3) the use of an integrated approach when dealing with war and crisis; (4) support for stable regional orders around the world; and (5) effective global governance. This implied further developments for the Common Security and Defence Policy-CSDP, which is now distinguished by a coherent mechanism to enhance collaborative defence capability planning, development, procurement, and operation.

The EU Council established a specific mechanism called Athena (EU 2014), to finance common costs6 associated with some operations as well as the national contingents’ costs (such as lodging or fuel), back in 2004. In 2021, the Athena Mechanism and the African Peace Facility (which financially supported peace operations led by African states and regional bodies) were merged into the European Peace Facility (EPF), an off-budget account, funded by allocations from the Member States based on their gross national income. Since its creation, the EPF has been mobilized to support military assistance activities in a number of third countries, and it has played a key role in supporting Ukraine, as it allowed the reimbursement of EU member states for their donations of military equipment. The financial ceiling of the EPF was set at €5.7 billion (in current prices) for the years 2021–2027 when it was first established. It has, then, been increased to €8 billion in December 2022 and then to €12 billion in June 2023, to ensure that additional financial needs can be covered.

In December 2017, the European Council established a “framework and a structured process to gradually deepen defence cooperation” and create “a more coherent European capability landscape”, in order to enhance the collaboration between participating EU Member States. It also endorsed the modalities for establishing the Coordinated Annual Review on Defence (CARD) which provides Member States with a comprehensive overview of the European defence landscape (capability, research, and industrial aspects) in order to better identify opportunities for new collaborative initiatives. Finally, to reduce the European dependence on non-European actors in developing new and defence technologies, the Commission introduced in the Multiannual Financial Framework of the Union 2021–2027, the European Defence Fund (EDF).

The 2021–2027 EU Multiannual Financial Framework (MFF) has introduced, for the first time, a heading (number 5)7 dedicated to Security and Defence (European Commission 2021). Heading 5 is the smallest of all headings, accounting for 1.2% of the overall budget. In particular, the defence programmes cover 65% of the amount dedicated to this heading, the bulk of it going to the EDF (€7.29 billion in current prices) and military mobility (€1.75 billion in current prices).

The EDF co-finances Member States’ defence capability development costs (1/3 of the total) and provides funding for cooperative defence research initiatives at all levels of R&D (2/3). This fund combines two pre-existing programs funded by the 2014–2020 MFF as trial or preparation actions, namely the Preparatory Action on Defence Research (PADR) and the European Defence Industrial Development Programme (EDIDP),8 funded through the “Smart and Inclusive Growth” (heading 1).

Military mobility, instead, finances projects for dual-use transport infrastructure under the Connecting Europe Facility (CEF), mostly on the railway and roads infrastructures across Europe, in order to make the movement of the European armed forces faster and on a sufficient scale to respond to crises erupting at and beyond the EU’s external borders.

The Strategic Compass approved, in 2022, outlines the strategic direction and priorities for the EU on common defence policy until 2030, to enhance the EU’s capacity for autonomous action, and crisis management. The Compass overtly identifies Russia and China as threats or rivals and recognizes the geopolitical changes due to Russia’s invasion of Ukraine (Fiott 2023).

To address the EU’s most urgent and critical defence capability gaps, in 2023 the European Commission put forward a proposal for a regulation establishing the European Defence Industry Reinforcement through the common Procurement Act (EDIRPA), which would create a short-term joint defence procurement instrument and incentivize the EU Member States to procure defence products jointly, and the Act in Support of Ammunition Production (ASAP), a temporary instrument ensuring that the EU can ramp-up its production capacity. Both ASAP and EDIRPA are financed via the EU Budget, with an envelope respectively of €500 million and €300 million.

Finally, in March 2024, the European Commission (2024) has tabled a proposal for a new defence industrial strategy (EDIS), with the objective of stepping up its defence readiness. Based on an analysis of investment and capability gaps, it calls for more investment in defence, a more secure supply, and deepened partnership. This strategy sets three clear targets to be achieved by 2030: intra-EU defence trade to represent at least 35% of the value of the total EU defence market; at least 40% of defence equipment should be procured in a collaborative manner; and at least half (and 60% by 2035) of defence procurement should be sourced internally in the EU.

The rapid unfolding of new initiatives testifies of this new trend, started after Russia’s occupation of Crimea, and accelerated after its invasion of Ukraine. These events have prompted the European Commission to increase its ambition and expand its role to advance the integration process. However, the final outcome will be influenced by both supranational entrepreneurship and the collective political will of member states (Fiott 2023; Håkansson 2023).

9.4 Defence Spending in the EU Countries

9.4.1 Methodological Aspects

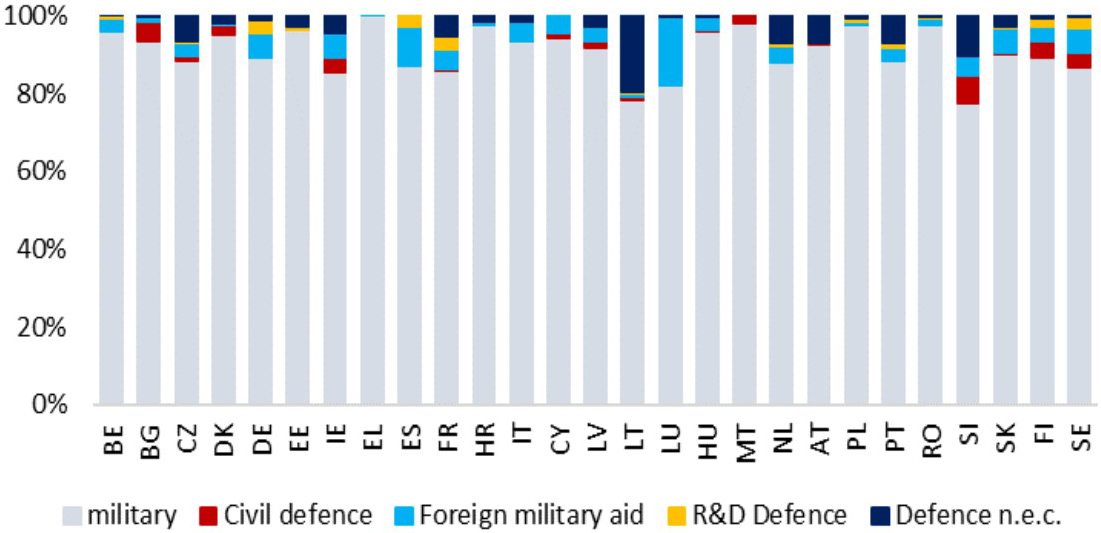

This section presents an examination of the evolution and composition of defence spending in the EU countries, drawing on multiple data sources: (i) the Stockholm International Peace Research Institute (SIPRI) Military Expenditure Database,9 which provides continuous time series data for 155 states from 1949 to 2022; (ii) the European Defence Agency,10 which provides data on defence spending and its composition since 2005 for EU Member States;11 (iii) NATO defence database that provides the decomposition of defence expenditure by main categories for 24 EU countries;12 (iv) EU countries Stability and Convergence Programs, that provide medium-term projections of defence spending, and, finally; and (v) the EU budget. Given that military spending accounts for around 90% of EU defence budgets (Fig. 9.2) referring to military spending or defence data guarantees consistency.

Fig. 9.2 Defence expenditure by function: average (2012–2022). Source: Eurostat.

9.4.2. Recent Trends

In 2022, defence spending in the EU hit a record of €240 billion, a 6% rise over 2021 in constant terms (EDA 2023), keeping a trend of consecutive increases for the eighth year, following the invasion of Crimea. Almost all EU countries have increased military spending in the past decade. Four categories of countries can be distinguished based on the most recent data (Fig. 9.3a). The first group comprises countries that are not NATO members (such as Ireland, Austria, and Malta) or are small countries (Luxembourg): they spend less than 1.1% of their GDP.

Instead, the bulk of European countries fall into the second category, with expenditures ranging from 1.1 to 2% of GDP, with Finland (1.94%) and France (1.88%) spending the most in this cluster. The third and fourth groupings include the Baltic Republics, Poland, and Greece, who spend more than 2% in accordance with NATO commitments and more than the EU average of 1.5%. Greece is the only country with a level of expenditure higher that 3%, up to roughly 4% of GDP, something probably due to the long-standing tensions at its borders with Turkey. According to NATO forecasts, the number of countries spending more than 2% of GDP should have doubled in 2023. Poland is predicted to have the greatest increases, with a growth of more than 60%, followed by Finland and Romania, where spending is expected to rise by more than 40%.

Fig. 9.3 Defence spending. (a) EU countries (% GDP) (above); (b) EU growth: 2000–2022 (below). Source: EDA Defence data 2022, NATO and SIPRI database. Note: EU countries are represented by their two-letter country codes. EU figures correspond to the average among EU countries. NATO database doesn’t include the data for Ireland, Malta, Austria, Cyprus, and Sweden.

EU Member States are not only guided by the NATO commitments but, as part of PESCO, they agreed in 2017 to increase defence budgets in real terms on a regular basis as one of their twenty common commitments. Half of the countries met their commitment with a consistent increase across the past four years. Only one country (Croatia) has shown positive growth in two years. Malta13 is not among the PESCO participating members and did not commit to any specific target.

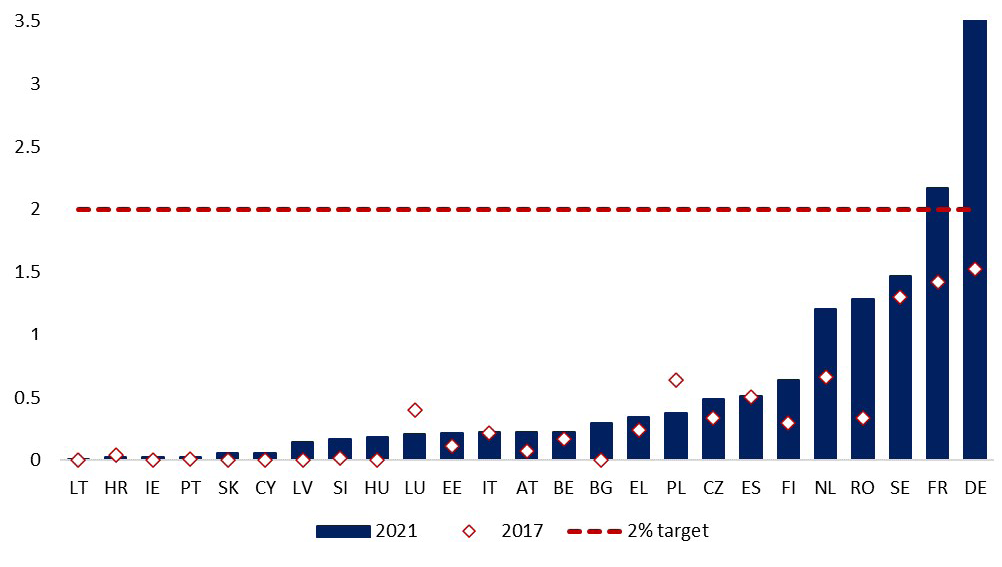

The Russian invasion of Ukraine, in February 2022, has drastically shaken the geopolitical equilibria; as a consequence, further increases in defence spending are expected. According to the 2023 Stability and Convergence Programmes,14 at least nine European countries plan to increase defence spending by 2026 (Fig. 9.4). Czechia (by 1% of GDP) and Finland15 (by 0.7% GDP) are on top of this list. The Netherlands, Estonia, and Spain intend to increase defence spending by 0.5, 0.4, and 0.3 percentage points of GDP, respectively. Four other countries (Slovakia, Latvia, Luxembourg, and Bulgaria) expect an increase of less than 0.2% of GDP by 2026. The national programmes of eight other countries16 mention the future budgetary impact of defence spending although no quantitative information is provided. Only the programmes of the remaining eight countries have no mention of defence spending.17

More generally, the Council of the EU confirmed future higher spending commitments in the Strategic Compass (Council of the EU, 7371/22), in which Member States committed to increasing defence expenditures to close critical military and civilian capability gaps and strengthen the European Defence Technological and Industrial Base strategy, inaugurated in 2007 to better coordinate defence policies and the related industrial activities.

Fig. 9.4 Defence expenditure planned in selected EU countries for 2026 (% of GDP). Source: 2023 Stability and Convergence Programmes.

9.4.3 The Composition of Defence Spending

The composition of defence spending has some relevance, not only in terms of effectiveness of the defence capabilities of a country, but also in terms of economic effects. Some studies argue that spending on non-equipment can be associated with a potential crowding-out effect of the private sector, while the equipment budget, linked to procurement and R&D, can generate a crowding-in effect.

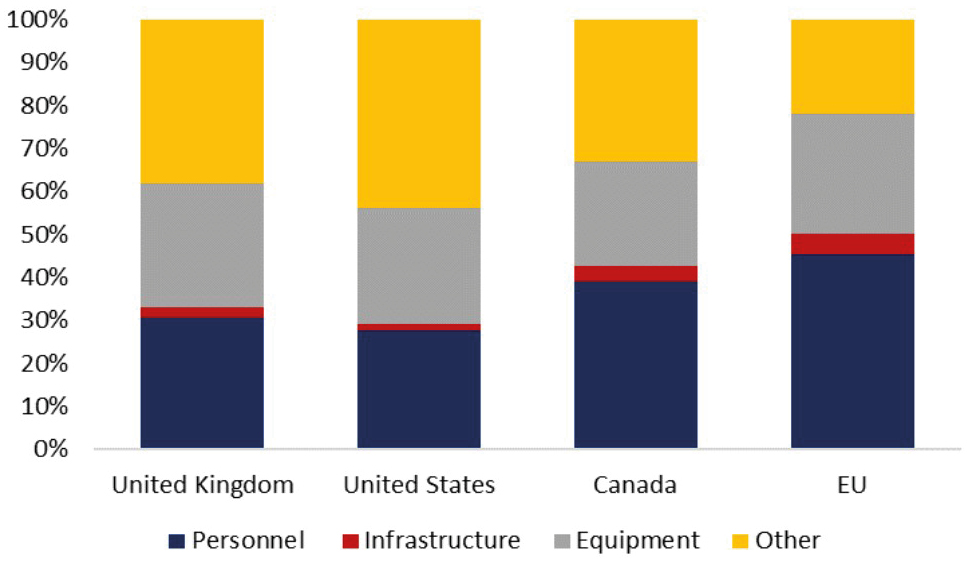

From a functional perspective, there are four components of defence spending: equipment,18 personnel,19 infrastructure,20 and other operating spending.21 Using data from NATO and the EU, we observe that personnel spending absorbs the majority of resources dedicated to the defence function, in all advanced countries (Fig. 9.5a). While it accounts for roughly one-third of total spending in the UK and the US, it represents slightly less of half of total spending for the EU countries and Canada.

Historically, the EU has spent the most in personnel spending. This category accounts for around 46% of defence expenditure in 2023, which is 64% more than the amount spent by the country that spends the least (US). On average over the period 2010–2022 this item accounted for 56.5% of GDP. Although the share of personnel spending has been declining since 2014 (Fig. 9.5b), the EU countries will still have the highest level, with Cyprus (74% of total expenditure) and Ireland (81% of total expenditure) topping the list (Fig. 9.5c).

These figures seem to confirm the theory of burden shifting inside the NATO alliance (Becker 2017; 2021). In case of peer pressure or fiscal pressure, reallocation of resources within the defence budget are a somehow hidden way of burden-shifting. In order not to lose the benefits of being part of an alliance, countries can favour, within the defence budget, those expenditure categories with more direct domestic benefits. As a result, personnel would be the most appealing short-term choice, given the immediate gains in terms of employment stimulus. This situation is all the more probable in times of peace, when there is no specific threat that pushes towards a strategic direction. Becker (2021) finds evidence that countries facing unemployment tend to reduce defence spending and divert resources from acquiring capability-enhancing equipment. Instead, they prioritize personnel spending as a stabilizing measure.

Fig. 9.5 Decomposing the defence spending (% of total defence expenditure). (a) Advanced economies in 2023 (above); (b) EU: 2010–2023 (middle); (c) EU countries in 2023 (below). Source: NATO and EDA defence data 2022. Note: EU figures correspond to the average among EU countries.

In contrast to other advanced economies, EU members spent the most on infrastructure in 2022 (about 4%) (Figs 9.5a and 5b). On average, this category in the EU accounts for around twice as much as in the US. All advanced economies have boosted expenditure in this category since last year. The US and the UK spend approximately one-third of their defence budgets on equipment; Canada slightly less than that. The amount committed to this item by the EU countries is increasing (Fig. 9.5b), and in 2023 it appears more in line with the level of expenditure of other advanced economies (27.8% of GDP). Three of the non-NATO EU countries (Austria, Ireland, and Malta) spend less than 20%in this category. On the contrary, equipment expenditure accounts for more than 40% of total defence expenditure in Luxembourg, Poland, and Hungary in 2023. Given that there is no indication that this category of spending has a detrimental influence on growth among EU and NATO members, the expansion in this category in the majority of the countries can be beneficial in light of the need to increase investments spending and fill strategic capability gaps.

Equipment category corresponds to investment in defence according to the EDA definition, which can be further divided into equipment purchases, and R&D. The equipment component has the largest share of defence investment and accounts for over 90% on average. Defence investment is subject to a target fixed by NATO (2014) and confirmed by the European Council (2017),22 asking for a “medium-term increase in defence investment expenditure to 20% of total defence spending (collective benchmark)”. While at the European level the benchmark is collective, already in 2006, NATO Defence Ministers committed to devote 20% of the defence budget to investment.

Data at the disaggregated level, for 2022, reveal that twenty EU Member States met the 20% target for defence expenditure dedicated to investment (Fig. 9.6a), which marks a significant improvement over the previous five years when only eight Member States achieved that aim. Luxembourg has the largest investment quota (53.5%), while Austria spends the least (9.5%). The aim has been met collectively since 2019. It now accounts for 24.2% of the twenty-seven countries’ overall defence expenditure (EDA 2023), which, however, is 0.2% lower than the previous year (24.4%) (Fig. 9.6b).

Looking at the breakdown of defence investments, apart from a positive trend in the equipment component23 since 2014, we see a negative tendency for R&D until 2017, when it climbed by 26.3% and stabilized at around 17% of total defence investment (Fig. 9.6b). Further rises are projected in the future, at least for one of his two components: defence expenditure on R&T corresponding to the expenditure for basic research, applied research and technology demonstration for defence purposes. This component of the R&D spending is expected to reach 2% of total defence expenditure as a collective benchmark by all the Member States (European Council 2017). Collectively the percentage spent on this item is equal to 1.5% in 2022 with an improvement of 0.6% compared to 2017 (EDA 2023). In 2021, at country level, three quarters of EU Member States have increased their spending on R&T since 2017 (Fig. 9.7). Only two countries (Germany and France) had reached the 2% target in 2021 individually.

Fig. 9.6 Defence investments. (a) EU countries 2022 (% of total defence expenditure) (above); (b) EU composition evolution (% of defence investments) (below). Source: own elaborations on EDA defence data 2022. Note: Malta did not commit to any specific target as it is not among the PESCO participating members and not a NATO ally. The data for Denmark comes from the NATO database and reports the percentage spent on equipment.

In terms of defence spending composition and its impact on economic growth, the outlook of additional increases in R&D is quite positive, thanks to the development of new technology (i.e. radar, jet engines, nuclear energy), favouring commercial spin-offs (Pivetti 1992; Dunne et al. 2005). Indeed, due to high‐risk environmental and public‐good characteristics, certain research projects are unlikely to be carried out by the private sector (Benoit 1978). Thus, there is evidence of crowding-in effects of public defence-related R&D investment on private R&D. Increases in government-funded R&D for an industry or a firm result in significant increases in private sector R&D in that industry or firm, with evidence of international spillovers in the same industry in other countries and positive effects on overall productivity growth (Moretti et al. 2023).

Fig. 9.7 Defence R&T expenditure (202124 vs 2017, % of total defence expenditure). Source: EDA defence data 2022. Note: the data for Latvia and Slovakia are not available for 2017. No data are available for Denmark. Malta is not among the PESCO participating members and so they did not commit to any specific target.

This is consistent with Antolin-Diaz and Surico (2022), who find that in the US the fiscal multiplier for military spending and other government outlays would shift from below one in the short term to above one in the long run, driven by sizeable government R&D expenditure.25 Also, in a Sraffian supermultiplier model of growth that takes into account the entrepreneurial role of the state (Deleidi and Mazzucato 2019 and 2021) there is evidence of a strong crowd-in impact of government R&D defence expenditures and of their large fiscal multiplier. The impact is larger for policies aimed at producing a structural change—like mission-oriented innovation policies (Mazzucato 2018)—that boost growth expectations, stimulate private R&D investment, and have a large positive effect on economic growth. Draghi (2024a) recommends to increase and concentrate on common initiatives the European funding for R&D. This could be reached via the dual-use programmes and a proposed European Defence Projects of Common Interest to organize the necessary industrial cooperation.

9.5 Conclusion

This chapter has provided new evidence that almost all EU countries have boosted military spending in recent years and are planning to increase it even further in the future. The trend started after the Russian invasion of Crimea in 2014, and while at that time almost no EU country met NATO’s spending target of 2% of GDP in defence, today around ten countries have reached that benchmark. The increase in overall spending is also accompanied by a change in the composition of such expenditure, with a growing share of investment in equipment, which may also be conducive to positive economic spillovers, according to the literature.

The articulation across different budgetary authorities in a multilevel governance system like the EU is of fundamental importance. Not only because of efficiency concerns in terms of public expenditure, but also and mainly for the sake of the effectiveness of the overall defence policy.

In March 2024, the European Commission launched a new strategy to boost defence spending and achieve better readiness. A new fund should also add €1.5 billion to the current common provisions for defence spending in the Multiannual Financial Framework. But most of all, this new strategy calls for a leap forward in integration and joint spending in the next common financial framework.

This chapter has explained the rationale behind stronger integration in defence spending at EU level, but it has also highlighted the reasons why national governments may resist such delegation of power. While, on the one hand, economic arguments suggest potential efficiency gains and improved returns from mutualization of defence spending; on the other hand, the political reality of a multilevel governance system, in which central powers are only delegated by the national level, calls for some caution.

Without convergence of broad geopolitical objectives, budgetary integration in this area may not be fully possible. The institutional evolution of defence policy in the EU attempts to build on a progressive convergence of foreign policy objectives across Member States. The main questions for the future of the EU common defence policy are to what extent this convergence will hold in the new geopolitical context and, if so, to what extent it will be reflected in new common provisions for defence in the common budget.

References

Alptekin, A., and P. Levine (2012) “Military Expenditure and Economic Growth: A Meta-analysis”, European Journal of Political Economy 28(4): 636–650, https://doi.org/10.1016/j.ejpoleco.2012.07.002

Angelopoulos, K., A. Philippopoulos, and E. Tsionas (2008) “Does Public Sector Efficiency Matter? Revisiting the Relation between Fiscal Size and Economic Growth in a World Sample”, Public Choice 137: 245–278, https://doi.org/10.1007/s11127-008-9324-8

Antolin-Diaz, J., and P. Surico (2022) “The Long-Run Effects of Government Spending”, CEPR Discussion Paper 17433.

Benoit, E. (1978) “Growth and Defense in Developing Countries”, Economic Development and Cultural Change 26(2): 271–280.

Becker, J. (2017) “The Correlates of Transatlantic Burden Sharing: Revising the Agenda for Theoretical and Policy Analysis”, Defense & Security Analysis 33(2): 131–157, https://doi.org/10.1080/14751798.2017.1311039

Becker, J. (2021) “Rusty Guns and Buttery Soldiers: Unemployment and the Domestic Origins of Defense Spending”, European Political Science Review 13(3): 307–330, https://doi.org/10.1017/S1755773921000102

Becker, J., and J. P. Dunne (2021) “Military Spending Composition and Economic Growth”, Defence and Peace Economics 34(3): 259–271.

Becker, J., S. Benson, J. P. Dunne, and E. Malesky (2024) “Disaggregated Defense Spending: Introduction to Data”, Journal of Peace Research, https://doi.org/10.1177/00223433231215785

Buti, M., and G. Papaconstantinou (2022) “European Public Goods: How Can We Supply More?”, Policy Brief 3, Luiss School of European Political Economy, https://leap.luiss.it/wp-content/uploads/2022/06/PB3.22-European-Public-Goods.-How-can-we-supply-more.pdf

Cepparulo, A., and P. Pasimeni (2024) “Defence Spending in the European Union” Discussion Paper 199, European Commission, https://economy-finance.ec.europa.eu/publications/defence-spending-european-union_en

Churchill, A. S., and S. L. Yew (2018) “The Effect of Military Expenditure on Growth: An Empirical Synthesis”, Empir Econ 55(3): 1357–1387, https://doi.org/10.1007/s00181-017-1300-z

Ciaffi, G., M. Deleidi, and M. Mazzucato (2024) “Measuring the Macroeconomic Responses to Public Investment in Innovation: Evidence from OECD Countries”. Industrial and Corporate Change 33(2): 363–382.

Council of the European Union (7371/22) “A Strategic Compass for Security and Defence—For a European Union that Protects its Citizens, Values and Interests and Contributes to International Peace and Security”.

Council Decision (CFSP) (2017) “Council Decision 2017/2315 of 11 December 2017”, https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32017D2315&from=EN

Deleidi, M., and M. Mazzucato (2019) “Mission-Oriented Innovation Policies: A Theoretical and Empirical Assessment for the US Economy”, Departmental Working Papers of Economics - University ‘Roma Tre’ 0248, Department of Economics - University Roma Tre.

Deleidi, M., and M. Mazzucato (2021) “Directed Innovation Policies and the Supermultiplier: An Empirical Assessment of Mission-oriented Policies in the US Economy”, Research Policy 50(2), https://doi.org/10.1016/j.respol.2020.104151

Draghi, M. (2024a) The Future of European Competitiveness. Part A: A Competitiveness Strategy for Europe. Brussels: European Commission.

Draghi, M. (2024b) The Future of European Competitiveness. Part B: In-depth Analysis and Recommendations. Brussels: European Commission.

Dunne, J. P., R. Smith, and D. Willenbockel (2005) “Models of Military Expenditure and Growth: A Critical Review”, Defence and Peace Economics 16(6): 449–460.

Dunne, J. P., and N. Tian (2016) “Military Expenditure and Economic Growth, 1960–2014”, The Economics of Peace and Security Journal 11(2), https://doi.org/10.15355/epsj.11.2.50

Dunne, J. P., and R. P. Smith (2020) “Military Expenditure, Investment and Growth”, Defence and Peace Economics 31(6): 601–614, https://doi.org/10.1080/10242694.2019.1636182

European Commission (2017) JOIN. 41 Final Improving Military Mobility in the European Union. Brussels: European Commission.

European Commission (2018) JOIN. 5 Final On the Action Plan on Military Mobility. Brussels: European Commission.

European Commission (2022a) JOIN. 48 Action Plan on Military Mobility 2.0. Brussels: European Commission.

European Commission (2022b) JOIN. 24 Final On the Defence Investment Gaps Analysis and Way Forward. Brussels: European Commission.

European Commission (2024) JOIN. 10 Final A New European Defence Industrial Strategy: Achieving EU Readiness through a Responsive and Resilient European Defence Industry. Brussels: European Commission.

European Council (1999a) “Declaration of the European Council on Strengthening the Common European Security and Defence”, European Council, Cologne 3–4 June 1999, https://www.europarl.europa.eu/summits/kol1_en.htm

European Council (1999b) “Presidency Conclusions”, Helsinki European Council, 10–11 December 1999, https://www.consilium.europa.eu/uedocs/cms_data/docs/

pressdata/en/ec/ACFA4C.htm

European Council (March 2024) “Conclusions—21 and 22 March 2024”, https://www.consilium.europa.eu/media/70880/euco-conclusions-2122032024.pdf

EDA (2018) Factsheet: Capability Development Plan. Brussels: EDA, https://eda.europa.eu/publications-and-data/factsheets/factsheet-capability-development-plan

EDA (2021) Annual Report. Brussels: EDA.

EDA (2022) 2022 Coordinated Annual Review on Defence Report. Brussels: EDA.

EDA (2023) Annual Report. Brussels: EDA.

EU (2014) “The Mechanism for Financing Military Operations (Athena). Summaries of EU Legislation”, https://eur-lex.europa.eu/EN/legal-content/summary/the-mechanism-for-financing-military-operations-athena.html

Fiott, D. (2023) “In Every Crisis an Opportunity? European Union Integration in Defence and the War on Ukraine”, Journal of European Integration 45(3): 447–462, https://doi.org/10.1080/07036337.2023.2183395

Fuest, C., and J. Pisani-Ferry (2019) “A Primer on Developing European Public Goods”, EconPol Policy Report 16(3), https://www.econstor.eu/bitstream/10419/219519/1/econpol-pol-report-16.pdf

Håkansson, C. (2023) “The Ukraine War and the Emergence of the European Commission as a Geopolitical Actor”, Journal of European Integration 46(1): 25–45, https://doi.org/10.1080/07036337.2023.2239998

Letta, E. (2024) Much More Than a Market, https://www.consilium.europa.eu/media/ny3j24sm/much-more-than-a-market-report-by-enrico-letta.pdf

Malizard, J. (2015) “Does Military Expenditure Crowd Out Private Investment? A Disaggregated Perspective for the Case of France”, Economic Modelling 46: 44–52.

Mazur, S. (2021) “Security and Defence Heading 5 of the 2021–2027 MFF”, Briefing 2021–2027 MFF, European Parliamentary Research Service, https://www.europarl.europa.eu/RegData/etudes/BRIE/2021/

690545/EPRS_BRI(2021)690545_EN.pdf

Mazzucato, M. (2013) The Entrepreneurial State: Debunking Public vs Private Sector Myths. London: Anthem Press.

Mazzucato, M. (2018) “Mission-oriented Innovation Policies: Challenges and Opportunities”, Industrial and Corporate Change 27(5): 803–815.

Moretti, E., C. Steinwender, and J. Van Reenen (2023) “The Intellectual Spoils of War? Defense R&D, Productivity, and International Spillovers”, Review of Economics and Statistics, 1–46.

Mowery, D. C. (2010) “Military R&D and Innovation”, in B. H. Hall and N. Rosenberg (eds), Handbook of the Economics of Innovation. North Holland: Elsevier, pp. 1219–1256. https://doi.org/10.1016/S0169-7218(10)02013-7

Musgrave, R. A. (1939) “The Nature of Budgetary Balance and the Case for the Capital Budget”, American Economic Review 29(2): 260–271.

NATO. (2014). Wales Summit Declaration Issued by the Heads of State and Government Participating in the Meeting of the North Atlantic Council in Wales, https://www.nato.int/cps/en/natohq/official_texts_112964.htm

Oates, W. E. (1999) “An Essay on Fiscal Federalism”, Journal of Economic Literature 37(3): 1120–1149.

Oates, W. E. (2005) “Toward a Second-Generation Theory of Fiscal Federalism”, International Tax and Public Finance 12: 349–373.

Pivetti, M. (1989) “Military Expenditure and Economic Analysis: A Review Article”, Contributions to Political Economy 8(1): 55–67.

Pivetti, M. (1992) “Military Spending as a Burden on Growth: an ‘Underconsumptionist’ Critique”, Cambridge Journal of Economics 16(4): 373–384.

Smith, R. P., and P. Dunne (1994) “Is Military Spending a Burden? A Marxo-Marginalist Response to Pivetti”, Cambridge Journal of Economics 18(5): 515–521.

Santamaría, P. G.-T., A. A. García, and A. G. Domonte (2022) “Scientometric Analysis of the Relationship between Expenditure on Defence and Economic Growth: Current Situation and Future Perspectives”, Defence and Peace Economics, 34(8): 1071–1090, https://doi.org/10.1080/10242694.2022.2091191

Wyplosz, C. (2016) “The Six Flaws of the Eurozone”, Economic Policy 31(87): 559–606.

Yesilyurt, F., and M. E. Yesilyurt (2019) “Meta-analysis, Military Expenditures and Growth”, Journal of Peace Research 56: 352–363. https://doi.org/10.1177/0022343318808841

1 The views expressed in the text are the private views of the authors and may not, under any circumstances, be interpreted as stating an official position of the European Commission.

2 European Commission.

3 Brussels School of Governance (BSoG) at the Vrije Universiteit Brussel (VUB).

4 For a theoretical discussion on the defence-growth nexus see also Pivetti (1989; 1992) and Smith and Dunne (1994). For a recent survey of the empirical literature on the direction and nature of the defence-growth nexus in advanced economies see Cepparulo and Pasimeni (2024).

5 PESCO in the area of security and defence was firstly introduced by article 42(6) of the Lisbon Treaty on European Union (TEU).

6 These costs include: HQ implementation and running costs, including travel, IT systems, administration, public information, locally hired staff, Force Headquarters (FHQ) deployment and lodging for forces as a whole, infrastructure, medical services (in theatre), medical evacuation, identification, acquisition of information (satellite images), and reimbursements to/from NATO or other organizations (e.g. the UN).

7 For a detailed description of the negotiations of this heading see Mazur (2021).

8 EDIDP is dominated by four big European businesses (Airbus, Leonardo, Thales, and Indra Sistemas) that are partially owned by their respective governments and by US investment funds.

11 The data collection started gathering data from twenty-two countries extending to all others over time. Denmark joined only on 23 March 2023.

12 Ireland and Austria are not members of the NATO alliance while Sweden became NATO’s newest member on 7 March 2024.

13 Denmark joined formally PESCO on May 2023.

14 Every April, EU Member States are required to lay out their fiscal plans for the next three years.

15 In the case of Finland, the expected increase of spending is also related to the NATO membership.

16 Austria, Croatia, Italy, Sweden, Denmark, Germany, Lithuania, and Poland.

17 Belgium, Greece, France, Ireland, Hungary, Romania, Portugal, and Slovenia.

18 Equipment expenditure includes major equipment expenditure and R&D devoted to major equipment according to the NATO definition.

19 Personnel expenditure includes military and civilian expenditure and pensions according to the NATO definition.

20 Infrastructure expenditure includes NATO common infrastructure and national military construction, according to the NATO definition.

21 Other expenditure includes operations and maintenance expenditure, other R&D expenditure and expenditure not allocated among above-mentioned categories.

23 According to the European defence industrial strategy (2024), it is expected that by 2030, EU countries should: buy at least 40% of the defence equipment by working together.

24 This corresponds to the latest available data in the public dataset provided by EDA.

25 See Ciaffi et al. (2024) for a survey of the macroeconomic effects of public R&D spending.